SOL-MAN-CFAS ANSWERSHEET, ANSWERKEY,

CORRECTANSWER

Bachelor of Secondary Education (St. Luke's College of Medicine - WHQM)

Scan to open on Studocu

Studocu is not sponsored or endorsed by any college or university

SOL-MAN-CFAS ANSWERSHEET, ANSWERKEY,

CORRECT ANSWER

Bachelor of Secondary Education (St. Luke's College of Medicine - WHQM)

Scan to open on Studocu

Studocu is not sponsored or endorsed by any college or university

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

2.

Overview of Accounting

PROBLEM1: TRUE OR FALSE

1. FALSE

2. FALSE - measuring

3. TRUE

4. TRUE

5. FALSE

6. FALSE

7. FALSE

8. TRUE

9. FALSE

10. TRUE

PROBLEM 2: MULTIPLE CHOICE

1. A

2. D

3. B

4. B

5. C

6. C

7. C

8. D

9. C

10. B

PROBLEM 3: MULTIPLE CHOICE

1. D

2. D

3. A

4. B

5. B

6. B

7. E

8. B

9. D

10. B

PROBLEM 4: FOR CLASSROOM DISCUSSION

1. D

2. C

(a) Depreciation necessarily takes into account estimates of

useful life and residual value.

(b) Cost of goods sold may be affected by write-downs of

inventory to net realizable value. NRV is estimated selling

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

3.

price less estimatedcosts of completion and costs to make the

sale. Thus, COGS may be valued by opinion.

(c) Discount on share capital represents the excess of par value

of shares issued over the fair value of the consideration

received. This is valued by fact because it is not affected by

estimates.

(d) Various estimated expenses and income are closed to

retained earnings. Thus, retained earnings is affected by

estimates.

3. D

4. C

5. D

6. D

7. A

8. D

9. A

10. C - equal authority

Conceptual Framework for Financial Reporting

PROBLEM 1: TRUE OR FALSE

1. FALSE – e.g., contributions from, and distributions to, the

entity’s owners result to changes in equity but these do not

result from the entity’s financial performance.

2. FALSE – The qualitative characteristics apply to

information in the financial statements as well as to

financial information provided in other ways.

3. FALSE

4. TRUE

5. FALSE

6. TRUE

7. FALSE

8. FALSE

9. TRUE

10. FALSE – mainly to primary users only and not necessarily

to all external users.

PROBLEM 2: TRUE OR FALSE

1. FALSE

2. TRUE

3. FALSE

4. TRUE

5. TRUE

6. TRUE

7. TRUE

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

4.

8. FALSE –Historical cost may need to be updated for the

asset’s depreciation, impairment, or unwinding of discount

or premium.

9. TRUE

10. TRUE

PROBLEM 3: MULTIPLE CHOICE

1. A

2. A

3. A

4. D

5. D

6. C

7. D

8. A

9. C

10. A

11. D

12. A

13. B

14. C

Explanation: Choices (a) and (b) can affect recognition

decisions about an asset or liability but not necessarily the

existence of the asset or liability.

15. B

PROBLEM 4: MULTIPLE CHOICE

1. A

2. C

3. A

4. D

5. C

6. D

7. D

8. B

9. A

Explanation: Choice (a) is the least accurate statement.

General purpose financial reports are mainly intended for

primary users, and not equally to all types of external

users. For example, a government regulatory agency is

considered an external user but not a primary user.

10. A

PROBLEM 5: FOR CLASSROOM DISCUSSION

1. D

2. D

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

5.

3. C

4. D

5.C

6. A

7. B

8. D

9. A

10. B

11. D

12. A

13. C

14. A

15. D

16. D

Explanations:

Choice (c) is correct. For example, if Entity B delivers the

goods before Entity A pays the purchase price, Entity A will

record the receipt of delivery as debit to ‘Inventory’ or

‘Purchases’ and credit to ‘Accounts payable’ (i.e., a

liability).

Choice (d) is incorrect. If Entity A performs its obligation

first, Entity A’s combined right and obligation changes to

an asset, not a liability. For example, if Entity A pays the

purchase price before Entity B delivers the goods, Entity A

will record the payment as debit to ‘Advances to

suppliers’ (i.e., an asset) and credit to ‘Cash’.

17. D

18. C

19. D

20. D

21. C

22. C

23. D

24. A

25. A

PAS 1 Presentation of Financial Statements

PROBLEM 1: TRUE OR FALSE

1. TRUE

2. TRUE

3. FALSE

4. FALSE

5. FALSE

6. FALSE

7. FALSE

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

6.

8. FALSE

9. FALSE

10.FALSE

PROBLEM 2: MULTIPLE CHOICE

1. A

2. B

3. A

4. A

5. A

6. D

7. D

8. D

9. A

10. B

PROBLEM 3: MULTIPLE CHOICE

1. B

2. A

3. D

4. C

5. A

6. C

7. B

8. C

9. C

10. D

PROBLEM 4: FOR CLASSROOM DISCUSSION

1. A

2. B

3. D

4. A

5. C

6. D

7. A

8. C

9. C

10. B

11. D

PAS 2 Inventories

PROBLEM 1: TRUE OR FALSE

1. FALSE

2. FALSE

3. TRUE

4. FALSE

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

7.

5. TRUE

6. TRUE

7.FALSE

8. TRUE

9. FALSE

10. TRUE

PROBLEM 2: MULTIPLE CHOICE

1. D

2. A

3. C

4. D

5. C

6. A

7. D

8. D

9. A

10.A

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

8.

PROBLEM 3: FORCLASSROOM DISCUSSION

1. C

2. A

Solution:

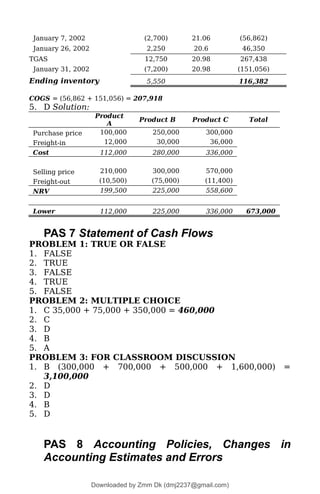

Ending inventory, in units = (3,000 + 2,250 + 10,200 – 2,700 – 7,200) = 5,550

Units Unit cost

Total

cost

Ending inventory in

units 5,550

Allocation to latest

purchases:

Jan. 26 2,250 20.60 46,350

Jan. 6 (balance) 3,300 21.50 70,950

Ending inventory in

pesos 117,300

TGAS (58,650 + 219,300 + 46,350) 324,300

Less: Ending inventory in pesos (117,300)

COGS 207,000

3. C Solution:

Weighted ave. unit

cost

=

TGAS in pesos

TGAS in units

Weighted ave. unit

cost

=

(58,650 + 219,300 + 46,350) = 324,300

(3,000 + 10,200 + 2,250) = 15,450

Weighted ave. unit

cost

= 20.99

Ending inventory in units 5,550

Multiply by: Wtd. Ave. Cost 20.99

Ending inventory in pesos 116,495

TGAS in pesos 324,300

Less: Ending inventory in pesos (116,495)

COGS 207,805

4. B Solution:

Units

Unit

Cost

Total Cost

Balance at January 1, 2002 3,000 19.55 58,650

January 6, 2002 10,200 21.5 219,300

TGAS 13,200 21.06 277,950

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

9.

January 7, 2002(2,700) 21.06 (56,862)

January 26, 2002 2,250 20.6 46,350

TGAS 12,750 20.98 267,438

January 31, 2002 (7,200) 20.98 (151,056)

Ending inventory 5,550 116,382

COGS = (56,862 + 151,056) = 207,918

5. D Solution:

Product

A

Product B Product C Total

Purchase price 100,000 250,000 300,000

Freight-in 12,000 30,000 36,000

Cost 112,000 280,000 336,000

Selling price 210,000 300,000 570,000

Freight-out (10,500) (75,000) (11,400)

NRV 199,500 225,000 558,600

Lower 112,000 225,000 336,000 673,000

PAS 7 Statement of Cash Flows

PROBLEM 1: TRUE OR FALSE

1. FALSE

2. TRUE

3. FALSE

4. TRUE

5. FALSE

PROBLEM 2: MULTIPLE CHOICE

1. C 35,000 + 75,000 + 350,000 = 460,000

2. C

3. D

4. B

5. A

PROBLEM 3: FOR CLASSROOM DISCUSSION

1. B (300,000 + 700,000 + 500,000 + 1,600,000) =

3,100,000

2. D

3. D

4. B

5. D

PAS 8 Accounting Policies, Changes in

Accounting Estimates and Errors

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

10.

PROBLEM 1: MULTIPLECHOICE

1. A

2. B

3. D

4. A

5. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. D

3. A

4. C

5. C

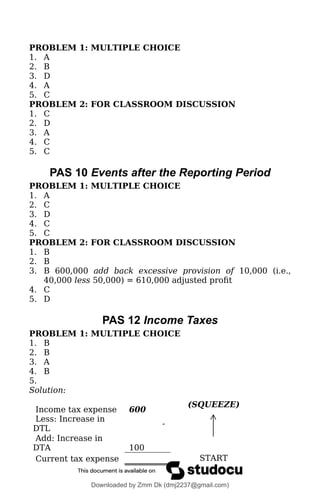

PAS 10 Events after the Reporting Period

PROBLEM 1: MULTIPLE CHOICE

1. A

2. C

3. D

4. C

5. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. B

2. B

3. B 600,000 add back excessive provision of 10,000 (i.e.,

40,000 less 50,000) = 610,000 adjusted profit

4. C

5. D

PAS 12 Income Taxes

PROBLEM 1: MULTIPLE CHOICE

1. B

2. B

3. A

4. B

5.

Solution:

Income tax expense 600

(SQUEEZE)

Less: Increase in

DTL

-

Add: Increase in

DTA 100

Current tax expense START

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

11.

700

6. D

7. A

8.A

9. B

10. C

11. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. B

2. A

3. B

4. A

5. A

PAS 16 Property, Plant and Equipment

PROBLEM 1: MULTIPLE CHOICE

1. D

2. D

3. D

4. D

5. D

6. D

7. D

8. B

9. D

10. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D (800K – 10K + 20K + 40K + 30K + 10K) = 890,000

2. B (890,000 – 90,000) ÷ 10 = 80,000;

890,000 – (80,000 x 2 years) = 730,000

3. C 820,000 fair value – 730,000 carrying amount on

12/31/x2 = 90,000;

(820,000 fair value – 90,000 residual value) ÷ 8 yrs. = 91,250

4. B (1,700,000 x 90%) – 1,900,000 = (370,000)

The revaluation surplus is transferred directly to retained

earnings. Hence, it does not affect the gain or loss on the sale.

PAS 19 Employee Benefits

PROBLEM 1: MULTIPLE CHOICE

1. A

2. C

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

12.

3. A (8Mx 5%) ÷ 6 employees currently employed as at year-

end = 66,667

4. A

5. B

6. C

7. D

8. C

9. C

10.D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D [(20 employees x 1 day x 12 months) – 150 days] x ₱1,000

x 105% = 94,500.

The 20% employee turnover rate is irrelevant because

the employee benefits are monetized.

2. D

3. B Solution: 2,900,000 PV of DBO – 2,600,000 FVPA =

300,000 deficit

4. B Solution: 400,000 service cost + 20,000 net interest (see

computations below) = 420,000

5. C

Solution:

Service cost:

(a) Current service cost 400,000

(b) Past service cost -

(c) Any (gain) or loss on settlement -

400,000

Net interest on the net defined benefit liability (asset):

(a) Interest cost on the DBO (2M, beg. x 10%) 200,000

(b) Interest income on plan assets (1.8M, beg. x 10%) (180,000)

(c) Interest on the effect of the asset ceiling -

20,000

Remeasurements of the net defined benefit liability (asset):

(a) Actuarial (gains) and losses 200,000

(b) Difference between interest income on plan assets

and

60,000

return on plan assets (180,000 – 120,000)

(c) Difference between the interest on the effect of

the asset -

ceiling and change in the effect of the asset ceiling

260,000

Total Defined Benefit Cost 680,000

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

13.

PAS 20 Accountingfor Government Grants and

Disclosure of Government Assistance

PROBLEM 1: MULTIPLE CHOICE

1. B

2. A

3. C

4. D

5. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D

2. C

20x1 = 0, no depreciation yet is recognized from the

building; therefore, no income yet is recognized from

the government grant (i.e., ‘matching’). The building

starts to be depreciated in 20x2.

20x2 = 20,000 (200,000 ÷ 10 years)

3. B Gross presentation: (1M x 9/10) = 900,000;

Net presentation: (1M – 200K) x 9/10 = 720,000

4. A Gross presentation: (1M ÷ 10) = 100,000;

Net presentation: (1M – 200K) ÷ 10 = 80,000

5. A

Foreign Exchange Rates

PROBLEM 1: MULTIPLE CHOICE

1. D

2. A

3. D

4. A

5. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. A [$1,000 x (52 – 50)] = 2,000 gain

2. D [$1,000 x (47 – 52)] = 5,000 loss

3. D

Solution:

(₱10M total assets - ₱5M total liabilities) ÷ ₱10 closing rate =

¥500,000 translated equity

4. A

Solution:

₱3M profit ÷ ₱8 average rate = ¥375,000 translated profit

5. A

Solution:

Translated share capital = (₱2M ÷ ₱5 historical) = ¥400,000

Translated retained earnings (see table below)

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

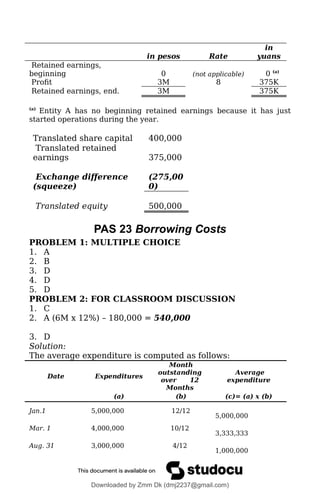

14.

in pesos Rate

in

yuans

Retainedearnings,

beginning 0 (not applicable) 0 (a)

Profit 3M 8 375K

Retained earnings, end. 3M 375K

(a)

Entity A has no beginning retained earnings because it has just

started operations during the year.

Translated share capital 400,000

Translated retained

earnings 375,000

Exchange difference

(squeeze)

(275,00

0)

Translated equity 500,000

PAS 23 Borrowing Costs

PROBLEM 1: MULTIPLE CHOICE

1. A

2. B

3. D

4. D

5. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. A (6M x 12%) – 180,000 = 540,000

3. D

Solution:

The average expenditure is computed as follows:

Date Expenditures

Month

outstanding

over 12

Months

Average

expenditure

(a) (b) (c)= (a) x (b)

Jan.1 5,000,000 12/12

5,000,000

Mar. 1 4,000,000 10/12

3,333,333

Aug. 31 3,000,000 4/12

1,000,000

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

15.

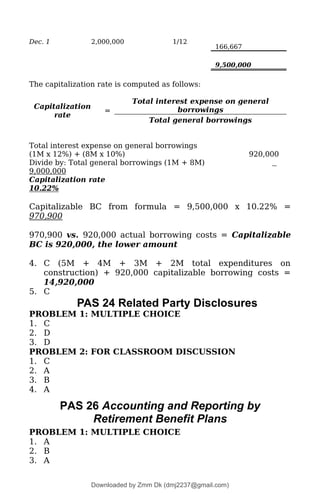

Dec. 1 2,000,0001/12

166,667

9,500,000

The capitalization rate is computed as follows:

Capitalization

rate

=

Total interest expense on general

borrowings

Total general borrowings

Total interest expense on general borrowings

(1M x 12%) + (8M x 10%) 920,000

Divide by: Total general borrowings (1M + 8M)

9,000,000

Capitalization rate

10.22%

Capitalizable BC from formula = 9,500,000 x 10.22% =

970,900

970,900 vs. 920,000 actual borrowing costs = Capitalizable

BC is 920,000, the lower amount

4. C (5M + 4M + 3M + 2M total expenditures on

construction) + 920,000 capitalizable borrowing costs =

14,920,000

5. C

PAS 24 Related Party Disclosures

PROBLEM 1: MULTIPLE CHOICE

1. C

2. D

3. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. A

3. B

4. A

PAS 26 Accounting and Reporting by

Retirement Benefit Plans

PROBLEM 1: MULTIPLE CHOICE

1. A

2. B

3. A

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

16.

4. A

PROBLEM 2:FOR CLASSROOM DISCUSSION

1. D

2. D

PAS 27 Separate Financial Statements

PROBLEM 1: MULTIPLE CHOICE

1. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D

PAS 28 Investments in Associates and Joint

Ventures

PROBLEM 1: MULTIPLE CHOICE

1. B

2. B

3. C

4. A

Solution:

Investment in associate

3/31/x1

500,00

0

Sh. in P (1M x 20% x

9/12)

150,00

0 60,000

Dividends (300K x

20%)

40,000 Sh. in L (200K x 20%

- Dividends

550,00

0 12/31/x2

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

Solution:

Investment in associate

1/1/x1

600,00

0

Sh. in profit (200K x

30%) 60,000 15,000

Dividends (50K x

30%)

645,00

0 12/31/x1

2. B [4M profit – (10M x 5%)] x 20% = 700,000

3. B

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

17.

PAS 29 FinancialReporting in Hyperinflationary

Economies

PROBLEM 1: MULTIPLE CHOICE

1. C

2. B

3. A

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C Building: 900,000 x 150/100 = 1,350,000; The accounts

receivable is not restated because it is a monetary item.

2. A 1,200,000 x 200/180 = 1,333,333

PAS 32 Financial Instruments: Presentation

PROBLEM 1: MULTIPLE CHOICE

1. B

2. B

3. B

4. A

5. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. B

2. D

3. B

Solution:

Issue price 2,600,000

Fair value of debt instrument without equity feature (2M x

102%)

(2,040,0

00)

Equity component

560,00

0

4. D

5. A - Offsetting is not permitted because Entity A does not

intend to settle the financial instruments on a net basis.

PAS 33 Earnings per Share

PROBLEM 1: MULTIPLE CHOICE

1. A

2. C

3. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

Solution:

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

18.

Date No. ofsh.

Months

outstanding

Weighted

average

(a) (b) (c) = (a) x (b)

1/1/20x1 120,000 12/12 120,000

3/1/20x1 42,000 10/12 35,000

9/30/20x1 20,000 3/12 5,000

11/1/20x1 (12,000) 2/12 (2,000)

158,000

Basi

c

EPS

=

Profit (Loss) less Preferred dividends

Weighted average number of outstanding ordinary

shares

Basi

c

EPS

=

2,800,000 – (100,000 x ₱10 x 10%)

158,000

Basic EPS = ₱17.09

2. A [(-1M) – 50K] ÷ 100,000 = -1,050,000 ÷ 100,000 = -10.5

3. C

Solution:

The weighted average number of ordinary shares

outstanding are adjusted retrospectively as follows:

20x1 20x2

1/1 (200,000 x 110% x

2)

440,00

0

(200,000 x 110% x 2 x

12/12)

440,00

0

4/1 (20,000 x 110% x 2 x 9/12) 33,00

0

9/3

0

-

11/

1

-

Weighted average 440,0

00

473,0

00

20x2 20x1

Profit after tax

2,200,00

0

1,800,00

0

Adjusted weighted ave. no. of outstanding

sh. 473,000 440,000

Basic EPS 4.65 4.09

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

19.

4. A

Solution:

Aggregate mkt.value of shares before exercise of rts.

(200,000 sh. x ₱180)

36,000,00

0

Add: Proceeds from exercise of rts. [(200,000 rts. ÷ 5) x

₱120] 4,800,000

Total

40,800,00

0

Divide by: Outstanding shares after exercise of rts.

[200,000 sh. before exercise + (200,000 rts. ÷ 5 rts. per

sh.)] 240,000

Theoretical ex-rights fair value per share 170

Adjustme

nt factor

=

Fair value of stocks immediately before the

exercise of rights

Theoretical ex-rights fair value per share

The adjustment factor is 180/170.

Jan. 1: (200,000 x 180/170 x 4/12)

70,58

8

May. 1: (240,000 x 8/12)

160,0

00

Weighted average no. of outstanding ordinary

shares

230,58

8

Profit for the year

2,900,00

0

Divide by: Weighted average no. of outstanding sh. 230,588

Basic earnings per share

12.5

8

5. C

Solution:

Diluted

EPS

=

Profit (Loss) plus After tax interest expense on

convertible bonds

Weighted average number of outstanding ordinary

shares plus Incremental shares arising from the

assumed conversion or exercise of dilutive potential

ordinary shares

Diluted

EPS

=

800,000 + (2,000,000 x 12% x 70%*)

100,000 + [(2,000,000 ÷ 1,000) x 30]

*70% = 1 – 30% tax rate

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

20.

Diluted EPS =(968,000 ÷ 160,000) = 6.05

PAS 34 Interim Financial Reporting

PROBLEM 1: MULTIPLE CHOICE

1. D

2. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D

2. C

3. B (120,000 x ¼) + (600,000 – 510,000) + (60,000 x ¼) =

135,000

PAS 36 Impairment of Assets

PROBLEM 1: MULTIPLE CHOICE

1. D

2. C

3. C

4. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

Use the following information for the next two questions:

1. A

Solution:

Recoverable amount (higher of FVLCD and VIN)

1,080,0

00

Less: Carrying amount (2,000,000 – 600,000)

(1,400,000

)

Impairment loss (320,000)

2. D Solution:

C.A had no imp. loss been recognized in prior pd.

1,200,00

0*

C.A. at date of reversal (1,080,000 x 5/6) 900,000

Gain on reversal of impairment loss (profit or

loss) 300,000

*Lower than new recoverable amount.

PAS 37 Provisions, Contingent Liabilities and

Contingent Assets

PROBLEM 1: MULTIPLE CHOICE

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

21.

1. D

2. D

3.B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. D

3. C

PAS 38 Intangible Assets

PROBLEM 1: MULTIPLE CHOICE

1. B

2. D

3. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. B

Solution:

Cost 600,000

Residual amount -

Depreciable amount 600,000

Divide by: (Shorter of useful life and remaining legal

life (a)

) 20

Annual amortization expense 30,000

Carrying amount 12/31/x1 = 600,000 – 30,000 = 570,000

2. B (300,000 + 620,000) = 920,000

3. A

PAS 40 Investment Property

PROBLEM 1: MULTIPLE CHOICE

1. C

2. A

3. B

4. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. E

2. D

3. A

4. C (10,000,000 + 10,000 + 30,000 + 25,000) = 10,065,000

5. A

PAS 41 Agriculture

PROBLEM 1: MULTIPLE CHOICE

1. D

2. C

3. D

4. D

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

22.

5. D

PROBLEM 2:FOR CLASSROOM DISCUSSION

1. D

2. C

3. C

4. A

5. D – Choice (a) is incorrect - fair value less costs to sell, not

fair value. Choice (b) is incorrect - gain or loss may arise

from the initial measurement of a biological asset. Choice

(c) is incorrect - agricultural produce is measured at the

lower of cost and NRV in accordance with PAS 2 or some

other applicable standard.

PFRS 1 First-time Adoption of Philippine

Financial Reporting Standards

PROBLEM 1: MULTIPLE CHOICE

1. D

2. C

3. C

4. C

5. B

PROBLEM 2: MULTIPLE CHOICE

1. E

2. C

3. C

4. B

5. D

6. B

7. B

8. D

9. A

Solution:

Accounting:

PFRS principle Application

Advertising costs are

expensed in the period in

which they are incurred, i.e.,

when the advertisement has

been made known to the

public.

Derecognize the deferred

advertising costs and

charge them directly to

retained earnings.

10. A

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

23.

PFRS 2 Share-basedPayment

PROBLEM 1: MULTIPLE CHOICE

1. D

2. D

3. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C (600 x 100 x 100) x 95% x 1/3 = 1,900,000

2. C (600 x 100 x 100) x 94% x 2/3 = 3,760,000 - 1,900,000 =

1,860,000

3. C (600 x 100 x 100) x 95% x 3/3 = 5,700,000 - 3,760,000 =

1,940,000

PFRS 3 Business Combinations

PROBLEM 1: MULTIPLE CHOICE

1. B

2. D

3. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. B

Solution:

Fair value of identifiable assets acquired

excluding

goodwill (4,000,000 total assets – 50,000

goodwill) 3,950,000

Less: Fair value of liabilities assumed

(1,000,00

0)

Fair value of identifiable net assets

acquired 2,950,000

Fair value of identifiable net assets acquired

2,950,0

00

Multiply by: Non-controlling interest (100% - 75%) 25%

NCI’s proportionate share in identifiable net

assets 737,500

Goodwill (Negative goodwill) is computed as follows:

Consideration transferred

2,500,00

0

NCI in the acquire

737,50

0

Previously held equity interest in the acquire -

Total

3,237,50

0

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

24.

Less: Fair valueof identifiable net assets

acquired

(2,950,0

00)

Goodwill

287,5

00

The ₱250,000 transaction costs are expensed. Acquisition-

related costs do not affect the measurement of goodwill.

PFRS 5 Non-current assets Held for Sale and

Discontinued Operations

PROBLEM 1: MULTIPLE CHOICE

1. C

2. A

3. D

4. C

5. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. D

3. C

4. B

5. D

PFRS 6 Exploration for and Evaluation of

Mineral Resources

PROBLEM 1: MULTIPLE CHOICE

1. B

2. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. C

PFRS 7 Financial Instruments: Disclosures

PROBLEM 1: MULTIPLE CHOICE

1. D

2. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. C

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

25.

PFRS 8 OperatingSegments

PROBLEM 1: MULTIPLE CHOICE

1. D

2. C

3. D

4. B

5. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. B

2. C

3. B

Solution:

Revenue test (340,000 threshold: Segments A, B, D and F)

Profit test (86,000 threshold: Segments A, B and F)

Assets test (930,000 threshold: Segments A, B, D, and F)

Reportable segments: A, B, D, and F

PFRS 9 Financial Instruments

PROBLEM 1: MULTIPLE CHOICE

1. A

2. B

3. B

4. B

5. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. A

2. C

3. D

Statements

PROBLEM 1: MULTIPLE CHOICE

1. C

2. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. A

Solution:

Entity A Entity B

Consolidat

ed

Cash in bank 12,000 6,000 18,000

Accounts rec. 36,000 14,400 50,400

Inventory 48,000 27,600

(48K +

37.2K) 85,200

Inv. in sub. 90,000 - eliminated -

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

26.

Building, net 216,00048,000

(216K +

57.6K) 273,600

Goodwill given 3,600

Total assets 402,000 96,000 430,800

Accounts

payable

60,000 7,200

67,200

Share capital 204,000 60,000

parent's

only 204,000

Share

premium

78,000 -

parent's

only 78,000

Retained

earnings 60,000

28,800

parent's

only 60,000

NCI in net

assets

given

21,600

Total liab. &

equity

342,000 96,000 430,800

2. D 204,000 + 78,000 + 60,000 + 21,600 (see table above) =

363,600

PFRS 11 Joint Arrangements

PROBLEM 1: MULTIPLE CHOICE

1. C

2. A – the joint arrangement is a joint venture. Accordingly,

Tech Co. will use the equity method to account for its

investment in Mecha Co.

3. B

4. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. A

2. C

3. B - 1M own sales + (400K x 50% share in JO’s sales) =

1.2M

4. B - 1M + (1M x 50%) – (600K x 50%) = 1.2M

PFRS 12 Disclosure of Interests in Other Entities

PROBLEM 1: MULTIPLE CHOICE

1. D

2. D

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

27.

PROBLEM 2: FORCLASSROOM DISCUSSION

1. D

2. A

PFRS 13 Fair Value Measurement

PROBLEM 1: MULTIPLE CHOICE

1. D

2. D

3. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. A

2. C

3. B (130,000 – 10,000) = 120,000

4. D

Solution:

The “most advantageous market” is determined as follows:

Active Market

#1

Active Market

#2

Quoted price 130,000 135,000

Transport costs (10,000) (12,000)

Costs to sell (2,000) (3,000)

Net sale

proceeds 118,000 120,000

The fair value is computed as follows:

135,000 price in active market #2 – 12,000 transport costs =

123,000

PFRS 14 Regulatory Deferral Accounts

PROBLEM 1: MULTIPLE CHOICE

1. C

2. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. D

PFRS 15 Revenue from Contracts with

Customers

PROBLEM 1: MULTIPLE CHOICE

1. A

2. A – Contract 3 is a lease. It will be accounted for under

PFRS 16, rather than PFRS 15.

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

28.

3. A

4. D

5.B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

2. D

3. D

4. C

5. D

6. A

7. A

8. D

PROBLEM 1: MULTIPLE CHOICE

1. C

2. B

3. C - Choice (d) is incorrect. Under a sublease, the lessee is

also the lessor of the same leased asset.

4. C

5. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. B

Solution:

Fixed payments 220,000

Multiply by: PV of an ordinary annuity of ₱1

@10%, n=4 3.16987

Lease liability 697,371

2. A

Solution:

Cost of right-of-use asset 697,371

Divide by: Lease term (shorter) 4

Annual depreciation 174,343

Since the lease contract neither provides for the transfer of

ownership to the lessee nor a ‘reasonably certain’ purchase

option, the asset is depreciated over the shorter of its useful

life (10 yrs.) and the lease term (4 yrs.).

3. D

4. A

5. B

Solution:

Fixed payments 220,000

Multiply by: PV of an ordinary annuity of ₱1 3.16987

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

29.

@10%, n=4

Net investment697,371

6. A

PFRS 17 Insurance Contracts

PROBLEM 1: MULTIPLE CHOICE

1. D

2. C

3. A

4. D

5. D

6. A

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D

2. D

3. A

4. B

5. D

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815

![3. A (8M x 5%) ÷ 6 employees currently employed as at year-

end = 66,667

4. A

5. B

6. C

7. D

8. C

9. C

10.D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D [(20 employees x 1 day x 12 months) – 150 days] x ₱1,000

x 105% = 94,500.

The 20% employee turnover rate is irrelevant because

the employee benefits are monetized.

2. D

3. B Solution: 2,900,000 PV of DBO – 2,600,000 FVPA =

300,000 deficit

4. B Solution: 400,000 service cost + 20,000 net interest (see

computations below) = 420,000

5. C

Solution:

Service cost:

(a) Current service cost 400,000

(b) Past service cost -

(c) Any (gain) or loss on settlement -

400,000

Net interest on the net defined benefit liability (asset):

(a) Interest cost on the DBO (2M, beg. x 10%) 200,000

(b) Interest income on plan assets (1.8M, beg. x 10%) (180,000)

(c) Interest on the effect of the asset ceiling -

20,000

Remeasurements of the net defined benefit liability (asset):

(a) Actuarial (gains) and losses 200,000

(b) Difference between interest income on plan assets

and

60,000

return on plan assets (180,000 – 120,000)

(c) Difference between the interest on the effect of

the asset -

ceiling and change in the effect of the asset ceiling

260,000

Total Defined Benefit Cost 680,000

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815](https://image.slidesharecdn.com/sol-man-cfas-answersheet-answerkey-correct-answer-250608121017-7e87240b/85/sol-man-cfas-answersheet-answerkey-correct-answer-pdf-12-320.jpg)

![PAS 20 Accounting for Government Grants and

Disclosure of Government Assistance

PROBLEM 1: MULTIPLE CHOICE

1. B

2. A

3. C

4. D

5. C

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D

2. C

20x1 = 0, no depreciation yet is recognized from the

building; therefore, no income yet is recognized from

the government grant (i.e., ‘matching’). The building

starts to be depreciated in 20x2.

20x2 = 20,000 (200,000 ÷ 10 years)

3. B Gross presentation: (1M x 9/10) = 900,000;

Net presentation: (1M – 200K) x 9/10 = 720,000

4. A Gross presentation: (1M ÷ 10) = 100,000;

Net presentation: (1M – 200K) ÷ 10 = 80,000

5. A

Foreign Exchange Rates

PROBLEM 1: MULTIPLE CHOICE

1. D

2. A

3. D

4. A

5. B

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. A [$1,000 x (52 – 50)] = 2,000 gain

2. D [$1,000 x (47 – 52)] = 5,000 loss

3. D

Solution:

(₱10M total assets - ₱5M total liabilities) ÷ ₱10 closing rate =

¥500,000 translated equity

4. A

Solution:

₱3M profit ÷ ₱8 average rate = ¥375,000 translated profit

5. A

Solution:

Translated share capital = (₱2M ÷ ₱5 historical) = ¥400,000

Translated retained earnings (see table below)

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815](https://image.slidesharecdn.com/sol-man-cfas-answersheet-answerkey-correct-answer-250608121017-7e87240b/85/sol-man-cfas-answersheet-answerkey-correct-answer-pdf-13-320.jpg)

![4. A

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D

2. D

PAS 27 Separate Financial Statements

PROBLEM 1: MULTIPLE CHOICE

1. D

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. D

PAS 28 Investments in Associates and Joint

Ventures

PROBLEM 1: MULTIPLE CHOICE

1. B

2. B

3. C

4. A

Solution:

Investment in associate

3/31/x1

500,00

0

Sh. in P (1M x 20% x

9/12)

150,00

0 60,000

Dividends (300K x

20%)

40,000 Sh. in L (200K x 20%

- Dividends

550,00

0 12/31/x2

PROBLEM 2: FOR CLASSROOM DISCUSSION

1. C

Solution:

Investment in associate

1/1/x1

600,00

0

Sh. in profit (200K x

30%) 60,000 15,000

Dividends (50K x

30%)

645,00

0 12/31/x1

2. B [4M profit – (10M x 5%)] x 20% = 700,000

3. B

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815](https://image.slidesharecdn.com/sol-man-cfas-answersheet-answerkey-correct-answer-250608121017-7e87240b/85/sol-man-cfas-answersheet-answerkey-correct-answer-pdf-16-320.jpg)

![Date No. of sh.

Months

outstanding

Weighted

average

(a) (b) (c) = (a) x (b)

1/1/20x1 120,000 12/12 120,000

3/1/20x1 42,000 10/12 35,000

9/30/20x1 20,000 3/12 5,000

11/1/20x1 (12,000) 2/12 (2,000)

158,000

Basi

c

EPS

=

Profit (Loss) less Preferred dividends

Weighted average number of outstanding ordinary

shares

Basi

c

EPS

=

2,800,000 – (100,000 x ₱10 x 10%)

158,000

Basic EPS = ₱17.09

2. A [(-1M) – 50K] ÷ 100,000 = -1,050,000 ÷ 100,000 = -10.5

3. C

Solution:

The weighted average number of ordinary shares

outstanding are adjusted retrospectively as follows:

20x1 20x2

1/1 (200,000 x 110% x

2)

440,00

0

(200,000 x 110% x 2 x

12/12)

440,00

0

4/1 (20,000 x 110% x 2 x 9/12) 33,00

0

9/3

0

-

11/

1

-

Weighted average 440,0

00

473,0

00

20x2 20x1

Profit after tax

2,200,00

0

1,800,00

0

Adjusted weighted ave. no. of outstanding

sh. 473,000 440,000

Basic EPS 4.65 4.09

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815](https://image.slidesharecdn.com/sol-man-cfas-answersheet-answerkey-correct-answer-250608121017-7e87240b/85/sol-man-cfas-answersheet-answerkey-correct-answer-pdf-18-320.jpg)

![4. A

Solution:

Aggregate mkt. value of shares before exercise of rts.

(200,000 sh. x ₱180)

36,000,00

0

Add: Proceeds from exercise of rts. [(200,000 rts. ÷ 5) x

₱120] 4,800,000

Total

40,800,00

0

Divide by: Outstanding shares after exercise of rts.

[200,000 sh. before exercise + (200,000 rts. ÷ 5 rts. per

sh.)] 240,000

Theoretical ex-rights fair value per share 170

Adjustme

nt factor

=

Fair value of stocks immediately before the

exercise of rights

Theoretical ex-rights fair value per share

The adjustment factor is 180/170.

Jan. 1: (200,000 x 180/170 x 4/12)

70,58

8

May. 1: (240,000 x 8/12)

160,0

00

Weighted average no. of outstanding ordinary

shares

230,58

8

Profit for the year

2,900,00

0

Divide by: Weighted average no. of outstanding sh. 230,588

Basic earnings per share

12.5

8

5. C

Solution:

Diluted

EPS

=

Profit (Loss) plus After tax interest expense on

convertible bonds

Weighted average number of outstanding ordinary

shares plus Incremental shares arising from the

assumed conversion or exercise of dilutive potential

ordinary shares

Diluted

EPS

=

800,000 + (2,000,000 x 12% x 70%*)

100,000 + [(2,000,000 ÷ 1,000) x 30]

*70% = 1 – 30% tax rate

Downloaded by Zmm Dk (dmj2237@gmail.com)

lOMoARcPSD|46138815](https://image.slidesharecdn.com/sol-man-cfas-answersheet-answerkey-correct-answer-250608121017-7e87240b/85/sol-man-cfas-answersheet-answerkey-correct-answer-pdf-19-320.jpg)