Download to read offline

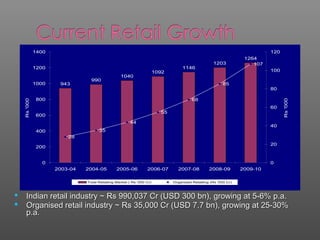

The Indian retail sector is a rapidly evolving industry, valued at approximately USD 300 billion, with only 4.6% organized retail, dominated primarily by food and grocery stores. Despite restrictions on foreign direct investment, various domestic and global players are planning expansions into smaller towns and the organized retail market is expected to grow significantly. Key players in the market include Pantaloon, Big Bazaar, and various international retailers such as Walmart and Tesco, indicating a competitive landscape with a shift towards urban and rural opportunities.