Downloaded 57 times

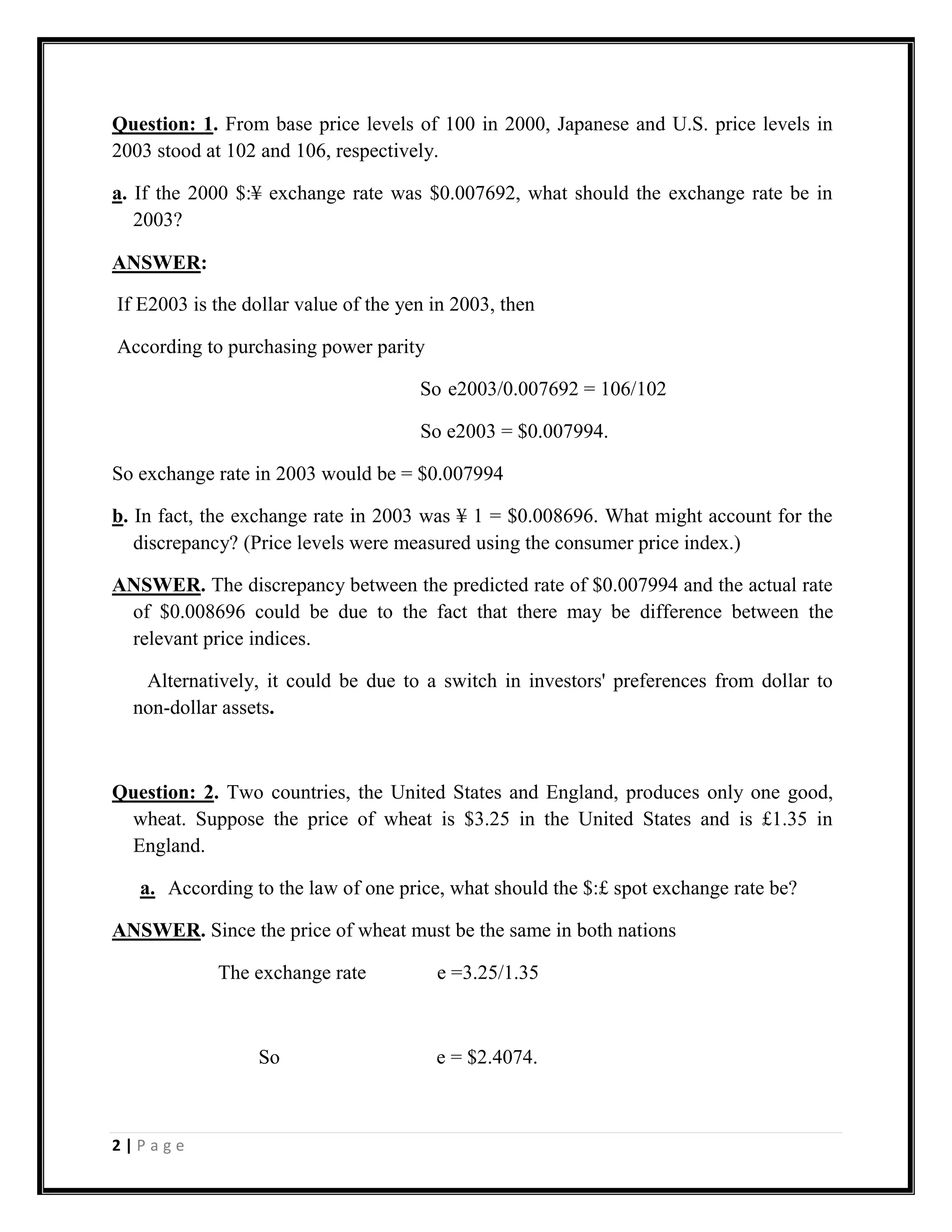

The document contains solutions to 5 questions regarding international finance concepts like purchasing power parity, interest rate parity, and the Fisher effect. Question 1 involves using PPP to calculate the expected exchange rate between the dollar and yen given price level data from 2000 to 2003, with the actual 2003 rate higher possibly due to differences in price indices or investor preferences. Question 2 uses interest rate parity to find the spot $:£ exchange rate balancing wheat prices in the US and UK, and then calculates the 1-year forward rate based on expected future prices. Question 3 applies the Fisher effect formula to find the nominal interest rate given expected inflation of 100% and a real rate of 5%. Questions 4 and

![Ch04[1]parity](https://cdn.slidesharecdn.com/ss_thumbnails/ch041parity-140310222946-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![ch04[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/ch041-240114135454-79dcc99a-thumbnail.jpg?width=640&height=640&fit=bounds)