A project report on consumer behaviour at uti mutual funds

V.S.GAUTHAMI-PROJECT

1. 1

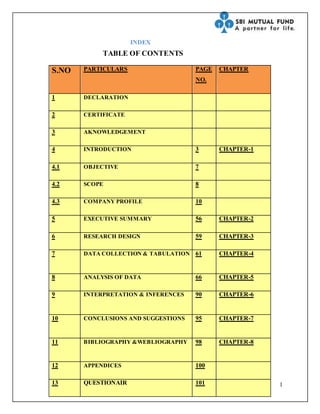

INDEX

TABLE OF CONTENTS

S.NO PARTICULARS PAGE

NO.

CHAPTER

1 DECLARATION

2 CERTIFICATE

3 AKNOWLEDGEMENT

4 INTRODUCTION 3 CHAPTER-1

4.1 OBJECTIVE 7

4.2 SCOPE 8

4.3 COMPANY PROFILE 10

5 EXECUTIVE SUMMARY 56 CHAPTER-2

6 RESEARCH DESIGN 59 CHAPTER-3

7 DATA COLLECTION & TABULATION 61 CHAPTER-4

8 ANALYSIS OF DATA 66 CHAPTER-5

9 INTERPRETATION & INFERENCES 90 CHAPTER-6

10 CONCLUSIONS AND SUGGESTIONS 95 CHAPTER-7

11 BIBLIOGRAPHY &WEBLIOGRAPHY 98 CHAPTER-8

12 APPENDICES 100

13 QUESTIONAIR 101

2. 2

INDEX OF TABLES

S.NO PARTICULARS PAGE

1 MONTHLY INCOME OF RESPONDENT 62

2 NUMBER OF RESPONDENTS WHO R

MARRIED OR UNMARRIED

62

3 NO.OF RESPONDENTS WHO MAKE

INVESTMENTS OR NOT

63

4 TABLE SHOWING WHAT DO AWARED

RESPONDENTS THINK ABOUT THE MUTUAL

FUND

63

5 SOURCE OF INFORMATION OF MUTUAL

FUND

63

6 NUMBER IF INVESTED IN MUTUAL FUND 64

7 PREFERED PORTFOLIOS BY MF

INVESTORS FOR INVESTMENT

64

8 AGE GROUP OF MUTUAL FUND

INVESTORS

64

4. 4

MUTUAL FUND CONCEPT:-

A Mutual Fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is then invested in capital market instruments such as

equities, debentures and other securities. The income earned through these investments and the

capital appreciation realized (after deducting the expenses and profits of mutual fund managers)

is shared by its unit holders in proportion to the number of units owned by them. Thus a Mutual

Fund strives to meet the investment needs of the common man by offering him or her

opportunity to invest in a diversified, professionally managed basket of securities at a relatively

low cost. The small savings of all the investors are put together to increase the buying power and

hire a professional manager to invest and monitor the money. Anybody with an surplus of as

little as a few thousand rupees can invest in Mutual Funds.

WORKING OF MUTUAL FUND:-

A Mutual Fund is a collection of stocks, bonds, or other securities owned by a group of investors

and managed by a professional investment company. For an individual investor to have a

diversified portfolio is difficult. But he can approach to such company and can invest into shares.

Mutual funds have become very popular since they make individual investors to invest in equity

and debt securities easy. When investors invest a particular amount in mutual funds, he becomes

the unit holder of corresponding units. In turn, mutual funds invest unit holders money in stocks,

bonds or other securities that earn interest or dividend. This money is distributed to unit holders.

If the fund gets money by selling some stocks at higher price the unit holders also are liable to

get capital gains.

5. 5

EMERGENCE OF MUTUAL FUND IN INDIA

• Mutual funds in India began in 1964

• Unit Trust of India (UTI) was the first MF company

• Remains the market leader even today, Having about 68% of the

market share

• Lost monopoly in 1987 With entry of public sector mutual funds

Promoted by public sector banks and insurance companies

Industry was open to foreign institutions in 1993

TRENDS OF MUTUAL FUND IN INDIA

• In 1963, finance minister Shri T. Krishnaswami gave the idea of

mutual funds.

• The origin of mutual fund industry in India is with the introduction

of the concept of mutual fund by UTI in the year 1963.

• The first scheme launched by UTI was Unit Scheme in 1964.At the

end of 1988 UTI had Rs.6,700 crores of assets under management.

7. 7

THE OBJECTIVES OF THE STUDY INCLUDE:

To get insight knowledge about Mutual fund.

To evaluate consumer feedback on mutual fund.

To know the awareness of mutual fund among different group of investors

To know the mutual fund performance levels on present markets.

The main objective of this project is concerned with getting the opinion of the people

Regarding the mutual funds and what they feel about availing the services of financial

advisors.

To find out market potential for mutual funds.

To find out the factors, which influence to investing in mutual funds.

To find out attributes investors look for while buying mutual funds.

I have tried to explore the general opinion about the mutual funds.

My work involved interaction with the customers who have invested in mutual funds and also who

have not purchased mutual funds and also to know whether they have invested in mutual funds or

not and also the reasons for their investment / non-investment.

8. 8

SCOPE OF THE STUDY:

This project was conducted so as to understand the concept of Mutual Funds and its usage as an

investment avenue. The study also aims to find out the awareness of mutual funds and its

preference over other investments. The project was undertaken at state bank of India of

Jabalpur city.

Scope of Mutual Funds has grown enormously over the years. In the first age of mutual funds,

when the investment management companies started to offer mutual funds, choices were few.

Even though people invested their money in mutual funds as these funds offered them diversified

investment option for the first time. By investing in these funds they were able to diversify their

investment in common Mutuals, preferred Mutuals, bonds and other financial securities.

At the same time they also enjoyed the advantage of liquidity. With Mutual Funds, they got the

scope of easy access to their invested funds on requirement.But, in today’s world, Scope of

Mutual Funds has become so wide, that people sometimes take long time to decide the mutual

fund type, they are going to invest in. Several Investment

Management Companies have emerged over the years, who offer various types of Mutual Funds,

Each type carrying unique characteristics and different beneficial features. This project may help

the company to make further planning and strategy.

9. 9

INTRODUCTION TO SBIMUTUAL FUND

Company Key Information

Asset Management Company :

SBI Funds Management Pvt. Ltd.

(A Joint Venture between State Bank of India & Société Générale Asset Management)

Setup date Jun-29-1987

Incorporation date Feb-07-1992

Sponsor State Bank of India Trustee SBI Mutual Fund Trustee Company.

10. 10

CORPORATE PROFILE

OUR IDENTITY

With 25 years of rich experience in fund management, we at SBI Funds Management Pvt. Ltd.

bring forward our expertise by consistently delivering value to our investors. We have a strong

and proud lineage that traces back to the State Bank of India (SBI) - India's largest bank. We are

a Joint Venture between SBI and AMUNDI (France), one of the world's leading fund

management companies.

With our network of over 222 points of acceptance across India, we deliver value and nurture the

trust of our vast and varied family of investors.

Excellence has no substitute. And to ensure excellence right from the first stage of product

development to the post-investment stage, we are ably guided by our philosophy of „growth

through innovation‟ and our stable investment policies. This dedication is what helps our

customers achieve their financial objectives.

OUR VISION

“To be the most preferred and the largest fund house for all asset classes, with a

consistent track record of excellent returns and best standards in customer service,

product innovation, technology and HR practices.”

OUR SERVICES

Mutual Funds

Investors are our priority. Our mission has been to establish Mutual Funds as a viable investment

option to the masses in the country. Working towards it, we developed innovative, need-specific

products and educated the investors about the added benefits of investing in capital markets via

Mutual Funds.

11. 11

Today, we have been actively managing our investor's assets not only through our investment

expertise in domestic mutual funds, but also offshore funds and portfolio management advisory

services for institutional investors

This makes us one of the largest investment management firms in India, managing investment

mandates of over 5.4 million investors

Portfolio Management and Advisory Services

SBI Funds Management has emerged as one of the largest player in India advising various

financial institutions, pension funds, and local and international asset management companies.

We have excelled by understanding our investor's requirements and terms of risk / return

expectations, based on which we suggest customized asset portfolio recommendations.

We also provide an integrated end-to-end customized asset management solution for institutions

in terms of advisory service, discretionary and non-discretionary portfolio management services

Offshore Funds

SBI Funds Management has been successfully managing and advising India's dedicated offshore

funds since 1988. SBI Funds Management was the 1st bank sponsored asset management

company fund to launch an offshore fund called 'SBI Resurgent India Opportunities Fund' with

an objective to provide our investors with opportunities for long-term growth in capital, through

well-researched investments in a diversified basket of stocks of Indian Companies.

3. History of Mutual Funds

The mutual fund industry in India started in 1963 with the formation of Unit Trust of India, at the

initiative of the Government of India and Reserve Bank of India. The history of mutual funds in

India can be broadly divided into four distinct phases.

First Phase – 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament. It was set up by the

Reserve Bank of India and functioned under the Regulatory and administrative control of the

Reserve Bank of India. In 1978 UTI was de-linked from the RBI and the Industrial Development

Bank of India (IDBI) took over the regulatory and administrative control in place of RBI. The

first scheme launched by UTI was Unit Scheme 1964. At the end of 1988 UTI had Rs.6, 700

12. 12

Crores of assets under management. Second Phase – 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks and

Life Insurance Corporation of India (LIC) and General Insurance Corporation of India (GIC).

SBI Mutual Fund was the first non- UTI Mutual Fund established in June 1987 followed by

Canbank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89), Indian Bank

Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund (Oct 92). LIC

established its mutual fund in June 1989 while GIC had set up its mutual fund in December

1990. At the end of 1993, the mutual fund industry had assets under management of Rs.47, 004

Crores.

Third Phase – 1993-2003 (Entry of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian mutual fund

industry, giving the Indian investors a wider choice of fund families. Also, 1993 was the year in

which the first Mutual Fund Regulations came into being, under which all mutual funds, except

UTI were to be registered and governed. The erstwhile KotharTempleton) was the first private

sector mutual fund registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and

revised Mutual Fund Regulations in 1996. The industry now functions under the SEBI (Mutual

Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual funds setting

up funds in India and also the industry has witnessed several mergers and acquisitions. As at the

end of January 2003, there were 33 mutual funds with total assets of Rs. 1, 21,805 Crores. The

Unit Trust of India with Rs.44, 541 Crores of assets under management was way ahead of other i

Pioneer (now merged with FranklinTempleton) was the first private sector mutual fund

registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and

revised Mutual Fund Regulations in 1996. The industry now functions under the SEBI (Mutual

Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual funds setting

up funds in India and also the industry has witnessed several mergers and acquisitions. As at the

end of January 2003, there were 33 mutual funds with total assets of Rs. 1, 21,805 Crores. The

Unit Trust of India with Rs.44, 541 Crores of assets under management was way ahead of other

13. 13

Fourth Phase – since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was bifurcated

into two separate entities. One is the Specified Undertaking of the Unit Trust of India with assets

under management of Rs.29, 835 crores as at the end of January 2003, representing broadly, the

assets of US 64 scheme, assured return and certain other schemes. The Specified Undertaking of

Unit Trust of India, functioning under an administrator and under the rules framed by

Government of India and does not come under the purview of the Mutual Fund Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered

with SEBI and functions under the Mutual Fund Regulations. With the bifurcation of the

erstwhile UTI which had in March

2000 more than Rs.76,000 Crores of assets under management and with the setting up of a UTI

Mutual Fund, conforming to the SEBI Mutual Fund.

(STATE BANK OF INDIA) MUTUAL FUND

SBI Mutual Fund is India’s largest bank sponsored mutual fund and has an enviable track

record in judicious investments and consistent wealth creation.

The fund traces its lineage to SBI - India’s largest banking enterprise. The institution has

grown immensely since its inception and today it is India's largest bank, patronised by

over 80% of the top corporate houses of the country.

SBI Mutual Fund is a joint venture between the State Bank of India and Society General

Asset Management, one of the world’s leading fund management companies that

manages over US$ 330 Billion worldwide. In eighteen years of operation, the fund has

launched thirty-two schemes and successfully redeemed fifteen of them. In the process it

has rewarded it’s investors handsomely with consistently high returns.

14. 14

A total of over 3.5 million investors have reposed their faith in the wealth generation

expertise of the Mutual Fund.

Schemes of the Mutual fund have consistently outperformed benchmark indices and have

emerged as the preferred investment for millions of investors and HNI’s.

Today, the fund manages over Rs. 20000 crores of assets and has a diverse profile of

investors actively parking their investments across 40 active schemes.

The fund serves this vast family of investors by reaching out to them through network of

over 100 points of acceptance, 26 investor service centers, 33 investor service desks and

52 district organizers.

SBI Mutual is the first bank-sponsored fund to launch an offshore fund – Resurgent India

Opportunities Fund. Growth through innovation and stable investment policies is the SBI

MF credo.

More about SBI Mutual Fund

The fund traces its lineage to SBI - India’s largest banking enterprise. The institution has

grown immensely since its inception and today it is India's largest bank, patronized by

over 80% of the top corporate houses of the country.

15. 15

KEY PERSONNEL

MANAGEMENT TEAM

Mr. Dinesh Kumar Khara

MD & CEO

Mr.Philippe

Batchevitch

Deputy CEO

Mr. K. T. Ravindran

Executive Director & Chief Operating Officer

Mr. Navneet Munot

Executive Director

& Chief Investment

Officer

Mr. R. S. Srinivas Jain

Executive Director & Chief Marketing Officer (Strategy and International

Business)

Mr. D. P. Singh

Executive Director

& Chief Marketing

Officer (Domestic

Business)

Ms. Aparna Nirgude

Chief Risk Officer

Mr.Rakesh Kaushik

Senior Vice

President (Accounts

& Administration)

Ms. Vinaya Datar

CS & Compliance Officer

Mr. C. A. Santosh

Head - Customer

Service

16. 16

BOARD OF DIRECTORS - AMC

Ms.Arundhati Bhattacharya

Chairman and Associate Director

Mr. Dinesh Kumar Khara

Managing Director & CEO

Mr. Shishir Joshipura

Independent Director

Dr. H. Sadhak

Independent Director

Mrs. Madhu Dubhashi

Independent Director

Dr. H. K. Pradhan

Independent Director

Mr. Jashvant Raval

Independent Director

Mr. Fathi Jerfel

Associate Director

Mr. Thierry Raymond Mequillet

Associate Director

Mr. Philippe Batchevitch

Alternate Director to Mr. Jerfel

TRUSTEES

SBI Mutual Fund Trustee Company Private Limited (the “Trustee”), through its Board of Directors

discharge its obligations as Trustee of the SBI Mutual Fund. The Board of Directors of SBI Mutual

Fund Trustee Company Private Limited are as under:

Shri T.L. Palani Kumar

Independent

Shri C.M. Dixit

Independent

Ms. Sandra Martyres

Associate

Ms. Bharati Rao

Associate

Mr. Krishnamurthy Vijayan

Independent

Mr. Shriniwas Joshi

Independent

17. 17

IMPORTANCE OF SBI MUTUAL FUND

1) SBI Mutual Fund helps in introducing a high degree of professional management and

marketing concept in to banking

2) SBI Mutual Fund creates Healthy competition on general efficiency levels in the industry

3) SBI Mutual Fund is always trying to innovate the new products avenues, new schemes,

services etc.

BUSINESS OBJECTIVES.

The Primary Objective of SBI Mutual Fund is to Enhance the Investments in the country through

the Provision of Different Mutual Fund Schemes in a systematic and Professional Manner, and to

Promote the Investments In the Mutual Fund

Organizational goal

SBI Mutual Fund Main goals are to

a) Develop a Close Relationship with Customer

b) Transform Ideas in to Viable and Creative Solutions

c) Provide Consistently high Returns to Shareholders,

d) To Grow through diversification by leveraging off the existing client base.

Business Focus

SBI Mutual Fund mission is to be world class Mutual Fund its Main aim is to build

Customer Franchises across distinct business So as to be the Preferred Provider of services in the

Segments.

That Fund Operates in and to achieve healthy growth in profitability, and consistency. The SBI

Mutual Fund is committed to maintain the highest level of ethical standards, professional

integrity and regulatory compliance

18. 18

Subsidiaries and Associates

SBI Bank

SBI Mutual Fund

SBI Life insurance Company

SBI Securities

SBI NRI Services

Other Companies co- promoted by SBI

SBI Mutual Fund is professionally managed organization with a board of directors consisting of

eminent persons who represent various fields including finance, taxation, construction and Urban

policy and development. The board primarily focuses on strategy

Formulation, policy and control, designed to deliver increasing value to the share holders

19. 19

THE MUTUAL FUND STRUCTURE

TRUSTEE SPONSOR

AMCOPERATIONS

FUND MANGER

MUTUAL FUND

SCHEMES DISTRIBUTOR

MKT/ SALESMKT/SALES

INVESTOR

SEBI

20. 20

THE STRUCTURE CONSISTS OF

Sponsor - Sponsor is the person who acting alone or in combination with another body corporate

establishes a mutual fund. Sponsor must contribute at least 40% of the net worth of the

Investment Managed and meet the eligibility criteria prescribed under the Securities and

Exchange Board of India (Mutual Funds) Regulations, 1996.The Sponsor is not responsible or

liable for any loss or shortfall resulting from the operation of the Schemes beyond the initial

contribution made by it towards setting up of the Mutual Fund.

Trust - The Mutual Fund is constituted as a trust in accordance with the provisions of the Indian

Trusts Act, 1882 by the Sponsor. The trust deed is registered under the Indian Registration Act,

1908.

Trustee - Trustee is usually a company (corporate body) or a Board of Trustees (body of

individuals). The main responsibility of the Trustee is to safeguard the interest of the unit holders

and inter alia ensure that the AMC functions in the interest of investors and in accordance with

the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996, the provisions of

the Trust Deed and the Offer Documents of the respective Schemes. At least 2/3rd directors of

the Trustee are independent directors who are not associated with the Sponsor in any manner.

Asset Management Company (AMC) - The AMC is appointed by the Trustee as the Investment

Manager of the Mutual Fund. The AMC is required to be approved by the Securities and

Exchange Board of India (SEBI) to act as an asset management company of the Mutual Fund. At

least 50% of the directors of the AMC are independent directors who are not associated with the

Sponsor in any manner. The AMC must have a net worth of at least 10 crore at all times.

Registrar and Transfer Agent - The AMC if so authorized by the Trust Deed appoints the

Registrar and Transfer Agent to the Mutual Fund. The Registrar processes the application form,

redemption requests and dispatches account statements to the unit holders. The Registrar and

Transfer agent also handles communications with investors and updates investor records.

21. 21

The graph indicates the growth of assets over the years:

GRAPH OF AUM OF INDIA vs AUM OF WORLD:-

4. Regulatory Framework

Securities and Exchange Board of India (SEBI)

The Government of India constituted Securities and Exchange Board of India, by an Act of

Parliament in 1992, the apex regulator of all entities that either raise funds in the capital markets

or invest in capital market securities such as shares and debentures listed on stock exchanges.

Mutual funds have emerged as an important institutional investor in capital market securities.

Hence they come under the purview of SEBI. SEBI requires all mutual funds to be registered

with them.

It issues guidelines for all mutual fund operations including where they can invest, what

investment limits and restrictions must be complied with, how they should account for income

and expenses, how they should make disclosures of information to the investors and generally

act in the interest of investor protection. To protect the interest of the investors, SEBI formulates

policies and regulates the mutual funds. MF either promoted by public or by private sector

entities including one promoted by foreign entities are governed by these Regulations. SEBI

approved Asset Management Company (AMC) manages the funds by making investments in

various types of securities. Custodian, registered with SEBI, holds the securities of various

schemes of the fund in its custody. According to SEBI Regulations, two thirds of the directors of

Trustee Company or board of trustees must be independent .Association of Mutual Funds in

22. 22

India (AMFI) With the increase in mutual fund players in India, a need for mutual fund

association in India was generated to function as a non-profit organization. 14

Growth In Asset Under Management

Types of AMCs in Indian Context

The following are the types of AMCs we have in India

AMCs owned by banks

AMCs owned by financial institutions

AMCs owned by the Indian private sector companies

AMCs owned jointly by Indian and foreign investors.

23. 23

DIFFERENT AMCS WORKING IN INDIA ARE

Name of the AMC Nature of Ownership

Alliance Capital Private Foreign

Anagram Wellington Private Indian

Apple Private Indian

Birla Capital International Private Indian

Bank of Baroda Banks

Bank of India Banks

Canbank Investment Banks

Cholamandalam Cazenove Private Foreign

Dundee Private Foreign

DSP Merrill Lynch Private Foreign

Escorts Private Indian

First India Private Indian

GIC Institutions

IDBI Investment Institutions

Indfund Management Ltd. Banks

ING Investment Private Foreign

ITC Threadneedle Private Foreign

RELIANCE Capital Management

Ltd.

Private Indian

Jardine Fleming Private Foreign

Kotak Mahindra Private Indian

Morgan Stanley Private Foreign

Punjab National Bank Banks

Reliance Capital Private Indian

State Bank of India Banks

24. 24

Shriram Private Indian

Sun F&C Private Foreign

Sundaram Newton Private Foreign

Tata Private Indian

Credit Capital Private Indian

Templeton Private Foreign

UTI Institutions

COMPARISON OF MUTUAL FUNDS WITH THE BANKS

Banks v/s Mutual Funds

BANKS MUTUAL FUNDS

Returns Low Better

Administrative exp. High Low

Risk Low Moderate

Investment options Less More

Network High penetration Low but improving

Liquidity At a cost Better

Quality of assets Not transparent Transparent

Interest calculation Minimum balance between

10th.&30th.Of every month

Everyday

Guarantee Max Rs.1 lakh on deposits None

Capital flow in the economy

MFs make it possible for investors to assume risks in the expectation of the higher returns even if

the investor cannot actively manage these investments and the associated risks. This increases

the level of risk capital that is available in the economy for funding enterprise. The MFs also

25. 25

add depth to the security markets where they invest, thus contributing to liquidity and price

discovery.

Schemes and Units

Investment in a company is normally represented by a certain number of shares. People invest in

a company by acquiring its shares; they disinvest by selling its shares. The total outstanding

shares of a company multiplied by the face value of each share, constitutes the share capital of

the company.

What shares are for a company, units are for a mutual fund scheme. Thus investors invest in a

scheme by buying its units. They disinvest by selling its units. The total outstanding units of a

scheme multiplied by the face value of its units, constitutes the unit capital of the scheme.

MUTUAL FUND OPERATION FLOW CHART:-

26. 26

TYPES OF MUTUAL FUND SCHEMES:-

Mutual funds can be done depending upon various factors and variables, such as, maturity

period, investment objectives etc... funds schemes again can be classified into three broad

categories:

equity schemes funds invest in three broad categories of assets—stocks, bonds and cash.

Depending upon the asset mix, mutual Classification of mutual, hybrid schemes, and debt

schemes. However the following are the various types of mutual funds available to the investors.

27. 27

Schemes according to Maturity Period:

A mutual fund can be classified into close-ended or open-ended scheme depending upon its

maturity period:

Open-ended fund/scheme:

An open-ended fund is one that is available for subscription and repurchase on continuous basis.

These schemes do not have a fixed maturity period. Investors can conveniently buy and sell

units at Net Asset Value(NAV) related prices which are declared on a daily basis. The key

feature of open-end scheme is liquidity.

Close-ended fund/scheme:A close-ended scheme has a stipulated maturity period e.g. 5-7

years. The fund is open for subscription only during a specified period at the time of launch of

the scheme.

Schemes according to Investment Objectives:

A scheme can also be classified as growth scheme, income scheme, or balanced scheme

considering its investment objective. Such schemes may be open-ended or close-ended schemes

as described earlier. Such schemes may be classified mainly as follows:

28. 28

Growth or equity oriented Scheme:

The aim of growth funds is to provide capital appreciation over the medium to long term. Such

schemes normally invest a major part of their corpus in equities. Such funds have comparatively

high risk. These schemes provide different options to the investors like dividend option, capital

appreciation etc... and the investors may choose an option depending on their performance. The

investors must indicate the option in the application form. The mutual funds also allow the

investors to change the options at a later date. Growth schemes are good for investors having a

long term outlook seeking appreciation over a period of time.

Income / debt oriented schemes:

The aim of income funds is to provide regular and steady income to investors. Such schemes

generally invest in fixed income securities such as bonds, corporate debentures, Govt. securities

and money market instruments. Such funds are less risky compared to equity schemes. These

funds are not affected because of fluctuations in equity markets. However, opportunities of

capital appreciation are also limited in such funds. The NAVs of such funds are affected because

of change in interest rates in the country. If the interest fall, NAVs of such funds are likely to

increase in the short run and vice-versa. However, long term investors may not bother about

these fluctuations.

Balanced Funds:

The aim of balanced funds is to provide both growth and regular income as such schemes invest

both in equity and fixed income securities in the proportion indicated in their offer document.

These are appropriate for the investors looking for moderate growth. They generally invest 40%

to 60% in equity and debt instruments. These funds are also affected because of fluctuation in

share prices in the stock markets. However, NAVs of such funds are likely to be less volatile

compare to pure equity funds.

Money market or liquid funds:

29. 29

These funds are income funds and their aim is to provide easy liquidity, preservation of capital

and moderate income. These schemes invest exclusively in safer short-term instruments such as

treasury bills, certificates of deposits, commercial paper and inter-bank call money, government

securities, etc. Returns on these schemes fluctuate much less compared to other funds. These

funds are appropriate for corporate and individual investors as a means to park their surplus

funds for short periods.

Gilt funds:

These funds invest exclusively in Govt. securities. Govt. securities have no default risk. NAVs of

these schemes also fluctuate due to change in interest rates and other economic factors as is the

case with income or debt oriented schemes.

Index funds:

Index funds replicate the portfolio of a particular index such as the BSE sensitive index, S&P

NSE-50 index (Nifty) etc. These schemes invest in the securities in the same weightage

comprising of an index. The NAVs of such schemes would rise or fall in accordance with the rise

or fall in the index, though not exactly by same percentage due to some factors known as

“tracking error” in technical terms. Necessary disclosures in this regards are made in the offer

document of the mutual fund scheme.These are also exchange traded index funds launched by

the mutual funds which are traded on the stock exchange.

ELSS:

Equity linked savings scheme (ELSS) are equity funds floated by mutual funds. This scheme is

suited for young people as they have the ability to take on higher risk. The ELSS funds should

invest more than 80 per cent of their money in equity and related instruments. It is ideal to invest

in them when the markets are down. These funds are now open all the year round. The other way

of investing in these funds could be a systematic investment, which essentially means investing a

small sum regularly (monthly or quarterly). It is a market-linked security and therefore there will

be risks accordingly.

30. 30

HOW RISKY YOUR MUTUAL FUND IS:-

Investors always judge a fund by the return it gives, never by the risk it took. In any historical

analysis of a mutual fund, the return is remembered but the risk is quickly forgotten. So a fund

manager may have used very high-risk strategies (that are bound to fail disastrously in the long

run), hoping that his wins will be remembered (as they often are), but the risk he took will soon

be forgotten.

WHAT IS RISK?

Risk can be defined as the potential for harm. But when anyone analyzing mutual funds uses this

term, what is actually being talked about is volatility. Volatility is nothing but the fluctuation of

the Net Asset Value (price of a unit of a fund). The higher the volatility, the greater the

fluctuations of the NAV. Generally, past volatility is taken as an indicator of future risk and for

the task of evaluating mutual fund, this is an adequate (even if not ideal) approximation.

Defining Mutual fund risk:

Mutual funds face risks based on the investments they hold. For example, a bond fund faces

interest rate risk and income risk. Bond values are inversely related to interest rates. If interest

rates go up, bond values will go down and vice versa. Bond income is also affected by the

change in interest rates.

Following Is A Glossary Of Some Risks To Consider When Investing In

Mutual Funds:

CALL RISK:-

The possibility that falling interest rates will cause a bond issuer to redeem or call its high-

yielding bond before the bond's maturity date.

COUNTRY RISK:-

The possibility that political events (a war, national elections), financial problems (rising

inflation, government default), or natural disasters (an earthquake, a poor harvest) will weaken a

country's economy and cause investments in that country to decline.

31. 31

CREDIT RISK:-

The possibility that a bond issuer will fail to repay interest and principal in a timely manner. Also

called default risk.

CURRENCY RISK:-

The possibility that returns could be reduced for Americans investing in foreign securities

because of a rise in the value of the U.S. dollar against foreign currencies. Also called exchange-

rate risk.

INCOME RISK:-

The possibility that a fixed-income fund's dividends will decline as a result of falling overall

interest rates.

INDUSTRY RISK:-

The possibility that a group of stocks in a single industry will decline in price due to

developments in that industry.

INFLATION RISK:-

The possibility that increases in the cost of living will reduce or eliminate a fund's real inflation-

adjusted returns.

INTEREST RATE RISK:-

The possibility that a bond fund will decline in value because of an increase in interest rates.

MANAGER RISK:-

The possibility that an actively managed mutual fund's investment adviser will fail to execute the

fund's investment strategy effectively resulting in the failure of stated objectives.

MARKET RISK:-

The possibility that stock fund or bond fund prices overall will decline over short or even

extended periods. Stock and bond markets tend to move in cycles, with periods when prices rise

and other periods when prices fall.

PRINCIPAL RISK:-

The possibility that an investment will go down in value, or "lose money," from the original or

invested amount.

32. 32

HOW RISK IS MEASURED:-

There are two ways in which you can determine how risky a fund is.

STANDARD DEVIATION:-Standard Deviation is a measure of how much the actual

performance of a fund over a period of time deviates from the average performance.

“Since Standard Deviation is a measure of risk, a low Standard Deviation is good.”

SHARPE RATIO:-

This ratio looks at both, returns and risk, and delivers a single measure that is proportional to the

risk adjusted returns.“Since Sharpe Ratio is a measure of risk-adjusted returns, a high Sharpe

Ratio is good."

HOW TO CHECK THE FUND’S RISK:-

. If you would like to take a look at the latest ratings, click on the relevant month viz March,

April, May .In this rating, each fund is given a star. The funds with a 5-star( )

rating are the best. Those with a 1-star( ) rating are the worst .This star rating is based on risk-

adjusted return. In a very simple way, it gives investors an understanding of whether a fund is

taking an acceptable amount of risk in generating the kind of returns it is doing.

33. 33

Risk Return Matrix in different sources of investments:

THINGS TO BE SEE WHILE INVESTING IN MUTUAL FUNDS:-

1. Don't just look at the NAV, also look at the risk:

2.Higher rating does not mean better returns:

3. Higher rating does not mean more risk:

FREQUENTLY USED TERMS IN MUTUAL FUNDS:-

NET ASSETS VALUE:-

The net asset value, or NAV, is the current market value of a fund's holdings, less the fund's

liabilities, usually expressed as a per-share amount. The public offering price, or POP, is the

NAV plus a sales charge. Open-end funds sell shares at the POP and redeem shares at the NAV,

and so process orders only after the NAV is determined. Closed-end funds (the shares of which

34. 34

are traded by investors) may trade at a higher or lower price than their NAV; this is known as a

premium or discount, respectively.

SALE PRICE:-

Is the price you pay when you invest in a scheme. Also called Offer Price. It may include a sales

load.

REPURCHASE PRICE:-

Is the price at which a close-ended scheme repurchases its units and it may include a back-end

load. This is also called bid Price.

REDEMPTION PRICE:-

Is the price at which open-ended schemes repurchase their units and close-ended schemes

redeem their units on maturity. Such prices are NAV related.

TURNOVER:-

Turnover is a measure of the fund's securities transactions, usually calculated over a year's time,

and usually expressed as a percentage of net asset value. Thus turnover measures the

replacement of holdings.

EXPENSES:-

Mutual funds bear expenses similar to other companies. The fee structure of a mutual fund can

be divided into two or three main components: management fee, non management expense, and

12b-l/non12b-1 fees. All expenses are expressed as a percentage of the average daily net assets

of the fund.

MANAGEMENT FEES:-

Management fee as equal to the contractual advisory fee + the contractual administrator fee.

This "levels the playing field" when comparing management fee components across multiple

funds.

NON-MANAGEMENT EXPENSES:-

Some of the more significant (in terms of amount) non-management expenses are: transfer agent

expenses, custodian expense

, legal/audit expense, fund accounting expense, registration expense, board of directors/trustees

expense and printing and postage expense

35. 35

BROKERAGE/COMMISSIONS:-

Brokerage commissions are directly related to portfolio turnover (portfolio turnover refers to the

number of times the fund's assets are bought and sold over the course of a year). Usually the

higher the rate of the portfolio turnover, the higher the brokerage commissions

12b-I/NON-12b-1 SERVICE FEES:-

12b-1 service fees/shareholder servicing fees are contractual fees which a fund may charge to

cover the marketing expenses of the fund. Non-12b-1 service fees are marketing/shareholder

servicing fees which do not fall under SEC rule 12b-1. in a front-end load or no-load fund, the

12b-1 fees for the fund are usually .

INVESTOR FEES AND EXPENSES:-

Fees and expenses borne by the investor vary based on the arrangement made with the investor's

broker. Sales loads (or contingent deferred sales loads (CDSL) are not included in the fund's total

expense ratio (TER) because they do not pass through the statement of operations for the fund..

Role of Mutual funds in Financial Market

Indian financial institution have played a dominant role in asset formation and intermediation

and contributed substantially in macroeconomic development. In this process of development

Indian Mutual Funds have emerged as a strong financial intermediaries and are playing a very

important role in bringing stability to the financial system and efficiency to resource allocation.

Mutual Fund plays a crucial role in an economy by mobilizing savings and investing them in

the capital market, thus establishing a link between savings and the capital market. The activities

of mutual fund have both short and long term impact on the savings and capital market, and the

national economy. Mutual fund, thus, assist the process financial intermediation. They mobilize

funds in the saving market and act as complimentary to banking, at the same time they also

compete with banks and other financial institutions. In the process stock market activities are

also significant influenced by mutual funds.There is thus hardly any segment of the financial

market, which is not influenced by the existence and operations of mutual funds. However, the

scope and efficiency of mutual funds are influenced by overall economic fundamentals: the inter-

36. 36

relation between the financial and real sector, the nature of development of the savings and

capital markets, market structure, institutional arrangements and overall policy regime.

ADVANTAGES OF INVESTING IN MUTUAL FUNDS

A. Professional Management - The primary advantage of funds is the professional

management of your money. Investors purchase funds because they do not have the time or

the expertise to manage their own portfolio. A mutual fund is a relatively inexpensive way

for a small investor to get a full-time manager to make and monitor investments.

B. Diversification – the idea behind diversification is to invest in a large number of assets so

that a loss in any particular investment is minimized by gains in others.

C. Economies of Scale - Because a mutual fund buys and sells large amounts of securities at a

time, its transaction costs are lower than you as an individual would pay.

D. Liquidity - Open-ended mutual funds are priced daily and are always willing to buy back

units from investors.

E. Regulations - All Mutual Funds are registered with SEBI and they function under strict

guidelines designed to protect the interests of the Investor.

F. Tax benefits

Equity Funds:

Currently, dividends are tax-free in the hands of the investor. There is no distribution tax payable

by the Mutual Fund on dividends distributed. There is no tax deduction at source on dividends as

well. Investments for over 12 months qualify for long term capital gains. Moreover for resident

investors there is no TDS on redemption of the units. The recently introduced Securities

Transaction Tax is applicable to equity fund investments.

37. 37

Debt Funds:

Currently, dividends are tax-free in the hands of the investor. However, there is distribution tax

together with surcharge and education cess, as may be applicable, payable by the Mutual Fund

on dividends distributed. There is no tax deduction at source on dividends as well. Investments

for over 12 months qualify for long term capital gains. For resident investors there is no TDS on

redemption of the units.

LIMITATIONS OF MUTUAL FUNDS

As Mutual Fund provides numerous advantages for investment it has also few limitations that are

listed below:

A) Costs Despite Negative Returns- Investors must pay sales charges, annual fees, and other

expenses regardless of how the fund performs..

B) Lack of Control- Investors typically can’t ascertain the exact make up of a fund’s portfolio at

any given time, nor can they directly influence which securities the fund manager buys and sells

or the timing of those trades.

C) Price Uncertainty- By contrast, with a Mutual Fund, the price at which you purchase or

redeem shares will typically depend on the funds NAV. In general; Mutual Funds must calculate

their NAV at least once every business day, typically after the major U.S. exchange close.

SBI MUTUAL FUND SCHEMES

Magnum COMMA Fund

Magnum Equity Fund

Magnum Global Fund

Magnum Index Fund

Magnum MidCap Fund

Magnum Multicap Fund

Magnum Multiplier Plus 1993

Magnum Sector Funds Umbrella

38. 38

MSFU - FMCG Fund

MSFU - EmergingBusinessesFund

MSFU - IT Fund

MSFU - PharmaFund

MSFU - ContraFund

SBI Arbitrage Opportunities Fund

SBI Blue chip Fund

SBI Infrastructure Fund - Series I

SBI Magnum Taxgain Scheme 1993

SBI ONE India Fund

SBI TAX ADVANTAGE FUND - SERIES I

1. Debt Based Schemes

Debt Funds invest only in debt instruments such as Corporate Bonds, Government Securities and

Money Market instruments either completely avoiding any investments in the stock markets as in

Income funds or gilt Funds or having a small exposure to equities as in Monthly Income Plans or

Children's Plan. Hence they are safer than equity funds. At the same time the expected returns

from debt funds would be lower. Such investments are advisable for the risk.

Magnum Children`s Benefit Plan

Magnum Gilt Fund

o Magnum Gilt Fund (Long Term)

o Magnum Gilt Fund (Short Term)

Magnum Income Fund

Magnum Income Plus Fund

39. 39

o Magnum Income Plus Fund (Saving Plan)

o Magnum Income Plus Fund (Investment Plan)

Magnum Insta Cash Fund

Magnum InstaCash Fund -Liquid Floater Plan

Magnum Institutional Income Fund

Magnum Monthly Income Plan

Magnum Monthly Income Plan Floater

SBI Debt Fund Series

o SDFS 15 Months Fund

o SDFS 90 Days Fund

o SDFS 13 Months Fund

o SDFS 18 Months Fund

o SDFS 24 Months Fund

o SDFS 60 Days Fund

o SDFS 180 Days Fund

SBI Premier Liquid Fund

2. Hybrid Schemes (Balanced scheme)

Magnum Balanced Fund invest in a mix of equity and debt investments. Hence they are less

risky than equity funds, but at the same time provide commensurately lower returns. They

provide a good investment opportunity to investors who do not wish to be completely exposed to

equity markets, but is looking for higher returns than those provided by debt funds.

40. 40

Magnum Balanced Fund

Magnum NRI Investment Fund - FlexiAsset Pl

B. STRUCTURE

Schemes can be classified as Closed-ended or Open-ended depending upon whether they

give the investor the option to redeem at any time (open-ended) or whether the investor has to

wait till maturity of the scheme.

1. Open ended Schemes - The units offered by these schemes are available for sale and

repurchase on any business day at NAV based prices.

2. Closed ended Schemes - The unit capital of a close-ended product is fixed as it makes a

one-time sale of fixed number of units.

3. Interval Schemes - These schemes combine the features of open-ended and closed-

ended schemes. They may be traded on the stock exchange or may be open for sale or

redemption during pre-determined intervals at NAV based prices.

41. 41

SBI MUTUAL FUND SCHEMES

*SBI GOLD FUND

The scheme will predominantly invest in units of SBI GETS which is registered with SEBI and /

or permitted by SEBI from time to time. The investments could be made either directly with the

underlying fund or through the secondary market. The scheme will also invest in money market

instruments. The investment strategy would largely be active in nature. The AMC shall endeavor

that the returns of SBI Gold Fund will replicate the returns generated by the underlying ETF.

Key Benefit

No need to hold or open a DEMAT account.

Liquidity.

Cost Effective.

Assured Purity & Security.

Systematic Investment

Plan (SIP) available.

This product is suitable for investors who are

seeking*:

Long term capital growth

Investments in SBI Gold Exchange Traded Scheme

High risk. (BROWN)

49. 49

Rules prescribed to govern Mutual Funds:

1. All Mutual Funds expect the statutory ones, will have to seek the approval of the SEBI

and the scheme floated by them shall have to be registered with the SEBI.

2. Mutual Funds shall be established in the form of trust under Indian Trust Act to be

operated by separate asset management companies (AMCs) will be authorized by SEBI .

3. SEBI will have the power to withdraw authorization to any AMC if it finds the interest of

investors, Mutual Funds or the capital market are not been served.

4. The AMC and the Trustee of a Mutual Fund should be two separate legal entities and an

AMC or its affiliate cannot act as a manager or any other fund.

5. No person should be director of more than one AMC, nor hold the position of the trustee

of director in trust company of funds operated by the same AMC.

6. Mutual Funds must distribute 90% of their profits in any given year.

7. No Mutual Funds under all its schemes shall hold more than 10% of its fund in the shares

or debentures or other instruments of a single company.

8. No Mutual Funds under all its schemes take together shall invest more than 10% of its

fund in the shares or debentures or other instruments of a single company.

9. No Mutual Funds under all its schemes taken together shall invest more than 15% of its

fund in the shares and debentures of any specific industry, expecting those schemes

which have been floated specifically for investment in one or more specified industries

and a declaration has been made in the offer letter.

10. No individual scheme of Mutual Funds shall invest more than 5% of its corpus in any one

company’s share.

11. Mutual Funds can invest only in transferable securities either in the money market or in

the capital market.

12. Mutual Funds shall be authorized for business by SEBI and registered companies with

sound track records and good reputation could sponsor this.

13. Mutual Funds shall provide continuous liquidity and closed-end scheme shall be listed on

exchange. For open ended schemes, Mutual Funds shall sell or purchase units at

predetermined price based on net asset value, which shall be published at least ones a

week.

50. 50

NAV OF A MUTUAL FUND

Track your investments:

One easy way to keep track of your fund is to keep track of the intelligent investor rankings of

mutual funds, which are complied on a quarterly basis. These rankings allow you to take note of

your funds performance and risk profile and compare it across various time periods as well as

across its peer set,

Net Asset Value (NAV)

The net asset value of the fund is the cumulative market value of the assets fund net of its

liabilities. In other words, if the fund is dissolved or liquidated, by selling off all the assets in the

fund, this is the amount that the shareholders would collectively own. This gives rise to the

concept of net asset value per unit, which is the value, represented by the ownership of one unit

in the fund. It is calculated simply by dividing the net asset value of the fund by the number of

units.

Calculation of NAV

The most important part of the calculation is the valuation of the assets owned by the fund. Once

it is calculated, the NAV is simply the net value of assets divided by the number of units

outstanding. The detailed methodology for the calculation of the asset value is given below:

Asset value is equal to:

Sum of market value of shares/debentures

Liquid assets/cash held, if any

Dividends/interest accrued

Amount due on unpaid assets

Expenses accrued but not paid

Details on the above items

For liquid shares/debentures, valuation is done on the basis of the last or closing market price on

the principal exchange where the security is traded

51. 51

How is the percentage change in NAV calculated?

Percentage change in NAV is an absolute measure of return, which finds the NAV appreciation

between two points, as a percentage. For example, if the NAV of the fund is Rs.23.45 at the

beginning of a year, and Rs. 27.65 at the end of the year, then the percentage change in NAV is

= (27.65-23.45) / 23.45*100

= 17.91%

The general formula is (Absolute change in NAV / NAV at the beginning)* 100

What is the rate of return to an investor in mutual funds?

An investor in mutual fund earns returns from 2 sources:

Income from Dividend paid by the mutual fund.

Capital gains arising out of selling the units at a price higher than the acquisition price.

What is Growth Option?

Investors who do not require periodic income distributions can choose the growth option, where

incomes earned are retained in the investment portfolio, and allowed to grow, rather than being

distributed to the investors.

What is Dividend Option?

Investors, who choose a dividend option on their investment, will receive dividends from the

mutual fund, as and when such dividends are declared. Dividend are paid in the form of

warrants, or directly credited to the investor bank accounts.There are other choices where in the

investor can choose their dividend payout frequencies that can monthly, weekly, daily.

What is re-investment option?

Mutual Funds also provide another option to investors in the form of re-investment. Investors

reinvest the dividends that are declared by the mutual fund, back into the fund itself, at NAV that

is prevalent at the time of re-investment.

52. 52

AN OVERVIEW ON MUTUAL FUNDS COMPANIES IN

INDIA

ABN AMRO Mutual Fund:

ABN AMRO mutual fund is promoted by the ABN AMRO banking group,

Birla Sun Life Mutual Fund:

. Birla Sun Life Asset Management Company Limited, the investment manager of Birla Sunlife

Mutual Fund, is a joint venture between the Aditya Birla Group and Sun Life Financial Services,

Baroda Pioneer Mutual Finds:

Baroda Pioneer Mutual Fund is presently under the management of Baroda Pioneer Asset

Management Company Limited

Hdfc Asset Manageme nt Company Limited (Amc) Functions As An

Asset Management Company For The Hdfc Mutual Fund. Amc Is A Joint Venture Between

Housing Finance Giant Hdfc And British Investment Firm Standard Life Investments Limited

HSBC Mutual Fund:

HSBC is one of the world's leading banking giants and boasts of a 140-year history in banking

services. HSBC operates in more than 70 countries across the globe and has assets of over $1.2

trillion on the consolidated group balance sheet.

ICICI Prudential Mutual Fund:

. The asset management company, Prudential ICICI Asset Management Company Limited, is a

joint venture between Prudential Plc, Europe's leading insurance company and ICICI Bank,

India's premier financial institution. Prudential Plc holds 55 per cent of the asset management

company and the balance by ICICI Bank.

53. 53

State Bank of India Mutual Fund:

SBI Mutual Fund, India's largest bank sponsored mutual fund, is a joint venture between the

State Bank of India and Societe Generale Asset Management, one of the world's top-notch fund

management companies. Since its inception, SBI Funds Management Private Ltd. has launched

thirty-two schemes and successfully redeemed fifteen of them.

ING Vysya Mutual Fund:

ING Vysya mutual fund benefits from the vast international experience and professional

expertise of its promoters the ING Group, Dutch insurance and banking giant. ING, one of

thelargest financial services groups globally, took over the former Vysya Bank in India to form

ING Vysya Bank

Sahara Mutual Fund:Sahara Mutual Fund is sponsored by the

Sahara India Financial Corporation Limited (SIFCL), the flagship company of Sahara India

Group. Incorporated in 1987, SIFCL is the First Residuary Non-Banking Company (RNBC) in

India that has been granted certificate of registration by RBI and is a leading public deposit

mobilization company in the Private sector. ..

Tata Mutual Fund:

Tata mutual fund, set up in 1995, is one of the leading private sector funds in the country and is

promoted by the Tata group. The sponsors of the fund are Tata Sons Limited and Tata

Investment Corporation Limited.

Kotak Mahindra Mutual Fund: . The fund is promoted by Kotak

Mahindra Bank, one of India's leading financial institutions that offer financial solutions ranging

from commercial banking, stock broking, life insurance and investment banking.Kotak Mahindra

mutual fund launched its schemes in December 1998 Kotak Mahindra mutual fund was the first

54. 54

fund house in the country to launch a dedicated gilt scheme investing only in government

securities.

Unit Trust of India Mutual Fund:

The setting up of the Unit Trust of India (UTI) in 1963 heralded the birth of the Indian mutual

fund industry. In 1964, UTI mutual fund launched its flagship scheme US-64 and went on to

become a generic term for the mutual fund sector till the government allowed public sector banks

to start mutual funds in 1987.

Standard Chartered Mutual Fund:

. The bank has a strong brand presence in India and is well entrenched in developing markets of

Asia Pacific region. The sponsor of the fund is Standard Chartered Bank. The AMC of the

fund is Standard Chartered Asset Management Company Private Limited.

Franklin Templeton India Mutual Fund:

Franklin Templeton Investments, global investment management major, started their India

operations in 1996 as Templeton Asset Management India Pvt. Limited

Morgan Stanley Mutual Fund India:

When the Indian mutual fund sector was opened up for foreign investment in 1993, Morgan

Stanley became the first international fund manager to enter India with a domestic mutual fund.

One of the largest investment banks and fund managers in the world, Morgan Stanley operates in

28 countries and has $576 billion in assets under management globally.

Escorts Mutual Fund:

Escorts Mutual Fund is promoted by the business conglomerate Escorts group. Escorts Asset

Management Limited acts as the AMC to the mutual fund.

Alliance Capital Mutual Fund:

. The Trustee is ACAM Trust Company Pvt. Ltd. and AMC, the Alliance Capital Asset

Management India (Pvt) Ltd. with the corporate office in Mumbai.

55. 55

.

Canbank Mutual Fund:

Canara Bank made its foray into the mutual fund sector by establishing the mutual fund arm

Canbank Mutual Fund in December, 1987.

LIC Mutual Fund

Promoted by India's largest life insurer, Life Insurance Corporation of India, LIC mutual fund

was launched on June 19, 1989.

Reliance Mutual Fund

Reliance mutual fund, promoted by the Anil Dhirubhai Ambani (ADAG) group, is one of the

fastest growing mutual funds in India

57. 57

A mutual fund is a scheme in which several people invest their money for a common financial

goal. The collected money invests in the capital market, debt and the money market, which they

earned, is divided based on the number of units which they hold.

The topic of this project is “CUSTOMER AWARENESS TOWARDS MUTUAL FUNDS

SPECIAL REFERENCE TOWARDS SBI MF”. The mutual fund industry in India has seen

dramatic improvements in quantity as well as quality of product and service offerings in recent

years. Along with this project also touches on the aspect of Systematic Investment Plan and

Steps of how to invest in Mutual Fund.

An effort has been made to work on the concepts that have been taught in class along with other

useful parameters so that better study can be done.

As information and awareness are rising more and more people are enjoying benefits of investing

in mutual funds.

The main reason number of retail mutual fund investors remains small is that nine in ten people

with incomes in india do not know that mutual funds exist.

But once people are aware of mutual fund investment opportunities ,the number who decided to

invest in mutual funds increases to many as one in five people The trick for converting a person

with no knowledge of mutual funds to a new mutual fund customer is to understand which of the

potential investors are more likely to buy mutual funds and to use the right arguments in the sale

process that customers will accept as important and relevant their decisions.

This project give me a great learning experience and at the same time it gave me enough scope to

implement any analytical ability .

The analysis and advise presented in this project report is based on market research on the

saving and investment practices of the investors and preferences of the investors for investment

in mutual funds.

58. 58

This report will help to know about the awareness of mutual fund among different group of

investors. To evaluate consumer feedback on mutual fund.

What they think about it, to what level they are ready to take risk are they interested to invest in

mutual fund, and in which AMCs’ they are interested. And help to know the Reasons for not

investing in mutual fund by the investors.

60. 60

RESEARCH METHODOLOGY:

For collecting data, I used Questionnaire and interaction with people. The primary data was

collected through interaction with the people I met, and secondary data was collected from SBI

mutual fund fact sheets, magazines, websites etc..

Sample Frame:

People who have invested in mutual funds and who have not invested in Mutual funds.

Sample size : 80 respondents

Sample Unit :

1. Bank Employees

2. Bank customers

3. Government employees

4. Retired persons

5. Businessmen.

Sampling Method :---- Simple random sampling technique.

“Simple random sampling means every element is selected independently of every other element

and the sample is drawn by a random procedure from a sampling frame.

Tools used for the study:

Graphical Representation

The difficulty faced during the fieldwork was not getting the appointments of the respondents

since they were very busy and some were non-cooperative. Moreover, time limitation was

there.

62. 62

TABLE1 SHOWING MONTHLY FAMILY INCOME OF

RESPONDENTS

TABLE 1

TABLE NO.-1

TABLE 2. NUMBER OF MF INVESTORS WHO ARE MARRIED

OR UNMARRIED

OPTIONS MARRIED UNMARRIED TOTAL

NUMBER OF

RESPONDENTS

51 29 80

MONTHLY

INCOME

NUMBER OF

CUSTOMERS(FREQUENCY)

5000-10000 4

10000-15000 11

15000-20000 9

20000-25000 8

250000-30000 16

30000-35000 10

35000-40000 8

40000 & ABOVE 14

TOTAL 80

63. 63

TABLE 3 NUMBER OF RESPONDENTS WHO MAKE INVESTMENTS

OR WHO DOES NOT

4.TABLE SHOWING WHAT DO AWARED RESPONDENTSTHINK

ABOUT THE MUTUAL FUND

TABLE 4

5.TABLE -5 SHOWING THE SOURCES OF INFORMATION OF

MUTUAL FUND TO AWARED RESPONDENTS

OPTIONS INVEST DO NOT INVEST TOTAL

NUMBER OF

CUSTOMERS

62 18 80

RESONS HIGH

RISK

RETURNS

NOT FIXED

BETTER FOR

INVESTMENT

PAST BAD

EXPERIENCE

TOTAL

NUMBER OF

CUSTOMERS

15 11 9 8 43

SOURCE ADVERTISEMENT PEER

GROUP

FINANCIAL

ADVISORS

BANK TOTAL

AWARED

RESPONDENTS

NUMBER OF

RESPONDENT

5 9 19 10 43

64. 64

6.TABLE.6- NUMBER OF INVESTORS INVESTED IN MUTUAL

FUND

RESPONSE

YES NO TOTAL

NUMBER OF

RESPONDENTS

35 45 80

7.TABLE 7 SHOWING PREFERED PORTFOLIOS BY THE

MUTUAL FUND INVESTORS

DEBT EQUITY LIQUID FMP(FIXEDMATURITY

PLAN)

NUMBER OF

INVESTORS

9 16 7 3

8.TABLE 8 AGE GROUP OF MUTUAL FUND

INVESTORS

AGE GROUP 18-30 30-40 40-50 50&ABOVE TOTAL

NO.OF

INVESTORS

2 8 14 11 35

66. 66

ANALYSIS AND INTERPRETATION OF DATA

RESPONDENTS AGE GROUP

Figure1

INTERPRETATION:

OUT OF 80 RESPONDENTS 20% ARE 18 TO 30 AGE, 30% ARE 30 TO 40 GROUP, 28%

ARE 40 TO 50 AGE GROUP AND REMAINING 23% ARE OF ABOVE 50. SO MUTUAL

FUND COMPANIES SHOULD MORE CONCENTRATE ON YOUNG GENERATION

BECAUSE THEY HAVE LESS RISK ON FAMILY AND THEY WILL INVESTMENT

MORE BECAUSE OF CAREER DEVELOPMENT AND RETIREMENT BENEFITS. AND

ALSO CONCENTRATE ON SENIOR CITIZENS FOR FMP, LIQUID PLANS BECAUSE

THEY NEEDED RISK FREE, SECURED ,AND FOR SHORT TERM PLAN.

18-30,16

30-40,24

40-50,22

50&ABOVE, 18

0

5

10

15

20

25

30

AGE GROUP OF RESPONDENTS

NUMBEROFRESPONDENTSe

18-30

30-40

40-50

50&ABOVE

67. 67

OCCUPATION OF THE RESPONDENTS

FIGURE 2

INTERPRETATION

Out Of 80 Respondents 40% Are In Service ,23 % Are In Business And 14%Professionals and

11% are retired.

68. 68

MONTHLY INCOME GROUPS OF RESPONDENTS

FIGURE 3

FIGURE 3

INTERPRETATION:

IN THE INCOME GROUP OF CUSTOMERS OF 80 RESPONDENTS,20%,THAT IS

INCOME GROUP 25000-30000

69. 69

NUMBER OF RESPONDENTS WHO ARE MARRIED

OR UNMARRIED

FIGURE 4

INTERPRETATION

OUT OF 80 SAMPLES 66% ARE MARRIED AND 34% ARE UN MARRIED.

SO PLANS LIKE CHILD EDUCATION PLAN,PENSION PLANS ETC CAN BE FOCUSED

ON MARRIED PERONS FOR THEIR FINANCIAL PLANNING FOR THEIR BRIGHT

FUTURE THROUGH SIP(SYSTEMATIC INVESTMENT PLAN)

70. 70

NUMBER OF RESPONDENTS WHO MAKE

INVESTMENTS OR WHO DOES NOT

FIGURE.-5

INTERPRETATION

OUT OF 80 SAMPLES 62 PEOPLE MEANS 78%MAKE INVESTMENT AND REST 18

MEANS 22% ,DO NOT MAKE ANY INVESTMENT .THIS SHOWS THERE IS GREAT

SCOPE TO ATTRACT THIS CUSTOMERS TOWARDS THE INVESTMENT IN MUTUAL

FUND PLANS.

0

10

20

30

40

50

60

70

NUMBER OF RESPONDENTS

62

18

NUMBER OF RESPONDENTS WHO HAVE

MADE INVESTMENT OR NOT

( IN ANY OF THE PHYSICAL OR FINANCIAL

ASSETS)

MAKEINVESTMENT

DO NOT MAKE INVESTMENT

71. 71

DIFFERENT KINDS OF INVESTMENTS THE

RESPONDENTS MAKES ON DIFFERENT ASSETS

FIGURE-6

INTERPRETATION

OUT OF 80 SAMPLES 62 PEOPLE MAKE INVESTMENT .SO THESE 62 RESPONDENTS,

MAXIMUM INVESTMENT IS MADE ON FIXED DEPOSITS THAT IS 41% ..THIS SHOWS

CUSTOMERS ARE LESS AWARED TO OTHER AREAS OF INVESTMENT ,AND ALSO

SHOWS THEY ARE MORE PRONE TO RISK FREE AND FIXED INCOME AREAS OF

INVESTMENT

FIXED DEPOSIT

41%

INSURANCE

27%

MUTUAL FUND

14%

GOLD/SILVER

9%

OTHERS

5%

SHAREMARKET

4%

NUMBER OF INVESTMENT MADE IN

DIFFERENT ASSETS

FIXED DEPOSIT

INSURANCE

MUTUAL FUND

GOLD/SILVER

OTHERS

SHAREMARKET

72. 72

RESPONDENTS AWARENESS TOWARDS THE

MUTUAL FUND

FIGURE -7

INTERPRETATION

OUT OF 8O RESPONDENTS 54 % PEOPLE ARE AWARE OF MUTUALFUND AND ITS

OPERATION AND 46% PEOPLE ARE NOT AWARE OF MUTUAL FUND AND ITS

OPERATION.

73. 73

SOURCE OF AWARENESS TOWARDS THE MUTUAL

FUND FOR THE AWARED RESPONDENTS

FIGURE-8

INTERPRETATION

FROM THE ABOVE CHART IT CAN BE INFERRED THAT THE FINANCIAL ADVISOR

IS MOST IMPORTANT SOURCE OF INFORMATION OF MUTUAL FUND .OUT OF 43

RESPONDENTS 46% KNOW ABOUT MUTUAL FUND THROUGH FINANCIAL

ADVISOR AND22%THROUGH BANK ,AND 19% THROUGH PEER GROUPS AND13%

THROUGH ADVERTISEMENTS

0

2

4

6

8

10

12

14

16

18

20

5

9

19

10

SOURCE OF AWARENESS

ADVERTISEMENTS PEER GROUP FINANCIAL ADVISORS BANK

74. 74

RESPONDENTS WHO KNOW ABOUT

SIP(SYSTEMATIC INVESTMENT PLAN)

FIGURE-9

INTERPRETATION

OUT OF 80 RESPONDENTS ,37 (46%) HAVE KNOWLEDGE ABOUT THE SIP PLAN

AND 43(54%) HAVE NOT KNOWLEDGE ABOUT SIP.

75. 75

RESPONDENTS WHO KNOW ABOUT TAX SAVING

PLAN OF MUTUAL FUND

FIGURE-10

INTERPRETATION

OUT OF 80 RESPONDENTS, 38% HAVE KNOWLEDGE ABOUT TAX PLANNING

SCHEME AND 62% HAVE NOT KNOWLEDGE ABOUT TAX PLANNING SCHEME.

76. 76

WHAT DO RESPONSEDENTS THINK ABOUT THE

MUTUAL FUND

FIGURE-11

INTERPRETATION

MOST OF RESPONDENT ABOUT 35% THINK INVESTMENT IN MUTUAL FUND IS

VERY RISKY AND 26% THINK RETURNS IN MF ARE NOT FIXED

TOTAL 43

77. 77

INVESTORS INVESTED IN MUTUAL FUNDS

RESPONSE

YES NO

NUMBER OF

RESPONDENTS

35 45

FIGURE-12 INTERPRETATION

OUT OF 80 PEOPLE 44% HAVE INVESTED IN MUTUAL FUND AND 56% HAVE NOT

INVESTED IN MUTUAL FUND. SO THAT THE POTENTIAL MARKET AVAILABLE FOR

TARGETING IS AROUND 56%.

78. 78

INVESTORS INVESTED IN DIFFERENT ASSETS

MANAGEMENT COMPANY.(AMC)

FIGURE-13

INTERPRETATION

IN JABALPUR CITY MOST THE INVESTORS PREFERED UTI ABOUT 25% INVESTED

IN UTI AND 21% IN SBI MF.16% IN HDFC.

79. 79

PREFERRED PORTFOLIOS BY THE MUTUAL FUND

INVESTORS

FIGURE-14

INTERPRETATION

MUTUAL FUND INVESTORS IN JABALPUR CITY OUT OF 35 ,46% INVESTORS

INVESTED IN EQUITY RELATED PLANS,SO INVESTORS ARE LESS AWARED OF

OTHER PORTFOLIOS,LIKE FMP, LIQUID PLANS,DEBT,MONEY MARKETS

0

2

4

6

8

10

12

14

16

PORTFOLIOS

9

16

7

3

NUMBER OF

CUSTOMERS

PREFERREDPORTFOLIOS BY THE MUTUAL FUND

INVESTORS

DEBT

EQUITY

LIQUID

FMP

80. 80

FACTOR CONSIDERED WHILE INVESTNG IN MUTUAL

FUND BY THE MF INVESTORS

FIGURE-15

INTERPRETATION

MUTUAL FUND INVESTORS CONSIDER RETURNS WHILE INVESTING IN MUTUAL

FUND.40% INVESTORS INVEST IN MF CONSIDERING RETURNS AND 31%

INVESTORS CONSIDER ABOUT THE LIQUIDITY.

81. 81

AGE GROUP OF MUTUAL FUND INVESTORS

FIGURE-16

INTERPRETATION

40% OF MUTUAL FUND INVESTORS BELONG TO AGE GROUP 40-50YEARS .AND

31% BELONG TO 50&ABOVE. YEARS.ONLY 23% BELONG TO 30-40 YEARS, 6%

BELONG TO 18-30.

SO COMPANY MUST FOCUS ON THE YOUNG GENERATION BECAUSE THEY ARE

MORE IN NUMBERS AND THEIR WILL BE MORE POTENTIAL TARGET MARKET FOR

MUTUAL FUND FOR THEIR PRODUCTS LIKE EQUITY ORIENTED SCHEMES.REASON

BEHIND THIS YOUNG INVESTORS CAN BEAR MORE RISK COMPARED TO

50 &ABOVE INVESTORS.

0

2

4

6

8

10

12

14

AGE GROUP

2

8

14

11

18-30

30-40

40-50

50&ABOVE

82. 82

OCCUPATION OF MUTUAL FUND INVESTORS

FIGURE-17

INTERPRETATION

37% OF MUTUAL FUND INVESTORS ARE IN SERVICE SECTORS. AND 28% OF

MUTUAL FUND INVESTORS IN BUSINESS.ONLY 16% ARE INPROFESSIONALS

83. 83

MARITAL STATUS OF MUTUAL FUND INVESTORS

FIGURE-18

INTERPRETATION

77% MF INVESTORS ARE MARRIED ,23% ARE UNMARRIED

0

5

10

15

20

25

30

MARITAL STATUS

27

8

MARRIED

UNMARRIED

84. 84

INCOME GROUP OF MUTUAL FUND INVESTORS

FIGURE-19

INTERPREATION

31% MUTUAL FUND INVESTORS BELONG TO INCOME GROUP Rs 40000 &ABOVE

AND 26% COMES IN INCOME GROUP OF RS 35000-40000.LEAST THAT IS 3% COMES

IN INCOME GROUP OF RS 150000-20000.

0

2

4

6

8

10

12

INCOME OF MUTUAL FUND INVESTORS

1

3

4

7

9

11

NUMBEROFINVESTORS

INCOME OF MUTUAL FUND INVESTORS

15000-20000

20000-25000

25000-30000

30000-35000

35000-40000

40000&ABOVE

85. 85

NUMBER OF RESPONDENTS INTERESTED TO INVEST IN MUTUAL

FUND IN FUTURE

FIGURE-20

INTERPRETATION

70% OF RESPONDENTS INTERESTED TO INVEST IN MF AND 30% ARE NOT

INTERESTED.SO SCOPE OF MUTUAL FUND IS GOOD.SBI MF MUST FOCUS ON THE

RESPONDENTS TO MAKE INVESTMENT IN SBI MF.

86. 86

FIGURE-21

INTERPRETATION

OUT OF 56 INTERESTED RESPONDENTS -38% PERCENT RESPONDENTS ARE READY

TO TAKE ZERO%PERCENT RISK .SO THESE RESPONDENTS MUST EDUCATE

ABOUT THE FMP ,AND DEBT PLAN.29% PERCENT RESPONDENTS ARE READY TO

TAKE 50% RISK THEY MUST GIVEN AWARENESS AND INFORMATION REGARDING

SIP PLANS,OF EQUITY.

87. 87

DIFFERENT AMC’S PREFERED BY REPONDENTS FOR FUTURE

INVESTMENT IN MUTUAL FUNDS

FIGURE-22

INTERPRETATION

OUT 56 INTERESTED RESPONDENTS 27% ARE INTERESTED TO INVEST IN

SBI MF , 20% IN HDFC, 18% IN OTHER AMC,s

88. 88

RESPONDENTS WHO ARE INTERESTED OR NOT INTERESTED TO INVEST IN

SBI MF MUTUAL FUND IN COMING FUTURE

FIGURE-23

INTERCHPRETATION

OUT OF 80 RESPONDENTS 61% RESPONDENTS ARE INTERESTED TO INVEST IN SBI

MF IN FUTURE.

61%

39%

INVESTMENT IN SBI MF

NOT INTERESTED TO INVEST IN

SBI MF

89. 89

FIGURE-24

INTERPRETATION

36% RESPONDENTS ARE NOT INVESTING IN MUTUAL FUND BECAUSE OF NOT

HAVING PROPER KNOWLEDGE AND INFORMATION ABOUT MUTUAL FUND AND

18% NOT INVESTING DUE TO FEAR OF HIGH RISK WHICH IS SUBJECTED TO

MARKET.

21%

36%

14%

11%

18%

REASONS FOR NOT INVESTING IN MUTUAL

FUND

RISK

NOT MUCH KNOWLEDGE

ABOUT THE MF

BAD EXPERIENCE

RETURNS ARE NOT FIXED

ALL OF THE ABOVE

91. 91

OUT OF 8O RESPONDENTS 54 % PEOPLE ARE AWARE OF MUTUALFUND AND

ITS OPERATION AND 46% PEOPLE ARE NOT AWARE OF MUTUAL FUND AND ITS

OPERATION.

OUT OF 80 RESPONDENTS 20% ARE 18 TO 30 AGE, 30% ARE 30 TO 40, 28% ARE

40 TO 50 AND REMAINING 23% ARE OF ABOVE 50. SO MUTUAL FUNDS

SHOULD MORE CONCENTRATE ON YOUNG GENERATION BECAUSE THEY

HAVE LESS RISK ON FAMILY AND THEY WILL INVESTMENT MORE BECAUSE

OF CAREER DEVELOPMENT AND RETIREMENT BENEFITS. AND ALSO

CONCENTRATE ON SENIOR CITIZENS FOR FMP ,LIQUID PLANS BECAUSE THEY

NEEDED RISK FREE ,SECURED ,AND FOR SHORT TERM PLAN.

MOST IMPORTANT SOURCE OF INFORMATION OF MUTUAL FUND .OUT OF 43

AWARED RESPONDENTS .THAT IS46% KNOW ABOUT MUTUAL FUND

THROUGH FINANCIAL ADVISOR AND22%THROUGH BANK ,AND 19% THROUGH

PEER GROUPS AND13% THROUGH ADVERTISEMENTS

OUT OF 80 SAMPLES 62 PEOPLE MAKE INVESTMENT AND REST 18 ,DO NOT

MAKE ANY INVESTMENT IN ANY TYPE OF ASSETS .THIS SHOWS THERE IS

GREAT SCOPE TO ATTRACT THIS CUSTOMERS TOWARDS THE INVESTMENT IN

MUTUAL FUND PLANS

OUT 80 SAMPLES MORE THAN 41% PEOPLE INVEST THEIR INVESTMENTS IN

FIXED DEPOSIT

OUT OF 80 RESPONDENTS ,37 HAVE KNOWLEDGE ABOUT THE SIP PLAN AND

43 HAVE NOT KNOWLEDGE ABOUT SIP

OUT OF 80 PEOPLE 44% HAVE INVESTED IN MUTUAL FUND AND 56% HAVE

NOT INVESTED IN MUTUAL FUND. SO THAT THE POTENTIAL MARKET

AVAILABLE FOR TARGETING IS AROUND 56%.

92. 92

MUTUAL FUND INVESTORS CONSIDER RETURNS WHILE INVESTING IN

MUTUAL FUND.40% INVESTORS INVEST IN MF CONSIDERING RETURNS AND

31% INVESTORS CONSIDER ABOUT THE LIQUIDITY.

31% MUTUAL FUND INVESTORS BELONG TO INCOME GROUP Rs 40000 &ABOVE

AND 26% COMES IN INCOME GROUP OF RS 35000-40000.LEAST THAT IS 3%

COMES IN INCOME GROUP OF RS 150000-20000.

40% OF MUTUAL FUND INVESTORS BELONG TO AGE GROUP 40-50YEARS .AND

31% BELONG TO 50&ABOVE. YEARS.ONLY 23% BELONG TO 30-40 YEARS,6%

BELONG TO 18-30.

SO COMPANY MUST FOCUS ON THE YOUNG GENERATION BECAUSE THEY ARE