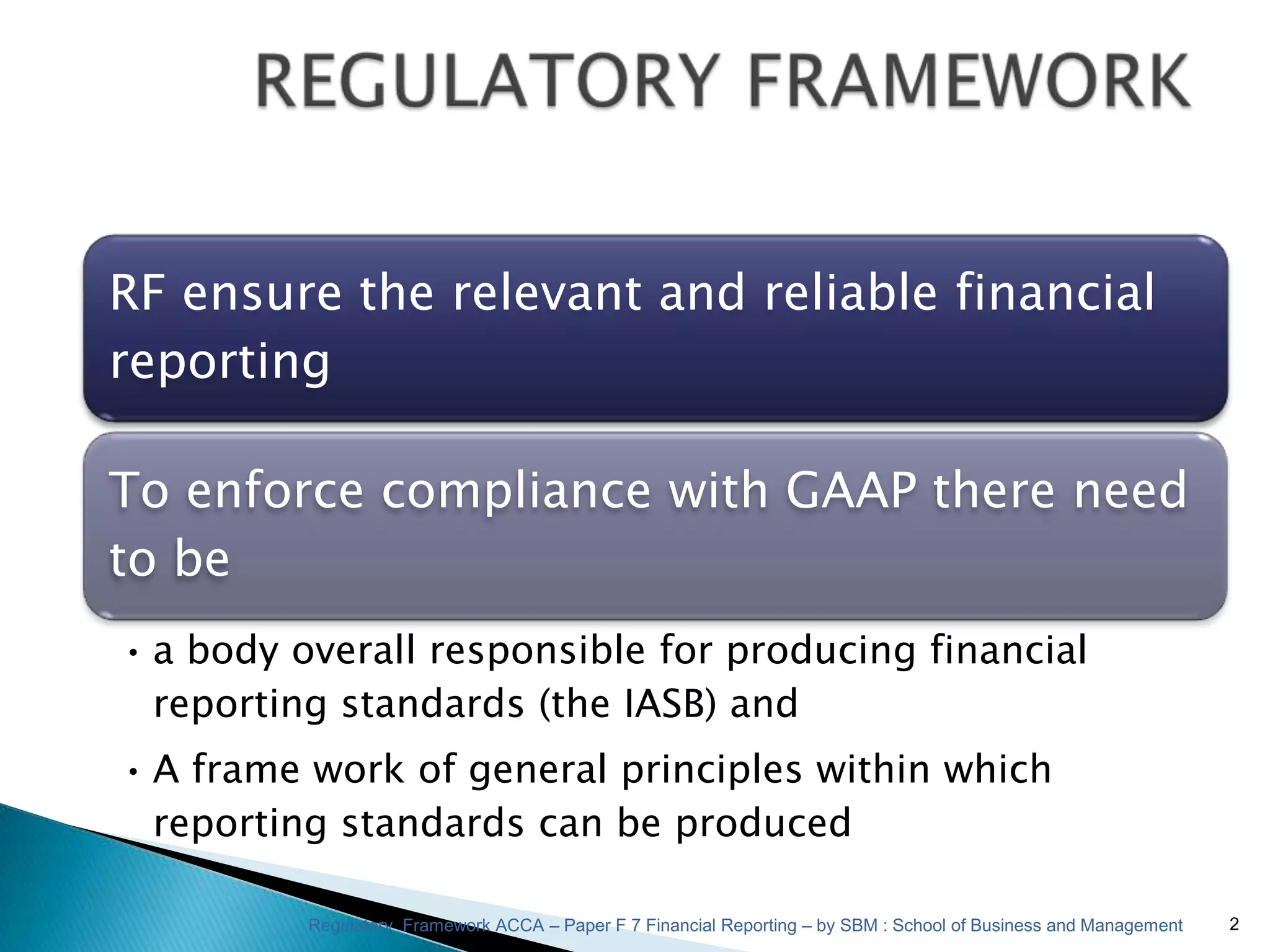

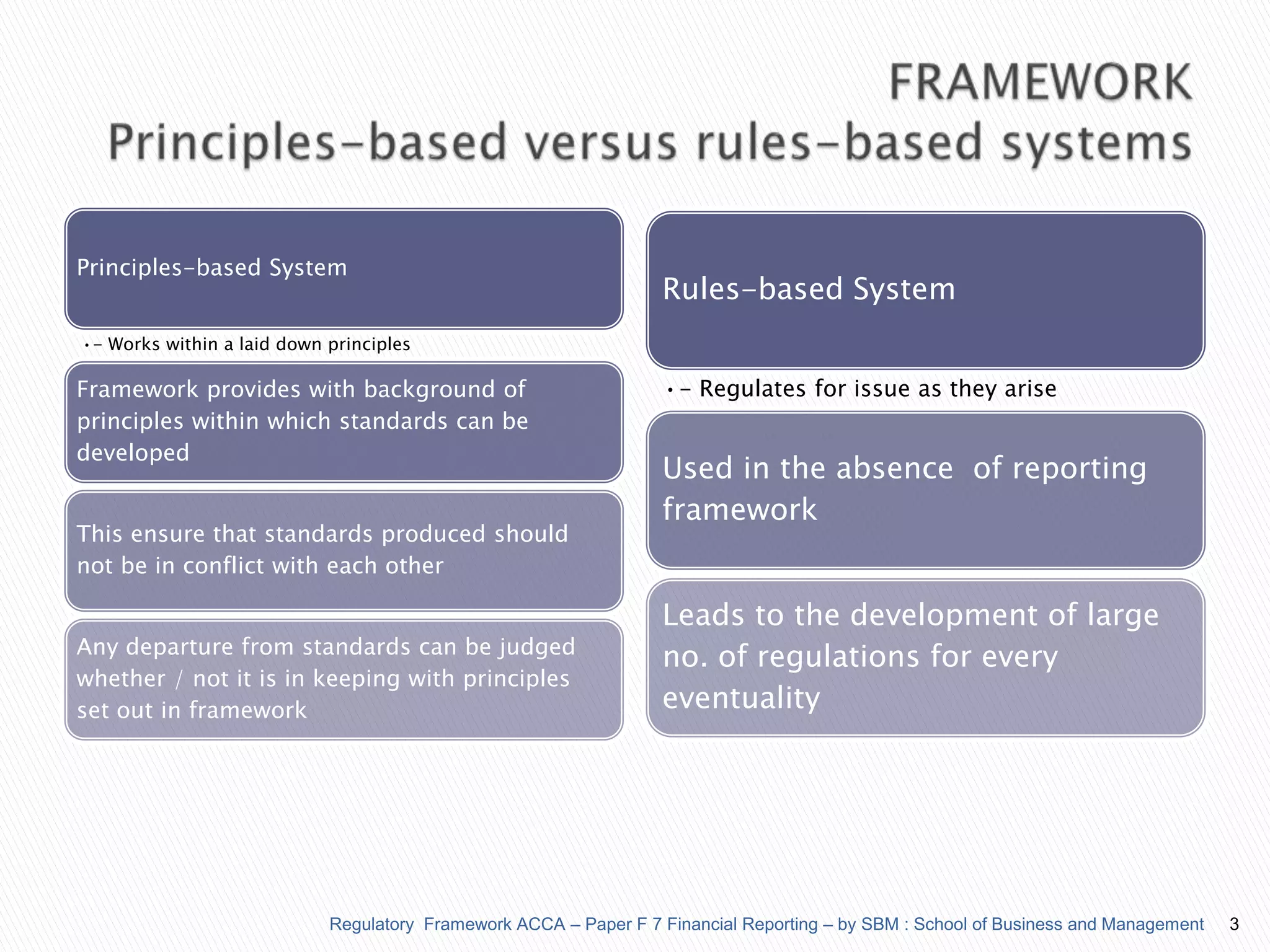

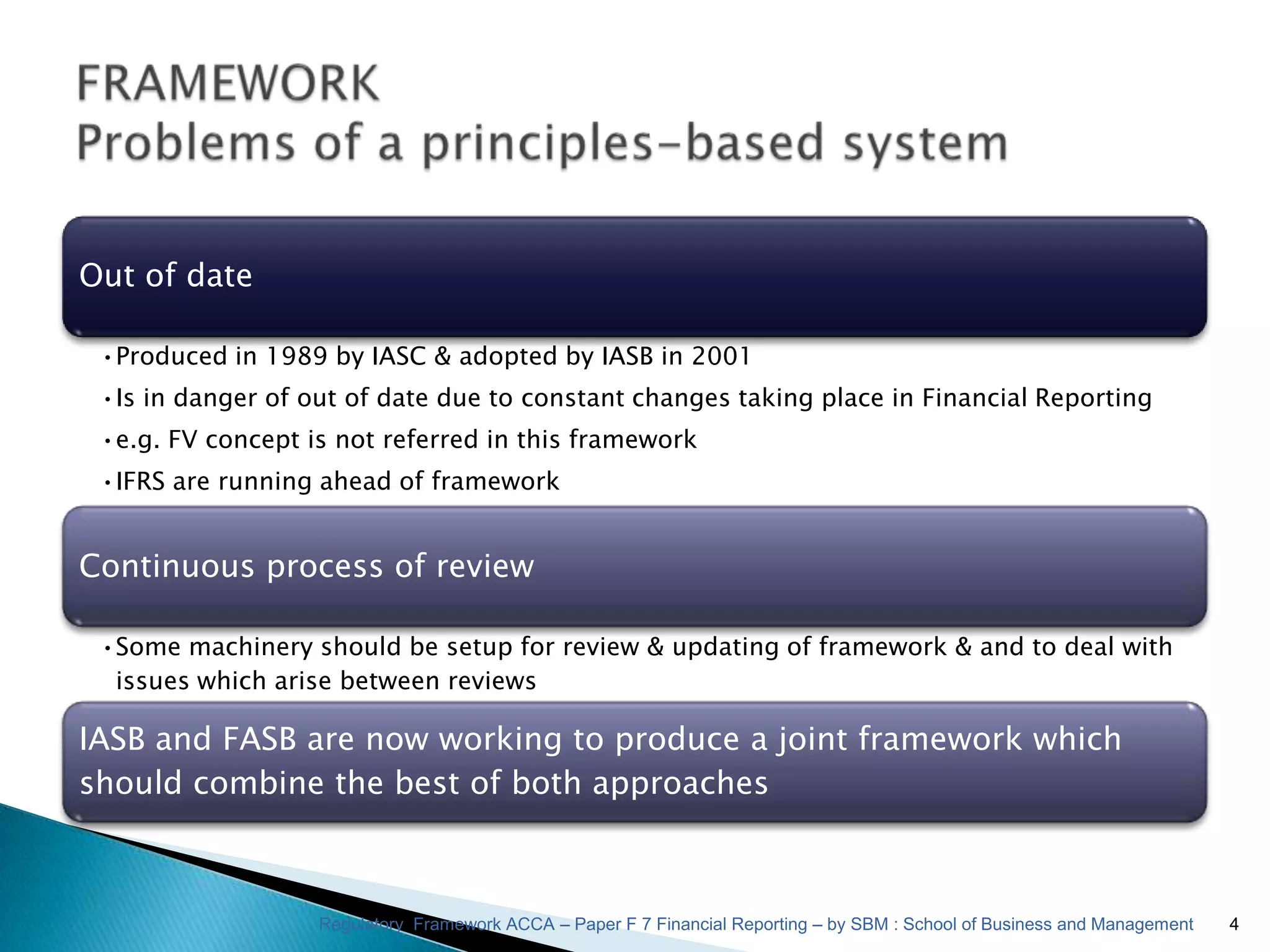

The document discusses regulatory frameworks for financial reporting. It addresses the differences between principles-based and rules-based systems, and some of the problems with principles-based approaches. It also describes the International Accounting Standards Board (IASB) and its role in developing International Financial Reporting Standards (IFRS). The IASB works to develop IFRS through an open process and coordinates with other standard setters to have a worldwide influence on financial reporting.