Call Girls Laxmi Nagar Delhi reach out to us at ☎ 9711199012

Malaysian Palm Oil FORTUNE 2014 Volume 4

1. INTRODUCTION

This paper will provide an overview of

how the issue of environmental

degradation and the depleting of natural

resources and how oil palm can

contribute in managing the solution. It will

also look at how development over the

years has evolved especially in the oils

and fats sector. Developed by

Massachusetts Institute of Technology

(MIT) researchers using data from 1900

to 1970, this model shows the limits of

growth model with insights into the

management of these issues. In a

nutshell, the limit of growth model

professes that to maximize global output,

the world needs to be efficient in using

natural resources and minimise

environment destruction in the production

process.

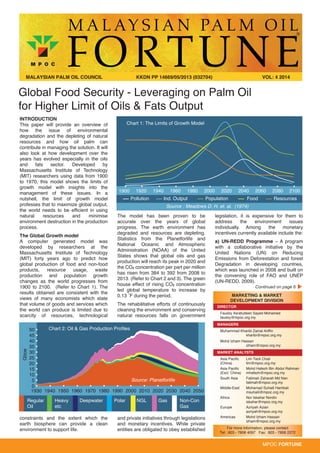

The Global Growth model

A computer generated model was

developed by researchers at the

Massachusetts Institute of Technology

(MIT) forty years ago to predict how

global production of food and non-food

products, resource usage, waste

production and population growth

changes as the world progresses from

1900 to 2100. (Refer to Chart 1). The

results obtained are consistent with the

views of many economists which state

that volume of goods and services which

the world can produce is limited due to

scarcity of resources, technological

constraints and the extent which the

earth biosphere can provide a clean

environment to support life.

The model has been proven to be

accurate over the years of global

progress. The earth environment has

degraded and resources are depleting.

Statistics from the Planetforlife and

National Oceanic and Atmospheric

Administration (NOAA) of the United

States shows that global oils and gas

production will reach its peak in 2020 and

the CO² concentration per part per million

has risen from 384 to 392 from 2008 to

2013. (Refer to Chart 2 and 3). The green

house effect of rising CO² concentration

led global temperature to increase by

0.13 ˚F during the period.

The rehabilitative efforts of continuously

cleaning the environment and conserving

natural resources falls on government

and private initiatives through legislations

and monetary incentives. While private

entities are obligated to obey established

legislation, it is expensive for them to

address the environment issues

individually. Among the monetary

incentives currently available include the:

a) UN-REDD Programme – A program

with a collaborative initiative by the

United Nations (UN) on Reducing

Emissions from Deforestation and forest

Degradation in developing countries,

which was launched in 2008 and built on

the convening role of FAO and UNEP

(UN-REDD, 2009).

MPOC FORTUNE

MALAYSIAN PALM OIL COUNCIL KKDN PP 14669/05/2013 (032704) VOL: 4 2014

®

DIRECTOR

Faudzy Asrafudeen Sayed Mohamed

faudzy@mpoc.org.my

MANAGERS

Muhammad Kharibi Zainal Ariffin

kharibi@mpoc.org.my

Mohd Izham Hassan

izham@mpoc.org.my

MARKET ANALYSTS

Asia Pacific Lim Teck Chaii

(China) lim@mpoc.org.my

Asia Pacific Mohd Hafezh Bin Abdul Rahman

(Excl. China) mhafezh@mpoc.org.my

South Asia Fatimah Zaharah Md Nan

fatimah@mpoc.org.my

Middle-East Mohamad Suhaili Hambali

msuhaili@mpoc.org.my

Africa Nor Iskahar Nordin

iskahar@mpoc.org.my

Europe Azriyah Azian

azriyah@mpoc.org.my

Americas Mohd Izham Hassan

izham@mpoc.org.my

MARKETING & MARKET

DEVELOPMENT DIVISION

For more information, please contact

Tel : 603 - 7806 4097 Fax: 603 - 7806 2272

Continued on page 6

Global Food Security - Leveraging on Palm Oil

for Higher Limit of Oils & Fats Output

Chart 1: The Limits of Growth Model

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

Pollution Ind. Output Population Food Resources

Source : Meadows D. H. et. al. (1974)

50

45

40

35

30

25

20

15

10

5

0

1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Chart 2: Oil & Gas Production Profiles

Gboe

Regular

Oil

Heavy

etc

Deepwater Polar NGL Gas Non-Con

Gas

Source: Planetforlife

2.

3. MPOC FORTUNE • 3

MARKETInsightsIns g

About Us

1. Changzhou City

Located in the center of Yangtze River

Delta, the most prosperous and dynamic

region in China, Changzhou is a

fast-growing industrial city, situated in the

middle between Shanghai and Nanjing.

As one of the central cities in Grand

Shanghai Economic Circle, Changzhou

is an important base of manufacturing

and logistics.

- An ancient city with a history of more

than 3,200 years

- 4,385 km² with 4.69 million registered

population

- Top 4 of Livable Cities in China in 2013

- Gold Award of International Garden City

in 2012

- No.9 of the Best Commercial Cities in

China by Forbes

2. CZBJ Profile

Jiangsu Changzhou Binjiang Economic

Development Zone (CZBJ), formerly

called Jiangsu Xinbei Industrial Park, was

established in April 2006 with the

approval of Jiangsu Provincial

Government and verification of National

Development and Reform Commission.

Covering an industrial area of 34.5 km²,

CZBJ achieved great economic

performance in 2013:

CZBJ has long become a hotspot for

investors from both home and abroad. In

recent years, many World Fortune 500

and leading industrial enterprises have

been set up in our development zone, i.e.

Ashland, Novelis, Micarta from the USA;

Lanxess, Linde, Wurth from Germany;

AkzoNobel from Netherlands; DIC from

Japan; Saint-Gobain from France and

etc. Both central state-owned enterprises

and producer services develop fast, i.e.

China Resources, State Grid, Dongfeng

Continued on page 8

Changzhou

Binjiang

Economic

Development

Zone (CZBJ) –

Gateway to

Palm Bioenergy

Investment

in China

4. North Port, Port Klang

- Fima Bulking Services Berhad

- Fimachem Sdn Bhd

- Fima Liquid Bulking Sdn Bhd

- Fima Freight Forwarders Sdn Bhd

Butterworth

- Fima Palmbulk Services Sdn Bhd

Jalan Parang, 2nd Extension, North Port, 42000 Port Klang, Selangor, MALAYSIA

Tel: +603 - 3176 7211 Fax: +603 - 3176 5641 Email: enquiry@fimabulking.com

http://www.fimabulking.com

Located in a free commercial

zone offer excellent

opportunities for

• Import and export

• Transhipment

• MDEX tender (approved

delivery point)

• Regional collection /

distribution hub

Facilities available :

• Carbonsteel

• Coated & stainless tanks come

with heating facilities &

nitrogen blanketing.

Malaysia’s Largest Independent

Common-user Multi-purpose Liquid

Bulk Terminal Operator

5. MPOC FORTUNE • 5

Continued on page 7

Much has been said and written about

India’s continuing reliance on imported

vegetable oils to meet the increasing

demand for edible consumption.

Domestic production continues to

stagnate and demand continues to rise

on the back of the multiplier effect of

rising population and economic wellbeing

of the population. Not much thought has

been given to the potential for increased

imports emanating from industrial growth,

particularly in the oleo chemicals industry.

Increasing demand for biodegradable

and sustainable products, coupled with

recent changes in regulations, are

increasing the importance of

oleochemicals in various segments of the

chemicals industry, like lubricants and

biosurfactants for eg., all of this offer

significant opportunities for companies in

the long run. Companies that explore

organic and/or inorganic growth options

in this market space could be poised for

major growth.

Traditionally, oleochemicals have been

used for applications in surfactants,

personal care, soaps, detergents and

food additives. However, various new

applications are emerging where they

can replace petroleum-based products,

creating exciting growth opportunities.

Oleo-chemicals is a fast growing sector

in India, with major demand for oleo

products coming from the below

segments.

SOAPS

Personal Care products are likely to

experience a great thrust in

consumption, where Indian consumption

lags far behind world standards. In so far

as soaps are concerned, they have a

99% market penetration but the per

capita consumption is significantly lower

than the global average. Compared to a

per capita consumption of 6500 gms per

annum in USA and 4000 gms in China,

Indian soap consumption lags way

behind at only about 730 gms per capita

per annum. This, by itself, points to the

possibility of a much larger palm oil

requirement from the soap segment

alone. Although bar soaps are the largest

component, there is tremendous

potential for growth in the hand wash

segment as well.

Soap consumption has experienced a

CAGR of about 4% in 2008-13. It is likely

to grow at a CAGR of 3% to 5% between

2013 to 2020. The main thrust of the

FMCG sector is to target rural areas

which seem to show the greatest

potential as more than 50% of the

population lives in rural areas.

The greatest potential is for liquid soaps

where consumption levels are extremely

low. This segment is expected to achieve

a CAGR rate of 16% in the 2013-20

period.

Personal care – Bar Soaps

Bar Soaps are the largest FMCG product

segment and is expected to see a growth

of 6% in volume over FY13-20

DETERGENTS

Laundry detergents are the biggest

segment accounting for about 90% of the

total detergent market. These detergents

are available as bars, powders and

liquids. Powders comprise majority of the

laundry market in India while liquid

detergents are still in a nascent stage of

market development.

Dishwashing detergents are available as

bars, powders and liquids; bars and

powders account for about 85% of the

total market by value but this is expected

to decrease to 75% by 2020. Overall

dishwashing detergent penetration in

India is expected to grow from about 30%

of households to about 40% by 2020.

Liquid detergents constitute about 5% of

the volume and 15% of the value in

dishwashing detergents and are

expected to increase to 11% in volume

and 30% value by 2020. The first liquid

laundry detergent product was launched

in India by Hindustan Lever in May 2013.

Liquid laundry detergents are expected

to grow to about 5% of the volume by

2020.

Consumers from rural areas and smaller

towns are increasingly shifting towards

use of detergent cleaning products owing

to growing concerns for hygiene.

Extensive marketing by FMCG

companies in these newer markets has

provided impetus to growth in per capita

consumption

Premium detergent products such as

machine wash and post-wash softeners

still have low penetration in India even in

urban areas but are expected to ramp up

over the next few years. Another

emerging trend in the detergents industry

is the focus on using less water in low

temperature washes and producing

lower waste during production and

usage.

MARKETInsightsIns g

1400

1200

1000

800

600

400

200

0

FY08 FY09 FY10 FY11 FY12 FY13 FY20

688 717 764 816 855 900

1,241CAGR 5%

CAGR 6%

Country Grams Per Year (FY13)

India ~730

China 4,000

USA 6,500

Per capita consumption – Bar Soaps

Source: Indiastat, KPMG Analysis

India's per capita consumptionis

projected to increase to ~920

gramsby FY20

Bar Soap Volume

Good Potential for

Palm Oleo Chemicals in India

Source: Euromonitor, analyst reports,

KPMG analysis

6. b) Clean Development Mechanism

(CDM) – A mechanism developed as

defined in Article 12 of the Protocol, which

allows countries with emission-reduction

commitment to implement emission-

reduction projects in developing countries

to earn saleable certified emission

reduction (CER) credits to meet the Kyoto

targets (UNFCC, 2014).

c) EU’s Renewable Energy Directive

(RED) – A directive which requires that

20% of the energy consumed within the

European Union is from renewable

sources by 2020 with specified targets for

use of renewable fuels and reduction of

greenhouse gas (GHG) emission across

all energy sector (Glass, 2013).

d) USA Renewable Fuel Standard

(RFS) – A standard established under the

Energy Policy Act (EPAct, 2005) to

develop and implement regulations to

ensure transportation fuel in United

States (US) contains a minimum volume

of renewable fuel, which will increase

each year, escalating to 36 billion by year

2022 (EPA, 2013).

In the oils and fats trade, consumers

especially those in developed countries

are demanding for sustainably produced

and environmental friendly products. This

new purchasing behaviour is created by

NGOs who often create issues to further

their cause and make their claim without

the backing of justifiable facts and figures

(Yusof, 2013). These NGO’s are blaming

the palm oil industry for environmental

destruction and they blow issues out of

proportion just to entice financial support.

As a result, the consumers are now

demanding and governments especially

in Europe has developed stringent

production guidelines which is applied to

producers through certification schemes.

The certification schemes ensure products

comply with the requirement imposed in

various concerns such as environment,

social and legislation to satisfy consumer

needs. Certification ensures products are

produced in compliance with the

consumer requirement including

Sustainability, which has become a major

concern. Amongst the notable

sustainability certification schemes are the

Roundtable on Sustainable Palm Oil

(RSPO) Certification Scheme, Indonesia

Standard for Sustainable Palm Oil (ISPO)

and EU’s International Sustainability &

Carbon Certification (ISCC). As for

Malaysia, there are plans to introduce the

Malaysian Standard for Sustainable Palm

Oil (MSPO) certification in the near future.

Financial institutions are also taking a cue

from this development amidst the new

consumer demands to strengthen their

brand value. For example, HSBC has

recently announced that they will not

finance oil palm companies whose

business activities result in environmental

destruction. (HSBC, March 2014)

Although the limits of growth model

together with some economist predict that

global output volume will, upon reaching

its peak will start to decline, it is yet to be

proven in the global food production.

Based on FAO statistical trend of food

production, it shows that yearly growth of

food production is 3.4% which exceeds

population growth of 1.6%. A similar trend

was observed for global oils and fats

production trend. (Refer to table 1 and 2).

One possible reason is that the

production level has not hit the maximum

limit.

However, there is still a risk of reduction in

global food production as arable land per

capita has declined from 1961 to 2012.

(Refer to table 3). Based on the limits of

growth model, environmental degradation

and global depletion of natural resources

are other factors which could contribute to

6 • MPOC FORTUNE

394

392

390

388

386

384

382

2008 2009 2010 2011 2012 2013

Chart 3: Recent Global Monthly Mean CO²

PartsPerMillion

Source: NOAA, 2014

200

180

160

140

120

100

80

60

40

20

0

8

7

6

5

4

3

2

1

0

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Table 2: Population Vis-a-vis Oils & Fats Production growth

Average population growth: 1.6%

Mn MT Billion

Average O&F production growth: 2.4%

’MnMT

Billionpeople

Source: Oil World Annual, Jan - Mar 2014

Continued from page 1

MARKETInsightsIns g

Global Food Security

- Leveraging on Palm

Oil for Higher Limit of

Oils & Fats Output

Continued on page 9

9

8

7

6

5

4

3

2

1

0

1961 1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009

Table 1: Population Vis-a-vis Global Food Production

Average population growth: 1.6%

Population (Billion) Food Production (Billion MT)

Average food production growth: 2.4% Source: FAO

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Table 3: Global arable land per capita

Hectares per capita

Source: FAO

0.14

0.12

0.10

0.08

0.06

0.04

0.02

0.00

Hectarespercapita

7. MPOC FORTUNE • 7

4,000

5,000

4,500

3,500

3,000

2,500

2,000

1,000

500

1,500

0

Detergents Volume

Country Kg Per Year (FY10)

India 2.5

China 4

USA 10

Per capita consumption – Laundry detergents

Laundry Dishwashing

Source: Analyst reports,

KPMG analysis

India’s per capita consumption

is projected to increase to 3.4kg

per annum by FY20

FY08 FY09 FY10 FY11 FY12 FY13 FY20

CAGR 7%

CAGR 9%

2,103

228

2,215

251

2,409

274

2,640

294

2,790

318

3,006

345

4,651

545

250

200

150

100

50

0

36 44 48 55

66

79

222

CAGR 16%

CAGR 17%

Skin care volume

FY08 FY09 FY10 FY11 FY12 FY13 FY20

Source: Feedback Industry Report Skin

Care 2013; Indiastat, KPMG analysis

Country USD Per Year Country USD Per Year

India 0.6

China 6.6

USA 32

Germany 55.4

Per capita consumption – Skin care

Source: Unilever Investor Seminar 2010; Note: India (2012), Others (2010)

Per capita consumption of laundry

detergents in India is estimated at 2.5 kg

per annum in 2013 and is projected to

increase to 3.4 kg per annum in 2020

Detergents - Laundry and dishwashing

Detergents are likely to have a modest

growth in volume with laundry detergents

continuing to remain the largest category

SKIN CARE

Key products in the Indian skin care

market include fairness creams (45%)

and moisturisers (22%). The remaining

33% include specialized products such

as toners and astringents, antiseptic

creams, premium skin care creams,

etc…

India’s per capita spend on skin care is

estimated to be only 1/10th of China’s.

This indicates a large potential for future

growth. Per capita consumption of skin

care products in India is expected to

increase from about 64 gms in 2013 to

approx. 164 gms by 2020.

Personal Care – Skin Care &

cosmetics

Volume growth in the skin care segment

is expected to be driven by premium &

men’s grooming products

COSMETICS

The industry consists of lip paint, nail

paint, eye makeup and facial make up.

Lip and nail make-up are estimated to

account for about 80% of the market.

Cosmetics industry in India has grown at

about 25% per annum over 2008-13 and

is expected to continue to sustain the

growth momentum going forward,

growing at about 22% over 2013-20.

Per capita spending on cosmetics in

India remains significantly lower than

other developed countries and indicates

significant growth potential. Higher

discretionary spending, strong media

exposure leading to increased fashion

consciousness, entry of several

international cosmetic manufacturers,

demand from men’s grooming segment

are key drivers leading industry growth.

Personal care – Skin Care &

Cosmetics

Cosmetics is still under-penetrated in

India but is expected to continue its high

growth momentum

OTHER SECTORS

Other major sectors of oleo chemicals

users include pharmaceuticals, tobacco

processing, rubber processing, paints,

plastics, etc. Palm based products

account for a significant portion of the

feedstock for the oleo chemicals industry,

with soaps accounting for the major

chunk.

Continued from page 5

MARKETInsightsIns g

Good Potential for Palm Oleo Chemicals in India

Continued on page 11

8. Motor, China National Salt Corporation,

Guodian Power (Changzhou),

Longcheng Steel Market, Turbo-logistics,

ABLE logistics and etc.

At present, three pillar industrial sectors

have been formed:

Advantages for Biofuel/ Biomass

Industry

With the only professional chemical park

in Changzhou, CZBJ focuses on

developing new materials and new

energy. In 2013, gross industrial output

realized by new materials and new

energy enterprises reached 60.5 billion

CNY, accounting for about 65% of that of

large-scale enterprises in CZBJ.

To promote biomass and biofuel industry,

CZBJ demonstrates advantages in four

aspects:

1. Sufficient Land Capacity

CZBJ has reserved a land of about 790

hectares with port and logistic resources

for quality projects. Moreover, the land

has been approved by provincial and

municipal government to develop

chemical, chemical new material and

new energy (biomass energy) industry.

2. Convenient Traffic Network

Possessing the entire Yangtze River

waterfront resources in Changzhou,

CZBJ enjoys “4D” transportation network:

Changzhou port is a first class ocean

going port approved by the State Council

and one of the 63 ports directly

connected to Taiwan. Changzhou Port is

planned to build 15 berths of 100,000

DWT and 52 berths of 1000DWT. By

2015, the handling capacity will be 6MT,

and reach 100 MT in 2020. Customs

supervision station and bonded

warehouses are available in the park,

providing 24-hour onsite service for

enterprises.

Changzhou Airport is a 4E level airport,

providing 20 domestic airlines to major

cities in China. Flights to some Asian

cities including HK will be open within

2014.

Continued on page 10

Changzhou Binjiang Economic

Development Zone (CZBJ) – Gateway to

Palm Bioenergy Investment in China

Continued from page 3

MARKETInsightsIns g

8 • MPOC FORTUNE

9. Table 6: Major emitters of GHG of palm biodiesel

Emission sources Amount (kg CO²/

tonnes biodiesel)

Production of fertilizers used 185 (11.5%)

Nitrous oxide emitted 130 (8.1%)

Use of pesticides 34 (2.1%)

Transportation & machinery use 89 (5.6%)

Milling & refining of palm oil 19 (1.2%)

EFB 87 (5.4%)

Effluent ponds 824 (51.5%)

Transportation to mills, refineries 36 (2.3%)

Biodiesel refining 197 (12.3%)

Total 1,601 (100%)

Production & use of fossil fuel 4,228

Palm biodiesel savings 2,627

GHG emission saving relative to fossil diesel 65%

Source: van Zutphen ( 2007)

MPOC FORTUNE • 9

the risk of down trend in global food

production.

How palm oil fits into the model

With the inclusion of oil palm into the

equation it is quite definite that the

maximum global output limit will be higher

than the figure predicted by the

researchers from the Massachusetts

Institute of Technology (MIT). The model

did not factor in the contribution of the oil

palm sector as their model was built for

the period from 1900 to 1970 before the

global palm oil industry was developed by

Malaysia and Indonesia in the 1970s.

(Yusof, 2007)

As a crop, oil palm has helped to save the

amount of land utilised to produce edible

oils to feed the world. Oil palm is a high

yielding crop producing 11 times more oil

compared to soybean, 10 times more

compare sunflower oil and 7 times more

than rapeseed (Khosla & Sundram, 2010).

In 2013, global palm oil production was at

56.2 million MT and accounted for almost

30% of global oils and fats production of

190 million MT (Oil World, 2014).

Oil palm crop also has a high carbon

sequestration. In Malaysia’s case, oil

palm could cover the carbon emission of

land use change by the rice sector and

emission from other minor system of the

economy (Ministry of Natural Resources

& Environment Malaysia, 2011). It is quite

close to the CO² removal of forest. In

2007, the amount of CO² removed by the

oil palm sector is high at 68% of the

amount removed by the forest. Life Cycle

analysis done by van Zutphen shows that

CO² emission from the production of 1

MT of palm bio-diesel is lower than

soyabean and canola based biodiesel.

The emission is also lower than the

production of 1 MT of diesel. (Refer to

table 4 & 5 for the detail).

Unfair trade practices on palm

In spite of the superior qualities and the

versatility of palm oil in safeguarding the

world’s food security and environment, it

is not included in the EU-RED and

USA-RFS programmes. Such decisions

might have been made due to specific

countries interest to protect local

agricultural industry and policy by

deliberately ignoring palm oil’s superior

contribution. The testing method use to

establish the GHG savings emission in

EU and USA may not be inclusive or

representative of palm oil’s GHG savings.

Based on Van Zutphen (2008) study, the

oil palm industry Green House Gas

saving relative to fossil diesel is 65%.

This savings exceeds the threshold value

of EU-RED of 35%.

The USA-RFS differs from EU-RED in its

computation of GHG emission as it

include emission from palm kernel

processing but does not include emission

from land use change resulting in a

threshold value of 20%. As for life cycle

analysis on palm based biodiesel

production conducted by MPOC, it shows

a 101% savings over fossil fuels.

Therefore, the two studies conducted by

van Zutphen and MPOC show that palm

oil biodiesel feedstock should qualify for

the benefits of US-RFS and EU-RED

programme.

Conclusion

Oil palm is a perennial crop which

supports the basis for the development of

the limits of growth model. The model

promotes efficient use of resource while

minimizing environmental destruction

during production. In line with the basis of

the model, oil palm cultivation enables

efficient land usage with high productivity

of agricultural crop on limited land while

promoting greener environment. Every

Continued from page 6

MARKETInsightsIns g

Global Food Security

- Leveraging on Palm

Oil for Higher Limit of

Oils & Fats Output

Continued on page 12

20072000

167

Forest

82

Palm

147

40.5

35.6

147*

Forest

100*

Palm

Plantation

217

49

26.9

Total CO²

Emission 223.1

Total CO²

removal by

LULUCF 249.8

Total CO²

removal by

LULUCF 247

Total CO²

Emission 292.9

Emissions by others

LULUCF

+

Rice Sector

350

300

250

200

150

100

50

0

Source: Ministry of Natural Resources & Environment Malaysia

Table 4 : Malaysian Greenhouse Gas Emission and Removal (MT)

Land Use, Land Use Change and Forestry (LULUCF)

is made of Forestry and (Oil Palm) Plantation sector

Table 5 : Palm oil biofuel is superior to

other biofuels to arrest climate change

Source: van Zutphen ( 2008)

4500

4000

3500

3000

2500

2000

1500

1000

500

0

kgCO²/tonne

Palm Oil Soya Canola Diesel

byns

10. 10 • MPOC FORTUNE

Continued from page 8

MARKETInsightsIns g

3. Broad Market Prospect

Usually palm oil is used to produce

biofuel, food and daily chemical products.

Due to the superior location, Changzhou

is surrounded by many enterprises of

these three kinds.

4. Sound Public Facilities

Power Supply

Two 220kV and two 110kV power

substations, with a total capacitance of

540,000KVA. Dual-circuit input line of 10kV,

20kV, 35kV and 110kVcan be provided.

Water Supply

Yangtze River provides abundant water

resource.

One tap water plant: 1,000,000t/d, and

one industrial water plant: 80,000t/d.

The demineralized water can be

supplied.

Steam Supply

Three thermal power plants with a

capacity of 1200t/h. High pressure:

4.5MPa, low pressure 0.4~1.0Mpa.

Natural Gas

The “West-East” and “Sichuan-East”

National Gas Transmission Projects have

distribution stations in the zone. The

pipelines have been laid along the main

roads to ensure civil and industrial

utilization.

Sewage Treatment

Two sewage treatment plants with a

capacity of 330,000t/d, (another

100,000t/d-plant is under construction),

including 30,000 t/d chemical wastewater

treatment capacity.

Residue Treatment

There are professional residue treatment

plants with an incineration capacity of

9,900t/a, another 30,000t/a incineration

unit is under planning, collection capacity

of 1,000t/a, and comprehensive

utilization capacity of 28,000 t/a.

Industrial Gases

Linde, a professional gases supplier from

Germany, offers gas service such as

nitrogen, oxygen, hydrogen and argon.

Pipe Rack

Raw materials, products, steam and

industrial gases can be delivered through

the public pipe rack, which is about 10

km.

Fire Fighting

CZBJ has been equipped with an

advanced firefighting station.

Tank Storage

The current capacity is 520,000 m3, of

which 149, 000 m3 are bonded. (Besides,

another 370,000 m3 tank farm is under

construction.) There are around

100,000m3 exclusive solid warehouses

(including 20,000 m3 for hazardous

chemicals).

Land-Level

Land will be leveled to the natural height

before delivered to investors, with

supporting infrastructures connected to

the boundary of the land. Desmond Ng,

MPOC Shanghai

(1) Biomass Industry:

(2) Daily Chemical Industry:

(3) Food Industry:

Changzhou Binjiang Economic

Development Zone (CZBJ) – Gateway

to Palm Bioenergy Investment in China

T

11. MPOC FORTUNE • 11

800

700

600

500

400

300

200

100

0

900

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

CAGR 4%

598 627

655

682 708 732 755 776

Source: KPMG analysis

Palm - based feedstock demand for soap production

CAGR 9%

Palm - based feedstock demand from oleochemicals

for different end-user segments (Non-soap)

64

38

30

33

9

14

15

71

44

33

34

10

14

16

79

50

36

36

12

15

17

87

57

40

37

14

15

18

96

64

45

38

16

15

19

106

71

50

39

18

15

20

115

79

55

40

20

16

21

126

87

62

40

23

16

22350

300

250

200

150

100

50

0

400

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Personal care

Detergents

Plastics

Rubber

Pharma

Processed food

Tobacco

Paint

’000MT

Continued from page 9

Good Potential

for Palm Oleo

Chemicals in India

MARKETInsightsIns g

The below chart shows the potential

CAGR of 4% from 2013-2020 from the

soap segment:

Palm – based feedstock demand from

oleochemicals

Demand of palm-based feedstocks for

oleochemical applications expected to

increase at a CAGR of 5% over FY 13-20

Palm-based feedstock demand from

oleochemicals for different end-user

segments (Non-soap)

Similarly, the below chart shows the

potential for a CAGR of 9% from the

non-soap segments over the same

period:

Based on what was presented, we can

conclude that there is immense potential

for increased usage of palm based

products in the manufacture of oleo

chemicals especially in the non food

sector. Although there are several oleo

manufacturers in India, this sector is one

of the growth sectors and it definitely

offers opportunities for further

investments, including joint ventures.

The newly elected Indian government

promises to be more business friendly

and this bodes well for the development

of Malaysia – India joint business ties

and a new avenue for palm based

products to be marketed in India.

Bhavna, MPOC India.

30

25

20

15

10

5

0

FY08 FY09 FY10 FY11 FY12 FY13 FY20

Country USD Per Year (FY13)

India 0.4

China 1

Per capita consumption – Cosmetic

Source: Analyst reports,

KPMG analysisUSA 37

Cosmetics volume

2 1 1

3

1 1

3 2 1

4

2 1

5

2 1

6

3

1

24

15

6

CAGR 22%

CAGR 25%

Lip paint Face make-up Nail paint

Source: Euromonitor, Analyst Reports,

news articles, KPMG analysis

12. MPOC

Offices

Worldwide

Malaysian Palm Oil Council (MPOC)

2nd Floor Wisma Sawit

Lot 6, SS 6, Jalan Perbandaran

47301 Kelana Jaya, Selangor

Tel: 603-7806 4097

Fax: 603-7806 2272

www.mpoc.org.my

American Palm Oil Council

1010 Wisconsin Av, Suite 307

Washington DC 20007

Tel: +1 (202) 333 0661

Fax: +1 (202) 333 0331

www.americanpalmoil.com

E-mail: kassim@americanpalmoil.com

Contact: Mohd Salleh Kassim

MPOC Africa Regional Office

5 Nollsworth Crescent, Nollsworth Park

La Lucia Ridge Office Estate,

La Lucia 4051, KwaZulu-Natal, South Africa

Tel: +27 (31) 5666 171

Fax: +27 (31) 5666 170

E-mail: kazmi@mpoc.org.za

Postal Address:

P.O.Box 1591

M.E.C.C. 4301, South Africa

Contact: Kamal Azmi

MPOC Bangladesh

62-63 Motijheel Commercial Area,

7th Floor, Amin Court Building,

Dhaka, Bangladesh

Tel: +88 (02) 9571 216

Fax: +88 (02) 9551 836

E-mail: fakhrul@mpoc.org.bd

Contact: Fakhrul Alam

MPOC Shanghai

Shanghai Westgate Mall Co. Ltd.

Room 1610B, 1038 Nanjing Rd. (w)

Shanghai 200041, P. R. China

Tel: +86 (21) 6218 2085 / 6218 2513

Fax: +86 (21) 6218 1125

E-mail: teah@mpoc.org.cn

Contact: Teah Yau Kun

MPOC Pakistan

11 – 3rd Floor, Leeds Centre

Main Boulevard Gulberg, 111 Lahore, Pakistan

Tel: +92 (42) 3571 6600 / 3571 6601

Fax: +92 (42) 3571 6602

E-mail: faisal@mpoc.org.pk

Contact: Faisal Iqbal

MPOC India

S-4, New Mahavir Building, Cumballa Hill Road

Kemps Corner, Mumbai 400 036

Tel: +91 (22) 6655 0755 / 6655 0756

Fax: +91 (22) 6655 0757

E-mail: bhavna@mpoc.org.in

Contact: Bhavna Shah

MPOC Europe Regional Office

31 Avenue Emile Vendervelde

1200 Brussels Belgium

Tel: +32 (2) 7748 860

Fax: +32 (2) 7794 371

E-mail: kumar@mpoc.eu

Contact: Uthaya Kumar

MPOC Moscow

Moscow, 4th Dobrininskiy side-street,

8 BC 'Dobrinya', 1st floor, Office R00-126

Tel : +790 963 520 40

Email: udovenko@mpoc.org.my

Contact: Aleksey Udovenko

MPOC Cairo

3 Gamal E1-Din Afify Street, Nasir City

Zone No.6, 11371 Cairo, Egypt

Tel: +20 (2) 2273 8108

Fax +20 (2) 2273 8106

E-mail: zainuddin@mpocegypt.com

Contact: Zainuddin Hassan

MPOC Istanbul

Guzel Konutlar Sitesi

Dilek Apartment Daire 3

Balmumcu, Besiktas - Istanbul, Turkey

Tel: +90 (212) 2668234

Fax +90 (212) 2668236

E-mail: haznita@mpoc.org.my

Contact: Norhaznita HusinPublisher: Malaysian Palm Oil Council (MPOC)

2nd Floor Wisma Sawit, Lot 6, SS 6,

Jalan Perbandaran, 47301 Kelana Jaya, Selangor

Printed by: Aktiara Corporation Sdn Bhd

1 & 3, Jalan TPP 1/3, Taman Industri Puchong

Batu 12, 47160 Puchong, Selangor

characteristic and property of oil palm makes

it superior compared to other oil crops. On the

field, the Malaysian palm oil industry has

developed good agricultural practices which

include zero burning, zero waste and

integrated pest management which minimise

chemical controls. Oil palm plantations act as

effective carbon sequesters with cumulative

benefits of cultivation to rural population and

the economy. In Malaysia, the oil palm sector

provides employment to approximately

800,000 people while palm oil sector export

revenue registered RM61.36 billion in 2013.

Anthony K. Veerayan & Lim Teck Chaii, MPOC HQ

References

1. Food and Agricultural Organisation of the United

Nations, (FAO) http://faostat3.fao.org/faostat-

gateway/go/to/download/R/RL/E

2. Malaysian Palm Oil Council’s comments on

EPA’s NODA concerning renewable fuels

produced from palm oil under the RFS Scheme

(EPA-HQ-OAR-2011-0542)

3. Meadows Donella H., Meadows Dennis L.

Meadows, Randers Jorgen, Behrens III William

W, ( 1974), The limits to growth, Pan Books Ltd.

U.K.

4. Ministry of Natural Resources & Environment

Malaysia ( 2011). Malaysia Second National

National Communication to the UNFCCC, p.

1115

5. Oil World Annual (Jan – March 2014) ‘Statistics

for 17 Oils and Fats & Biodiesel.

6. Pramod Khosla and Kalyana Sundram, (2010) ‘A

Supplement on Palm Oil – Why? The Journal of

the American College of Nutrition, Vol.29, No.

3(S) pp.237s-239s.

7. van Zutphen, H (2007) The CO² and Energy

Balance of Malaysian Palm Oil, Zwolle,

Netherlands

8. van Zutphen H ( 2008) ‘Comparative LCA

analysis of different edible oils and fats’

International Palm Oil Sustainable Conf., Kota

Kinabalu, Sabah, p. 18

Websites.

1. Clean Development Mechanism - CDM (2014)

https://unfcc.int/kyoto_protocol/ mechanisms/

clean_development_mechanisms/items/2718.p

hp, Accessed on 1 may 2014

2. Glass D. (2013) ‘European Union Renewable

Energy Directive-Advanced Biotechnology for

Biofuels http://dglassassociates.wordpress.

com/2013/01/22/european-union0renewable-en

ergy-directive/, Accessed on 27 may 2014.

3. HSBC Statement on Forestry and Palm Oil

(March 2014) http://www.hsbc.com/~/media/

HSBC-com/citizenship/sustainability/pdf/hsbc-st

atement-on-forest, Accessed on 28 may 2014

4. Renewable Fuel Standards (RFS) – Fuel and

Fuel Additives (2013) http://www.epa.gov/

OTAQ/fuels/renewablefuels, Accessed on 1 may

2014

5. The Hubbert Curve for the whole world,

http://planetforlife.com/oilcrisis/oilpeak.html

Accessed in 28 may 2014

6. The United nations Collaborative Programme on

Reducing Emissions from Deforestation and

Forest degradation in Developing Countries

(2009) http://www.un-redd.org/ AboutUN-REDD

Programme/tabid/102613/Default.aspx,

Accessed on 1 may 2014.

7. Trends in Atmospheric carbon Dioxide (2014)

US Department of Commerce, National Oceanic

and Atmospheric Administration http://www.esrl.

noaa.gov/gmd/ccgg/trends/ Accessed on 28

may 2014.

8. Yusof Basiron, Unjustified & Illogical campaigns

against palm oil (2013) http://www.ceopalmoil.

com/2013/02/unjustified-illogical-campaigns-ag

ainst-palm-oil/, Accessed on 28 may 2014

C

O

M

PLETED

C

O

M

PLETED

Global Food Security

- Leveraging on Palm

Oil for Higher Limit of

Oils & Fats Output

MARKETInsightsIns g

Continued from page 9