Natural Gas - The Growing Relevance : India’s Energy Landscape

•

1 like•818 views

Infraline Energy’s Natural Gas Report highlights about the present Indian Natural Gas Scenario, the pipeline infrastructure in India, the city gas distribution system and their challenges. Also, it covers the Global LNG market and the LNG business catering to the domestic scale. It provides a detailed analysis of the impact of the proposed gas price hike on the end consumers and covers the status of gas pipelines and latest CGD infrastructure. For further details http://www.infraline.com/Reports.aspx?id=272&tlt=Natural-Gas-The-Growing-Relevance--India%E2%80%99s-Energy-Landscape&sl=Business%20Report%20Series

Recommended

Recommended

More Related Content

More from Infraline Energy

More from Infraline Energy (7)

Recently uploaded

Recently uploaded (20)

Natural Gas - The Growing Relevance : India’s Energy Landscape

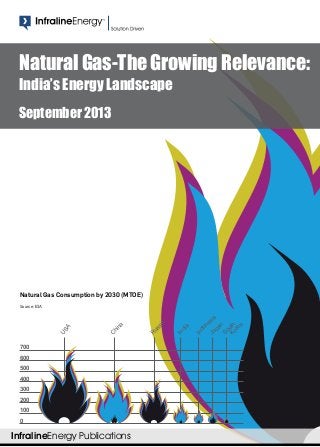

- 1. InfralineEnergy Publications 0 100 300 400 500 600 700 200 U SA C hina R ussia India Japan Indonesia SouthKorea Natural Gas-The Growing Relevance: India’s Energy Landscape September 2013 Natural Gas Consumption by 2030 (MTOE) Source: EIA

- 2. For Sales & Support Charu Agarwal charu.agarwal@infraline.com +91-11-46250023 / 9911032133 For Research & Consulting Anshul Tomar anshul.tomar@infraline.com +91-8586854441 Natural gas is set to play an increasingly important role in the global energy mix. Currently, gas consumption is 24% of the total primary energy consumption globally and global gas demand is projected to increase from 3200 BCM now to 4500 BCM by 2030 thus registering a growth rate of almost 40%. Natural gas production in India in 2012-13 was 105 MMSCMD as compared to total demand of 275 MMSCMD. The total LNG imports in India in 2012-13 were 52 MMSCMD i.e. 26.5% of total gas consumption. The gas demand is expected to increase to 470 MMSCMD by the end of 2017. However, given the domestic gas supplies outlook, sluggish progress with commercial exploitation of unconventional resources; and also, uncertain schedule in transnational pipeline projects it is evident that India will need larger and larger imports of LNG to meet the overall gas demand besides meeting the gas requirements from various sectors. Moreover the recently proposed gas price hike is set to change the dynamics of natural gas business in India. This report entails the current scenario and forecast of natural gas production, exploration and LNG imports in India. It provides a detailed analysis of the impact of the proposed gas price hike on the end consumers. The report extensively covers the status of gas pipelines and latest CGD infrastructure. The report is a ready reference for all the stakeholders in the natural gas business in India. 28 32 35 41 39. 63 87 87 129 150 172 193 215 236 258 86 127 140 126 106 124 149 170 177 209 216 222 229 236 243 196 225 262 279 293 293 371 405 446 473 494 523 552 586 606 81 66 86 110 147 106 135 148 140 114 106 108 108 114 105 0 100 200 300 400 500 600 FY08 FY09 FY10 FY11 FY12 FY12* FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 GasQuantity(MMSCMD) Year LNG Import NG Domestic Production NG Demand Deficit Actual Data Projected Data Natural Gas Demand-Supply Scenario (2008-21) 2012 -13 2013 -14 2014 -15 2015 -16 2016 -17 2017 -18 2018 -19 2019 -20 2020 -21 2021 -22 Imports-Transborder pipelines 0 0 0 0 0 30 30 30 30 30 Imports-LNG 73 101 101 156 184 258 258 258 258 258 Domestic sources 124 149 170 177 210 216 222 229 236 243 Total 197 250 271 333 394 504 510 517 524 531 0 100 200 300 400 500 600 46% 48% 6% 63% 37% 2012-13 2021-22 India’s gas supply mix Projected Gas Availability During 12th and 13th Five-Year Plan Launch Date: Sept 2013 Oil and Gas Key Highlights A must read compendium for all stakeholders in Natural gas business in India Natural gas Demand /Supply outlook in India Operator wise Natural gas Production Cost of gas based power generation vis-a-vis Coal based Impact of gas price hike on: ŠŠ Power Sector ŠŠ Fertilizer Sector ŠŠ CGD Sector CNG vehicles in India City wise price of CNG in India City-wise CNG outlets in India Existing & Planned LNG import terminals Capacity & Length of Gas pipelines in India Evaluation of LNG sourcing options for India US LNG terminals with FTA export authorization US LNG export projects LNG pricing regimes Unconventional sources of natural gas in India Infraline Energy Publications Natural Gas-The Growing Relevance: India’s Energy Landscape September 2013

- 3. Table of Contents 1. Indian Natural Gas Sector – An Overview ŠŠ History of Natural Gas in India ŠŠ Exploration Status in India & Gas Producing Basins ŠŠ Growth of Oil & Gas Reserves ŠŠ Natural Gas Demand and Supply Outlook ŠŠ Natural Gas Production & Consumption ŠŠ LNG imports by India ŠŠ Evolution of domestic natural gas pricing ŠŠ Natural Gas regulatory framework ŠŠ Issues and challenges in Natural gas sector 2. Organization of Gas sector ŠŠ Gas Producers ŠŠ Gas Transporters ŠŠ LNG importers/Suppliers ŠŠ Government Bodies & Regulators ŠŠ End Users 3. Natural Gas Pipeline in India ŠŠ Existing Natural Gas Pipelines in India – Length & Capacity ŠŠ Proposed Natural gas Pipelines ŠŠ Natural Gas Grid Outlook 4. City Gas Distribution in India ŠŠ CGD Business & Infrastructure ŠŠ Use of CNG in transport sector ŠŠ City-wise Price of CNG in India – Pricing Approach ŠŠ Challenges in City gas Distribution in India 5. Global LNG Market ŠŠ Recent Global LNG market updates ŠŠ Demand push for LNG ŠŠ USA/China Heavy LNG Trucks ŠŠ Shipping Fleet – LNG as fuel 6. LNG Business in India ŠŠ Importance of LNG in Indian Context ŠŠ Existing LNG importing terminals in India ŠŠ Planned LNG terminals/facilities and investments ŠŠ Existing LNG supply contracts ( Long & Medium Term) ŠŠ LNG import outlook 7. Future Gas Supply Options for India ŠŠ Domestic gas supply outlook – Conventional ŠŠ Unconventional Natural Gas resources in India ŠŠ Portfolio of LNG Sourcing options ŠŠ Transnational Gas Pipelines – Yet to reach critical mass 8. Economics of Natural Gas in India ŠŠ Economics of gas use in Power sector ŠŠ Economics of gas use in Fertilizer sector ŠŠ Economics of gas transportation for pipeline companies ŠŠ Economics of gas use in CGD companies Infraline Energy Publications Natural Gas-The Growing Relevance: India’s Energy Landscape September 2013

- 4. Payment Details 14th Floor, Atmaram House,1, Tolstoy Road, Connaught Place, New Delhi - 110001, India Tel +91 11 46250023 (D), 46250000, Fax +91 11 46250099 Email charu.agarwal@infraline.com For more details, visit http://store.infraline.com Making the Payment Payment in Indian Rupees (INR): We accept Cheques / Demand Draft. However, we prefer payment through RTGS. Account Name Infraline Technologies India Pvt. Ltd Account Type Current Account Account No. 503011022657 Bank Branch IFSC Code VYSA0005030 Name of Bank ING Vysya Address ING Vysya Bank Ltd. Ground Floor Narain Manzil, Barakhamba Road, New Delhi-110 001 Payment through Cheques / Demand Draft: Payment should be made in favour of ‘Infraline Technologies (India) Private Limited’ through Cheques / DD payable at New Delhi (or ‘at Par’ cheques) and send it to the below mentioned address. For Payments in Foreign Currency Through Wire Transfer: The wire transfer instructions are available at http://www.infraline.com/WireTransferInstructions.htm Through Credit Card: We accept Visa, Master, Amex Cards and all major Net Banking cards. Additional 7% Gateway processing charge applicable along with additional shipping/courier charges. Adani Group,ALSTOM,Avantha Power, J.P. Morgan, Larson &Toubro Ltd, NTPC, Ferranti- Computer- Systems, PricewaterhouseCoopers Pvt. Ltd., Rolls Royce, Shell Gas LPG (India) Pvt. Ltd, Standard Chartered, Tata Power Co. Ltd., Total Oil India Pvt Limited, BALCO, Bharat Petroleum, Cairn Energy, CESC , Deutsche Bank, DLF, DSP Merill Lynch, Ernst&Young, GMR, Goldman Sachs, IDFC, IIM, Indian Oil, Jindal Steel, KPMG, LANCO, McKinsey, MITSUI&Co., Moserbaer, ONGC, PFC , Reliance, SBI Capital, Siemens, BNP Paribas, Suzlon, Torrent Power, Vedanta, VISA Power, YES Bank, Barclays Capital, CERC, Cummins India Ltd., GE capital Ltd., Major Clientele of InfralineEnergy Business Report Series Our Similar Business Report Series Pricing Options Report - Hard Copy (courier charges extra for international clients) INR 80,000 Report - E-copy (Single User License) INR 1,20,000 Report - E-copy (Corporate License) INR 2,40,000 Note: TDS will not be deducted. In case of payments to be made in USD, Euro, GBP , etc., the conversion rates on the date of purchase will be applicable. Shale Gas Exploration in India - Potential, Challenges and Opportunities February 2013 InfralineEnergy Business Research Report Series Dr. V. K. Rao InfralineEnergy Business Report Series Evaluating the Emerging Global LNG Markets Assessing the Impact on LNG Sourcing Options for India July 2012 InfralineEnergy Business Report Series City Gas Distribution in India Demystifying the Opportunity, Growth and Investment Potential November 2011 TM Solution Driven Evaluating the Emerging Global LNG Markets: Assessing the Impact on LNG Sourcing Options for India July 2012 October 2012