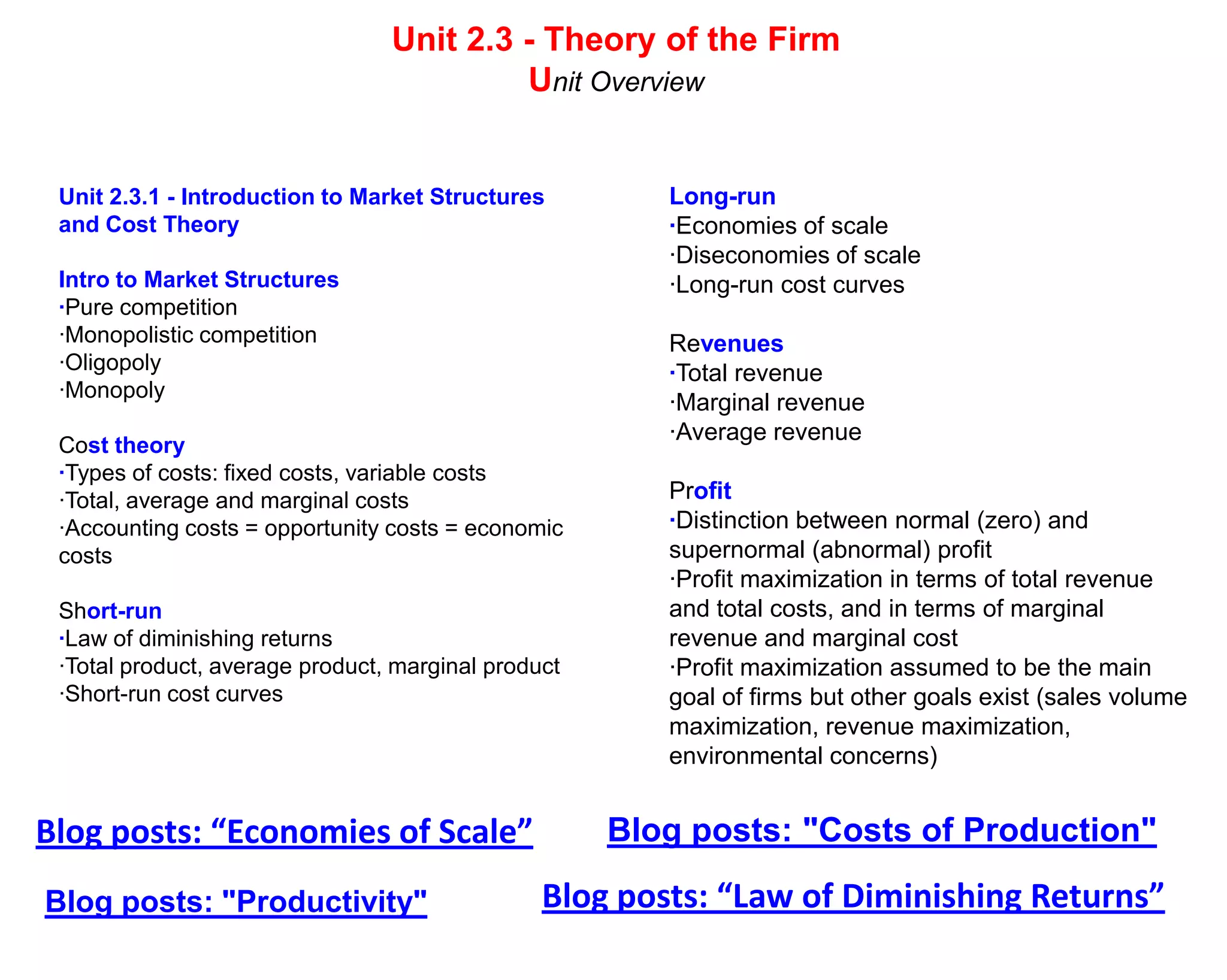

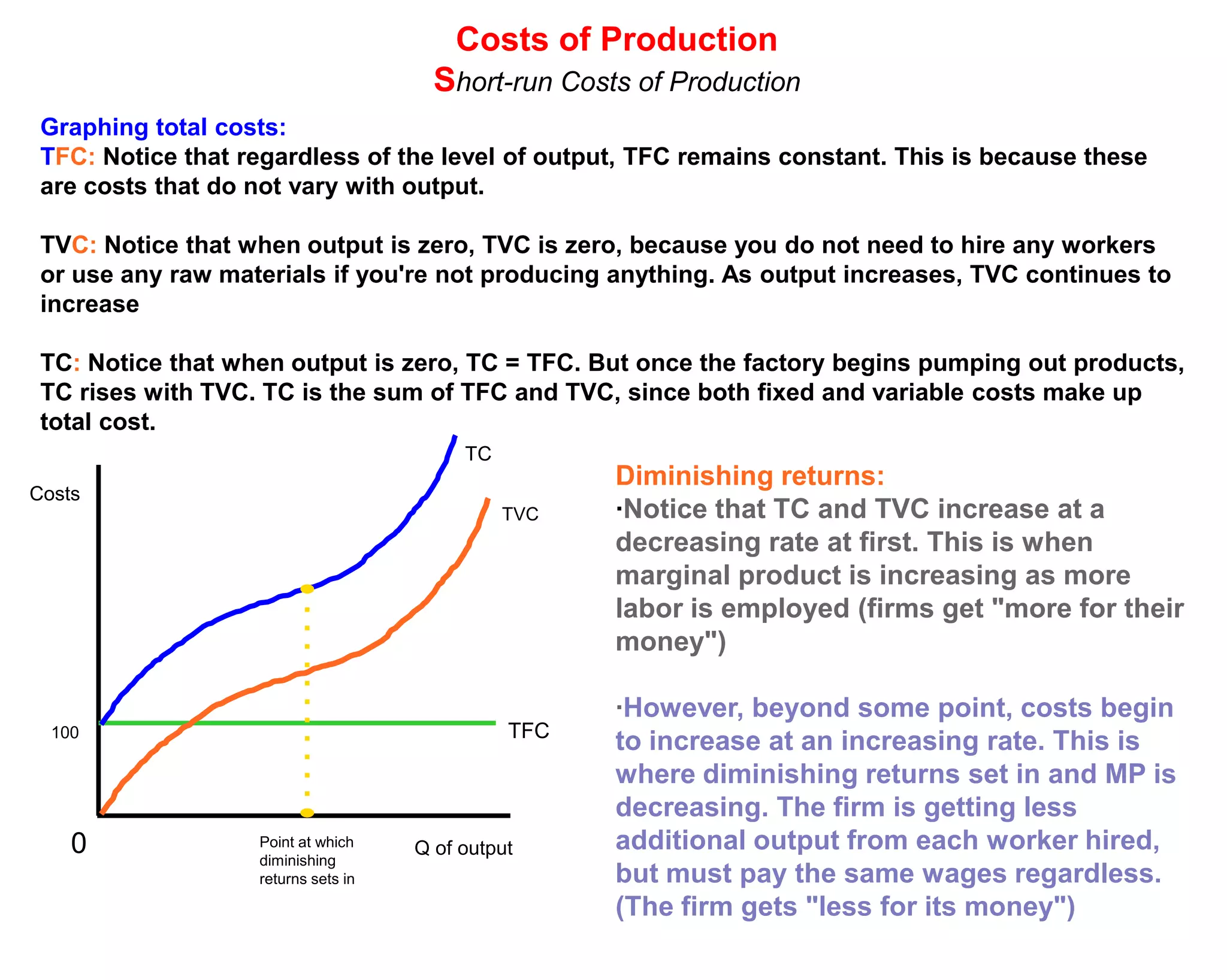

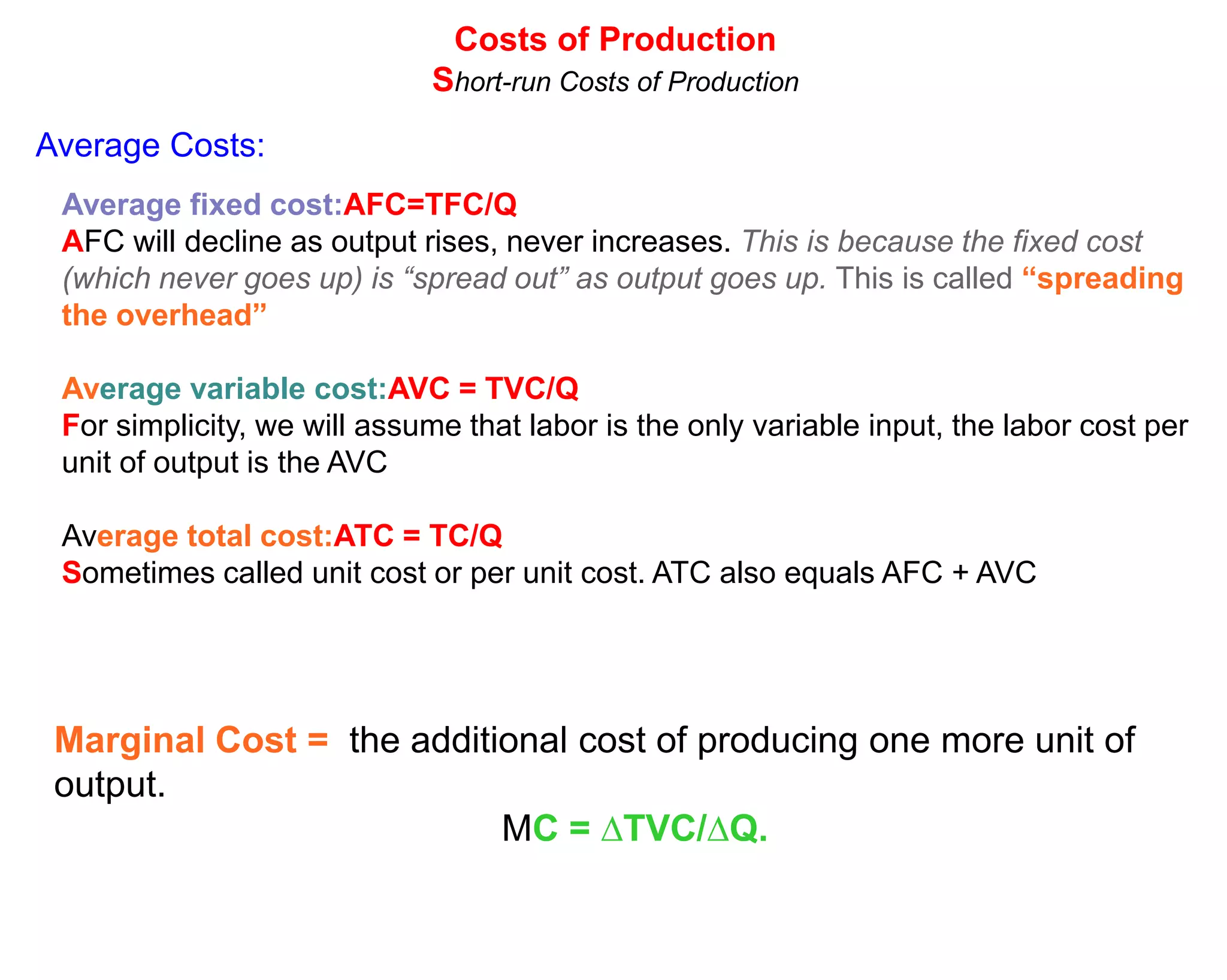

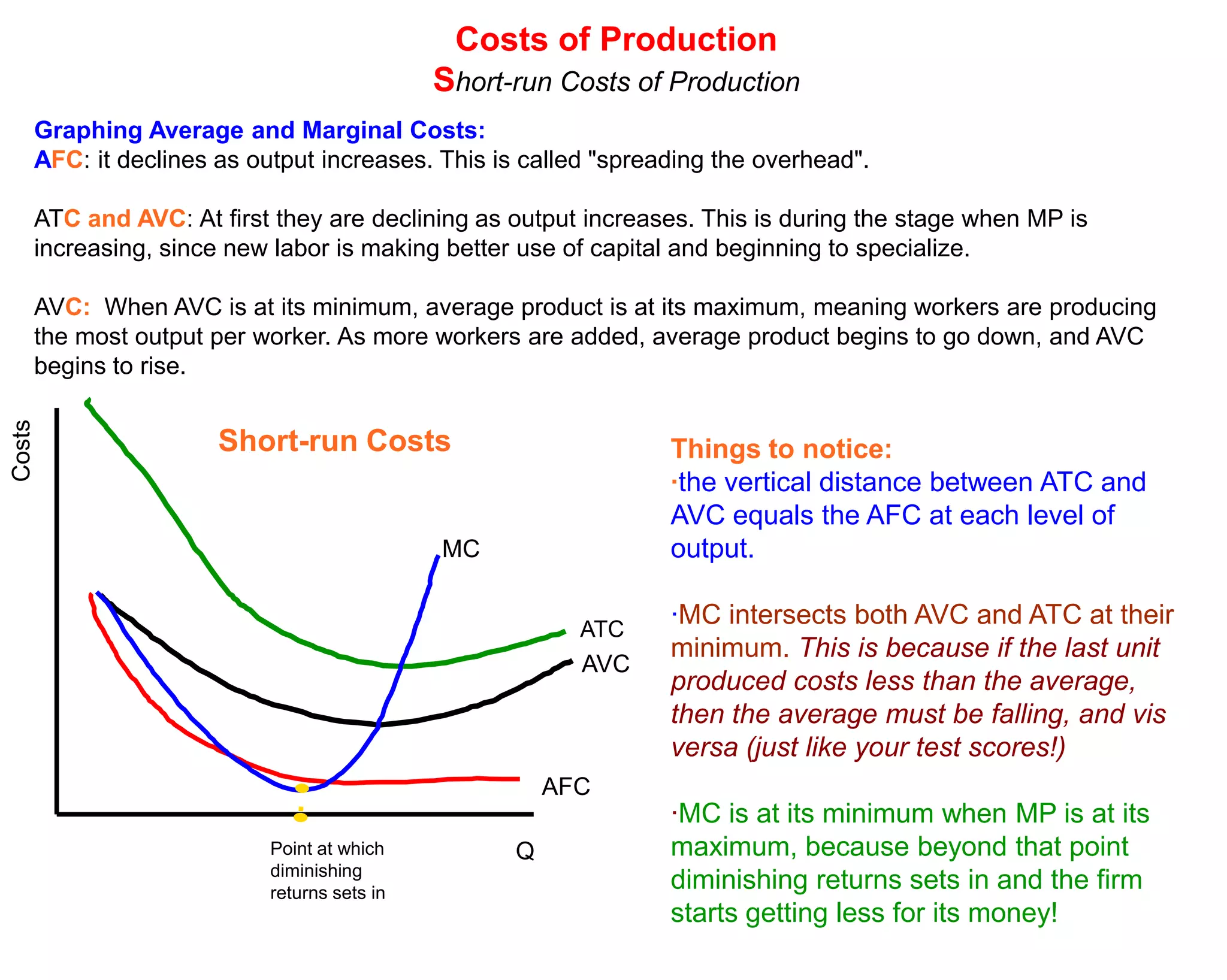

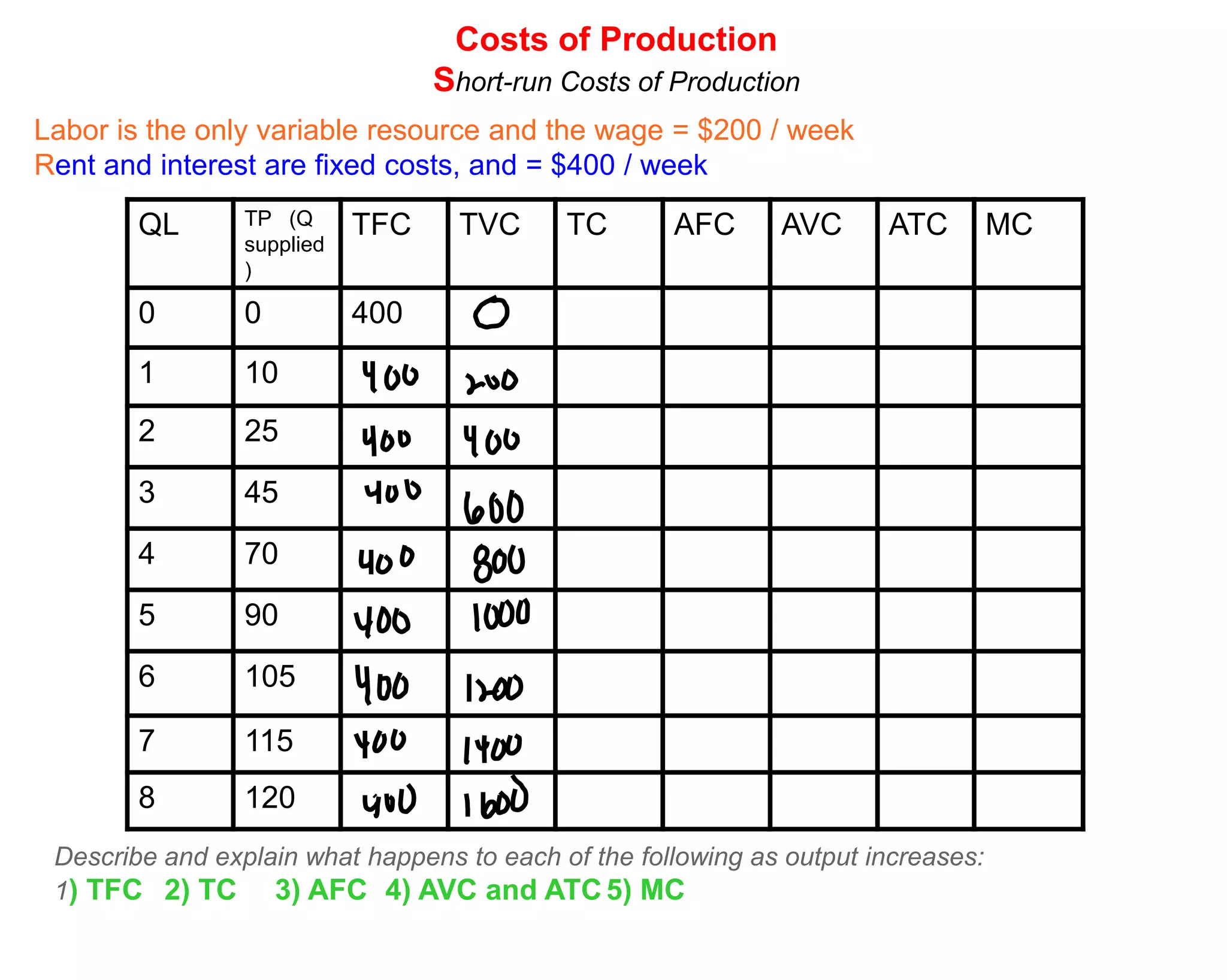

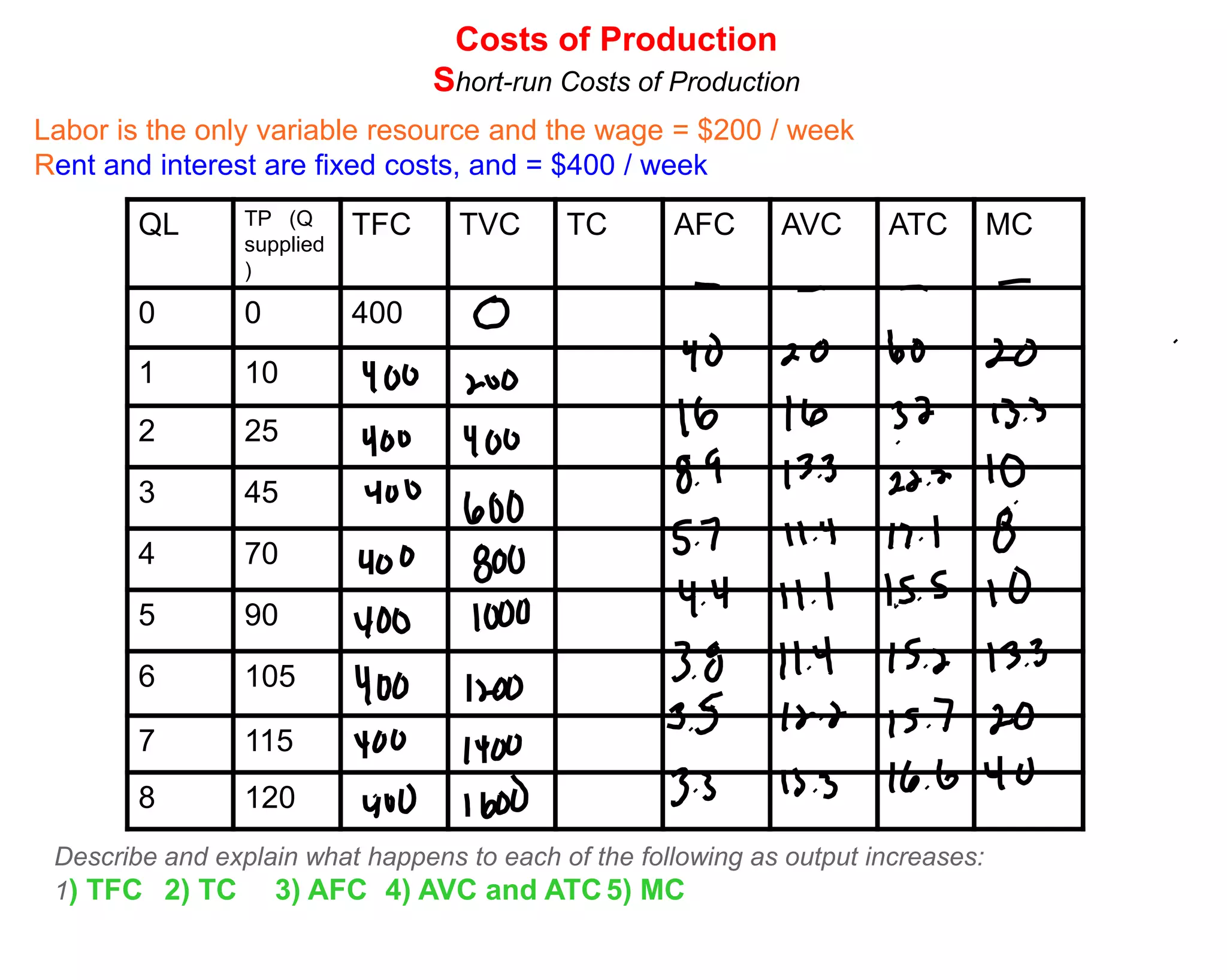

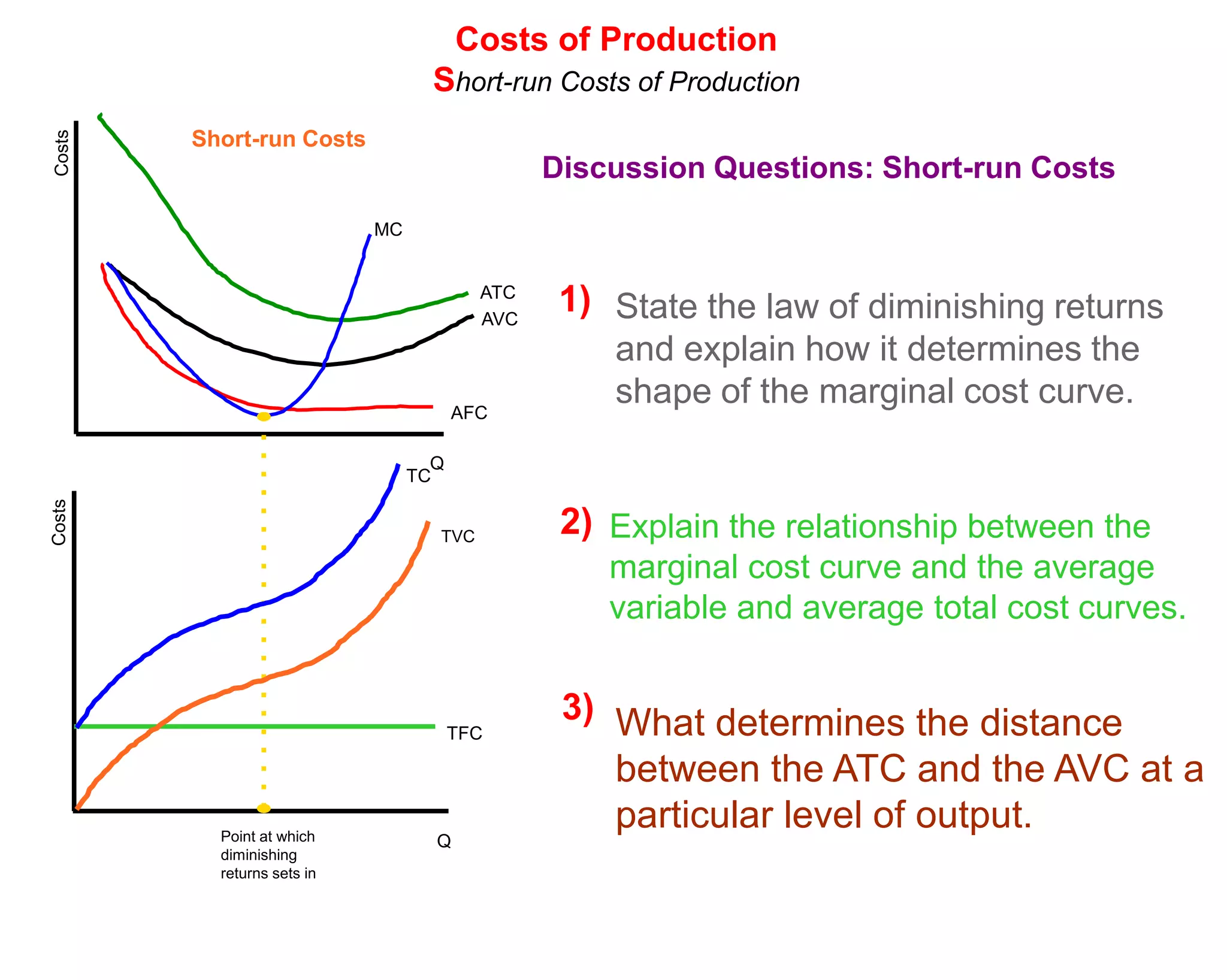

Firms face different costs in the short-run depending on their level of output. Total costs include total fixed costs, which do not vary with output, and total variable costs, which do vary with output. As a firm's output increases, average fixed costs decline due to spreading fixed costs over more units of output. Average variable costs and average total costs initially decline as well, but eventually begin increasing once diminishing returns set in and marginal costs rise. Understanding how costs change with output helps firms maximize profits in the short-run.