Download to read offline

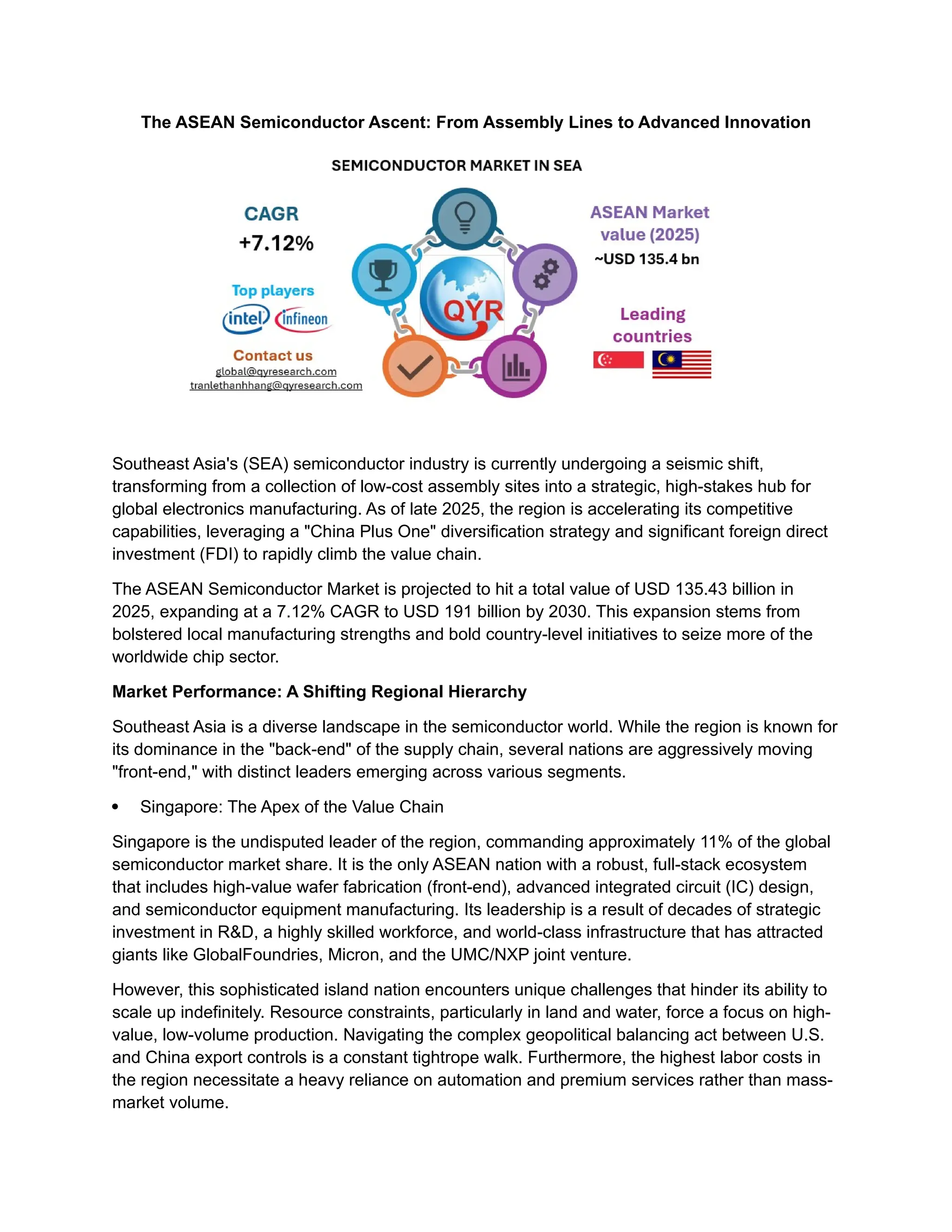

Southeast Asia's (SEA) semiconductor industry is currently undergoing a seismic shift, transforming from a collection of low-cost assembly sites into a strategic, high-stakes hub for global electronics manufacturing. As of late 2025, the region is accelerating its competitive capabilities, leveraging a "China Plus One" diversification strategy and significant foreign direct investment to rapidly climb the value chain.