Reverse Mortgage Pros and Cons

•

1 like•420 views

http://www.HudReverseMortgageCalculator.com - Find out the pros and cons of getting a reverse mortgage. Are they safe? Will I lose my house? What about my heirs? Do I still own my home? What happens after I die? Can I sell my house if I change my mind? There are definitely pros and cons to getting a reverse mortgage. Each individual's situation and motivation is unique. Only you can decide if a reverse mortgage is right for you...But, you need to know the facts before you can make an informed decision. Speak to a Reverse Mortgage professional today. Get a free consultation and a quote to see how much money you qualify for. 888-269-1098

Recommended

More Related Content

Viewers also liked

Recently uploaded

Recently uploaded (20)

Reverse Mortgage Pros and Cons

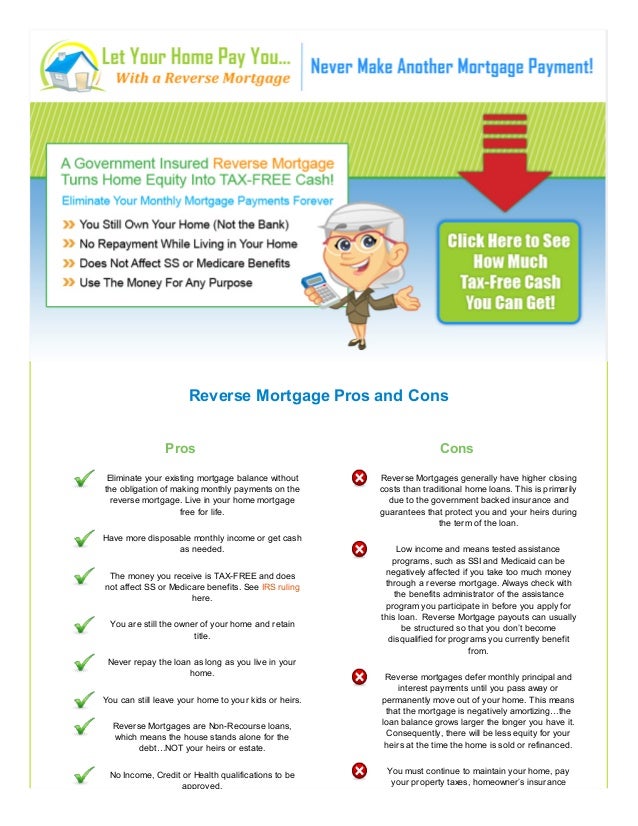

- 1. Reverse Mortgage Pros and Cons Pros Eliminate your existing mortgage balance without the obligation of making monthly payments on the reverse mortgage. Live in your home mortgage free for life. Have more disposable monthly income or get cash as needed. The money you receive is TAX-FREE and does not affect SS or Medicare benefits. See IRS ruling here. You are still the owner of your home and retain title. Never repay the loan as long as you live in your home. You can still leave your home to your kids or heirs. Reverse Mortgages are Non-Recourse loans, which means the house stands alone for the debt…NOT your heirs or estate. No Income, Credit or Health qualifications to be approved. Cons Reverse Mortgages generally have higher closing costs than traditional home loans. This is primarily due to the government backed insurance and guarantees that protect you and your heirs during the term of the loan. Low income and means tested assistance programs, such as SSI and Medicaid can be negatively affected if you take too much money through a reverse mortgage. Always check with the benefits administrator of the assistance program you participate in before you apply for this loan. Reverse Mortgage payouts can usually be structured so that you don’t become disqualified for programs you currently benefit from. Reverse mortgages defer monthly principal and interest payments until you pass away or permanently move out of your home. This means that the mortgage is negatively amortizing…the loan balance grows larger the longer you have it. Consequently, there will be less equity for your heirs at the time the home is sold or refinanced. You must continue to maintain your home, pay your property taxes, homeowner’s insurance

- 2. Home Free Evaluation Safeguards HUD Counseling Do I Qualify Pros and Cons AARP FAQ's Latest News Senior Resources Getting Started Find a Lender Contact Us Copyright © California Reverse Mortgage Privacy Policy|Contact Us|Terms and Conditions approved. Flexible options for receiving your money and can be changed at anytime without penalty. No pre-payment penalties ever. premiums and any HOA dues or assessments if applicable. Some people simply may not be able to keep up with these expenses and could risk foreclosure as a result of these items becoming delinquent. Continue your page here…