Problem:

The regression modelsassume that the errors are independent (or uncorrelated)

random variables. This means that the different values of the response variable, Y,

can be related to the values of the predictor variables, the X’s, but not to one

another.

The usual interpretations of the results of a regression analysis depend heavily on

the assumption of independence.

3.

Time Series DataContext:

With time series data, the assumption of independence rarely holds.

Consider the annual base price for a particular model of a new car. Can

you imagine the chaos that would exist if the new car prices from one

year to the next were indeed unrelated (independent) of one another?

In such a world, prices would be determined like numbers drawn from a

random number table. Knowledge of the price in one year would not

tell you anything about the price in the next year. In the real world, price

in the current year is related to (correlated with) the price in the

previous year, and maybe the price two years ago, and

so forth.

That is, the prices in different years are autocorrelated; they are not

independent.

Autocorrelation is notall bad:

• From a forecasting perspective, autocorrelation is not all bad. If values

of a response, Y, in one time period are related to Y values in previous

time periods, then previous Y’s can be used to predict future Y’s.

• In a regression framework, autocorrelation is handled by “fixing up”

the standard regression model. To accommodate autocorrelation,

sometimes it is necessary to change the mix of predictor variables

and/or the form of the regression function.

• More typically, however, autocorrelation is handled by changing the

nature of the error term.

6.

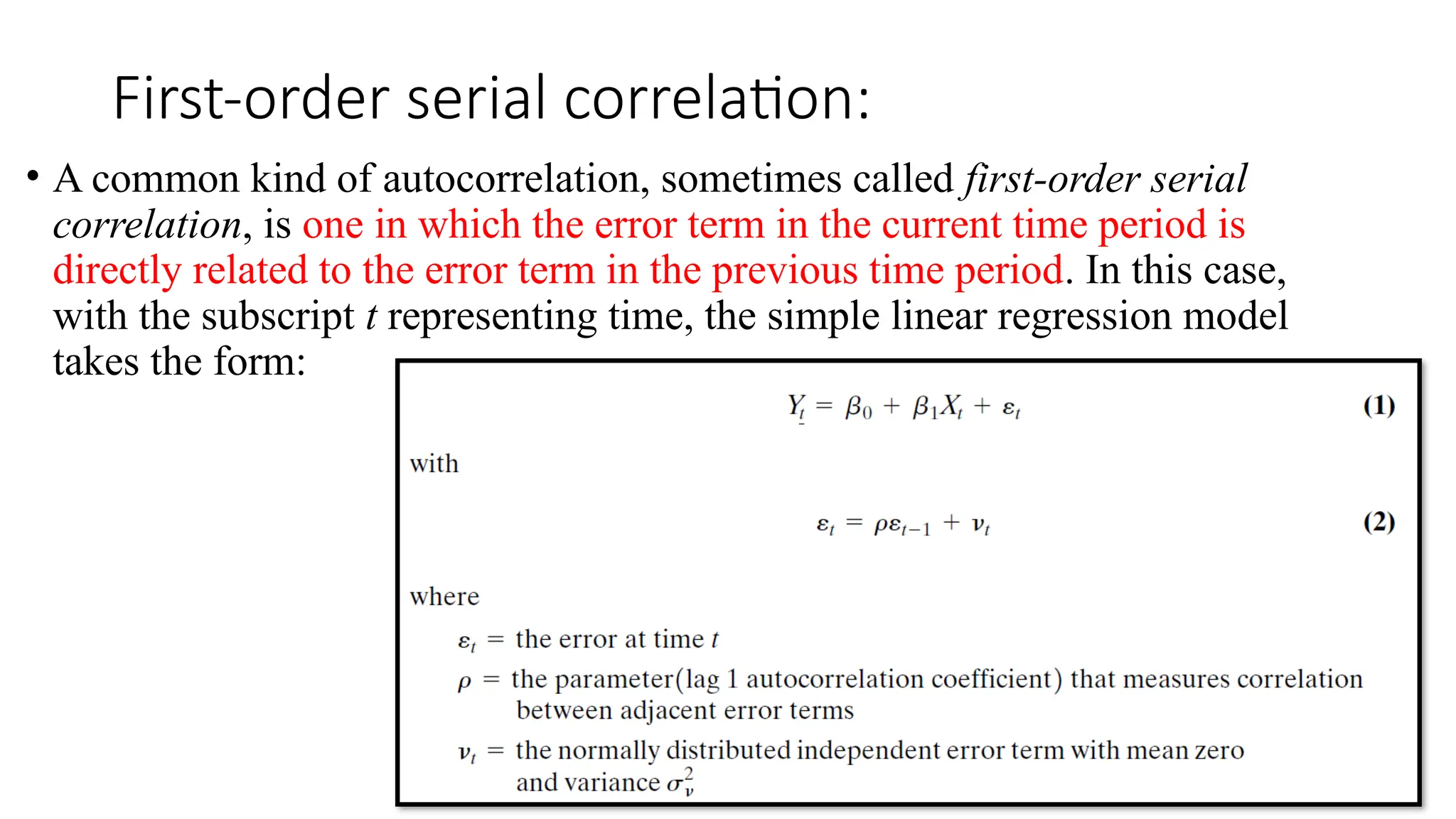

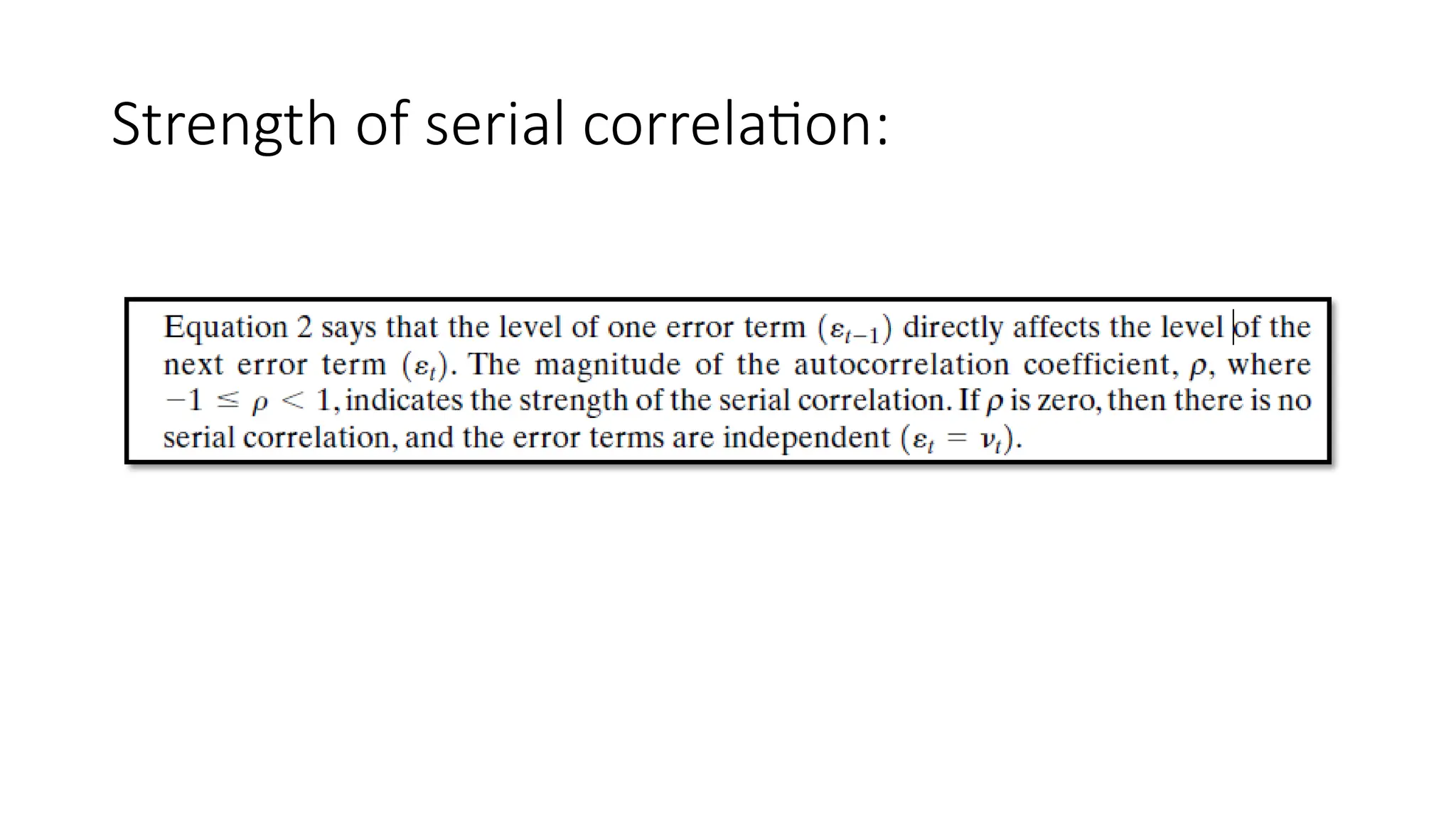

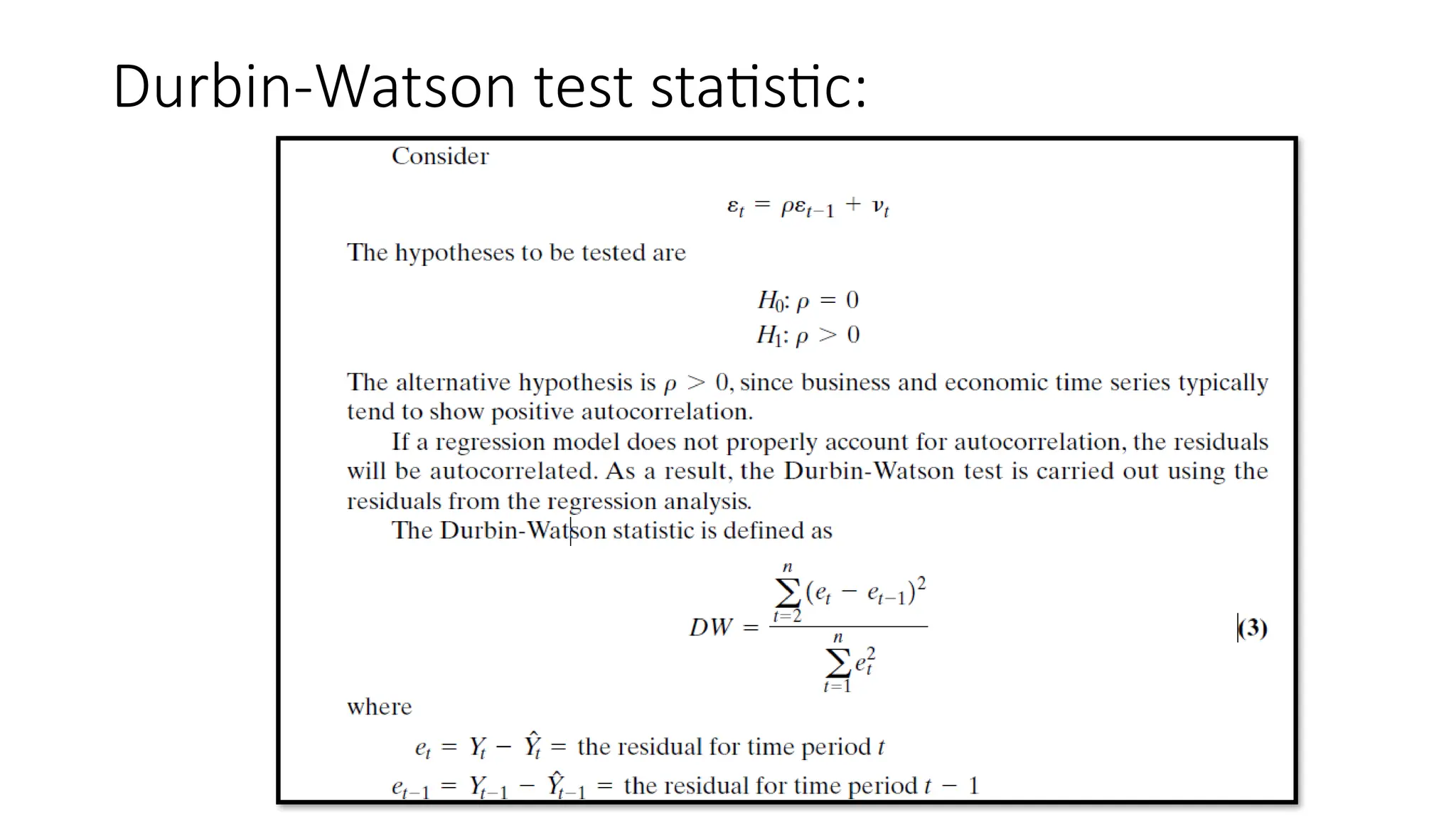

First-order serial correlation:

•A common kind of autocorrelation, sometimes called first-order serial

correlation, is one in which the error term in the current time period is

directly related to the error term in the previous time period. In this case,

with the subscript t representing time, the simple linear regression model

takes the form:

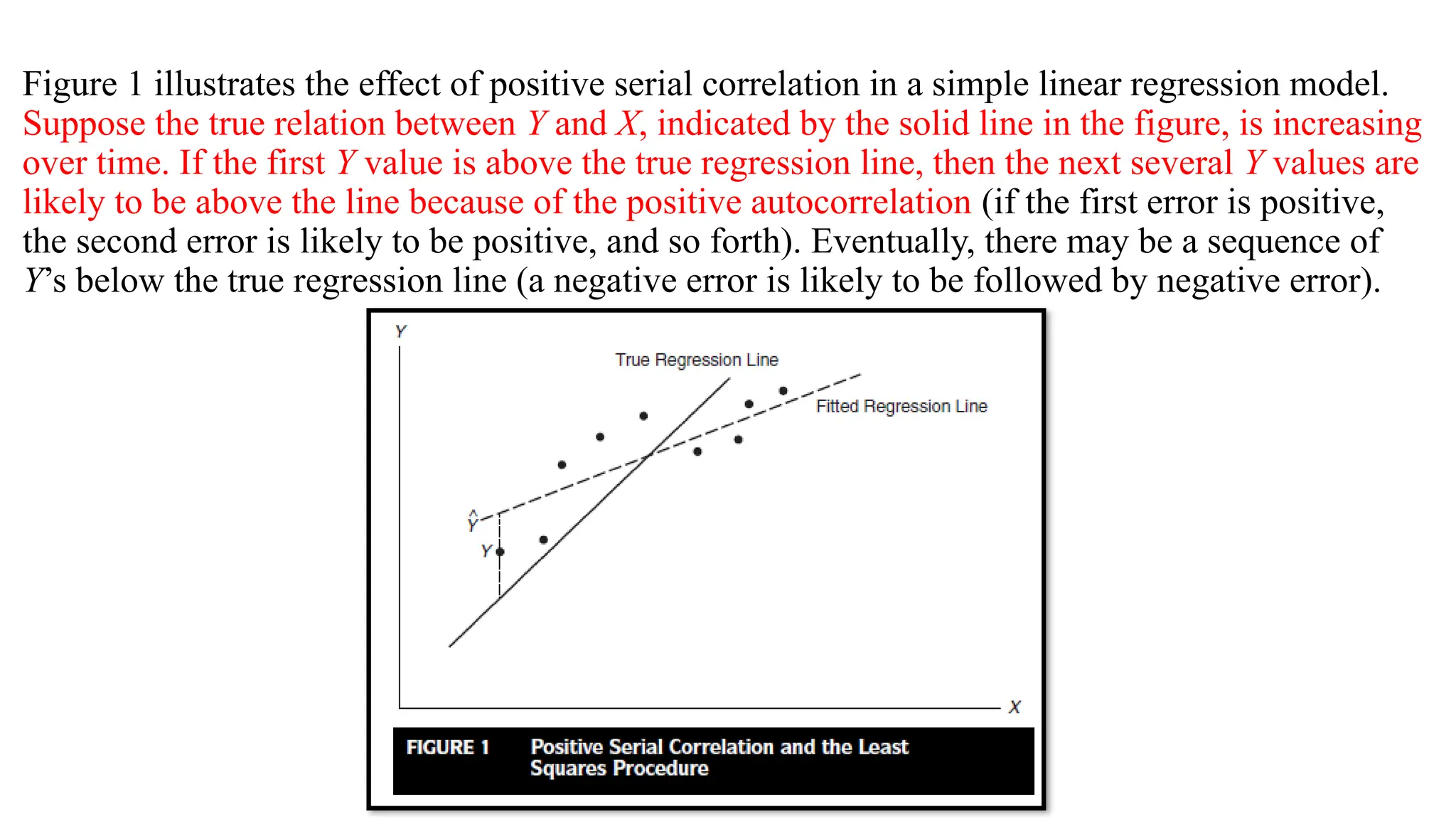

Figure 1 illustratesthe effect of positive serial correlation in a simple linear regression model.

Suppose the true relation between Y and X, indicated by the solid line in the figure, is increasing

over time. If the first Y value is above the true regression line, then the next several Y values are

likely to be above the line because of the positive autocorrelation (if the first error is positive,

the second error is likely to be positive, and so forth). Eventually, there may be a sequence of

Y’s below the true regression line (a negative error is likely to be followed by negative error).

9.

Problems with theinference:

• The data are “tilted” relative to the true X,Y relationship.

• However, the least squares line, by its very nature, will pass through the observations, as

indicated by the dotted line in the figure.

• Using the dotted line to make inferences about the solid line or using the dotted line to

generate forecasts of future Y’s could be very misleading.

• The scatter about the least squares line is tighter than it is about the true regression line.

Consequently, the standard error of the estimate, will underestimate the variability of the

Y’s about the true regression line.

• Strong autocorrelation can make two unrelated variables

appear to be related.

10.

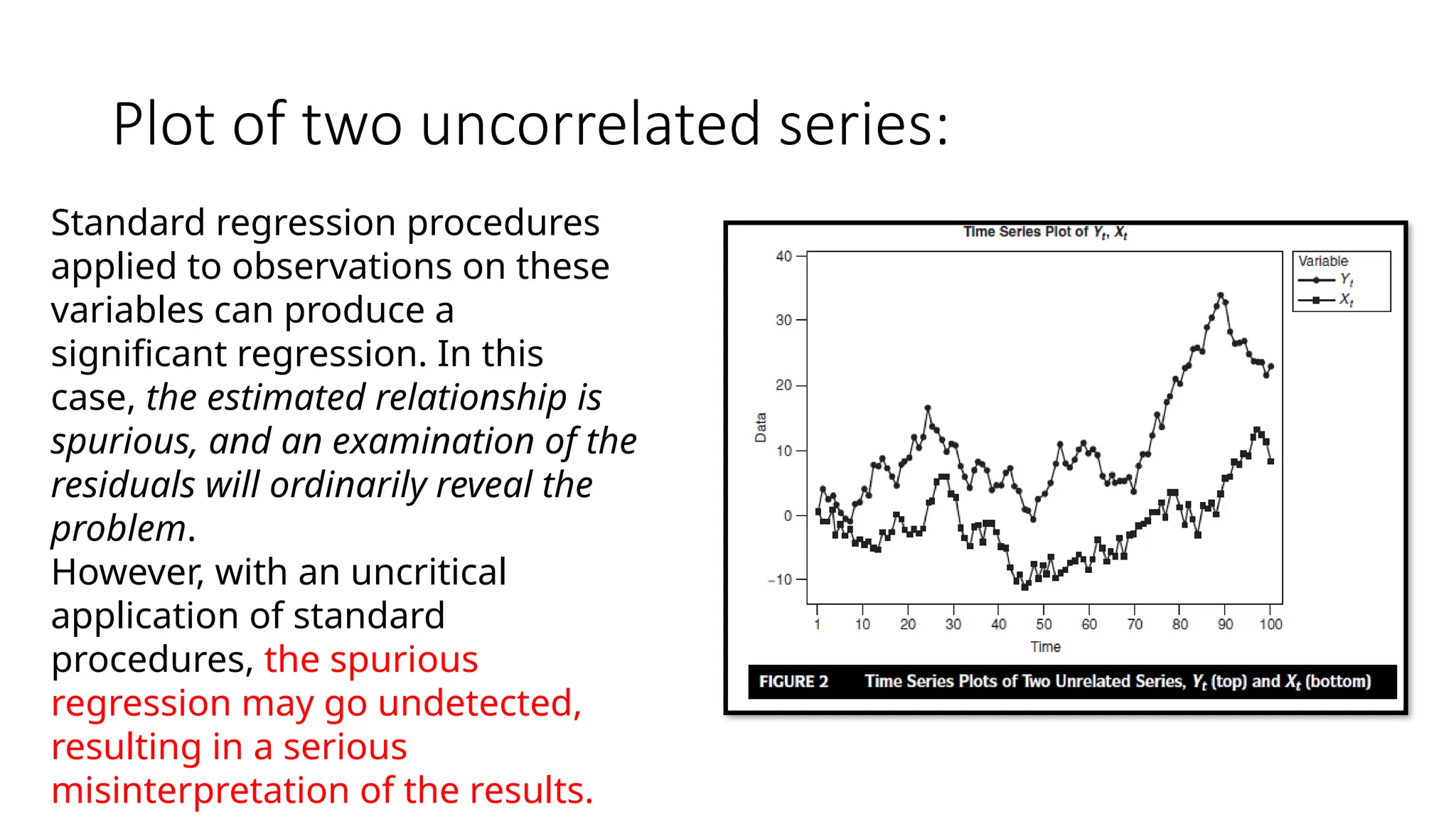

Plot of twouncorrelated series:

Standard regression procedures

applied to observations on these

variables can produce a

significant regression. In this

case, the estimated relationship is

spurious, and an examination of the

residuals will ordinarily reveal the

problem.

However, with an uncritical

application of standard

procedures, the spurious

regression may go undetected,

resulting in a serious

misinterpretation of the results.

11.

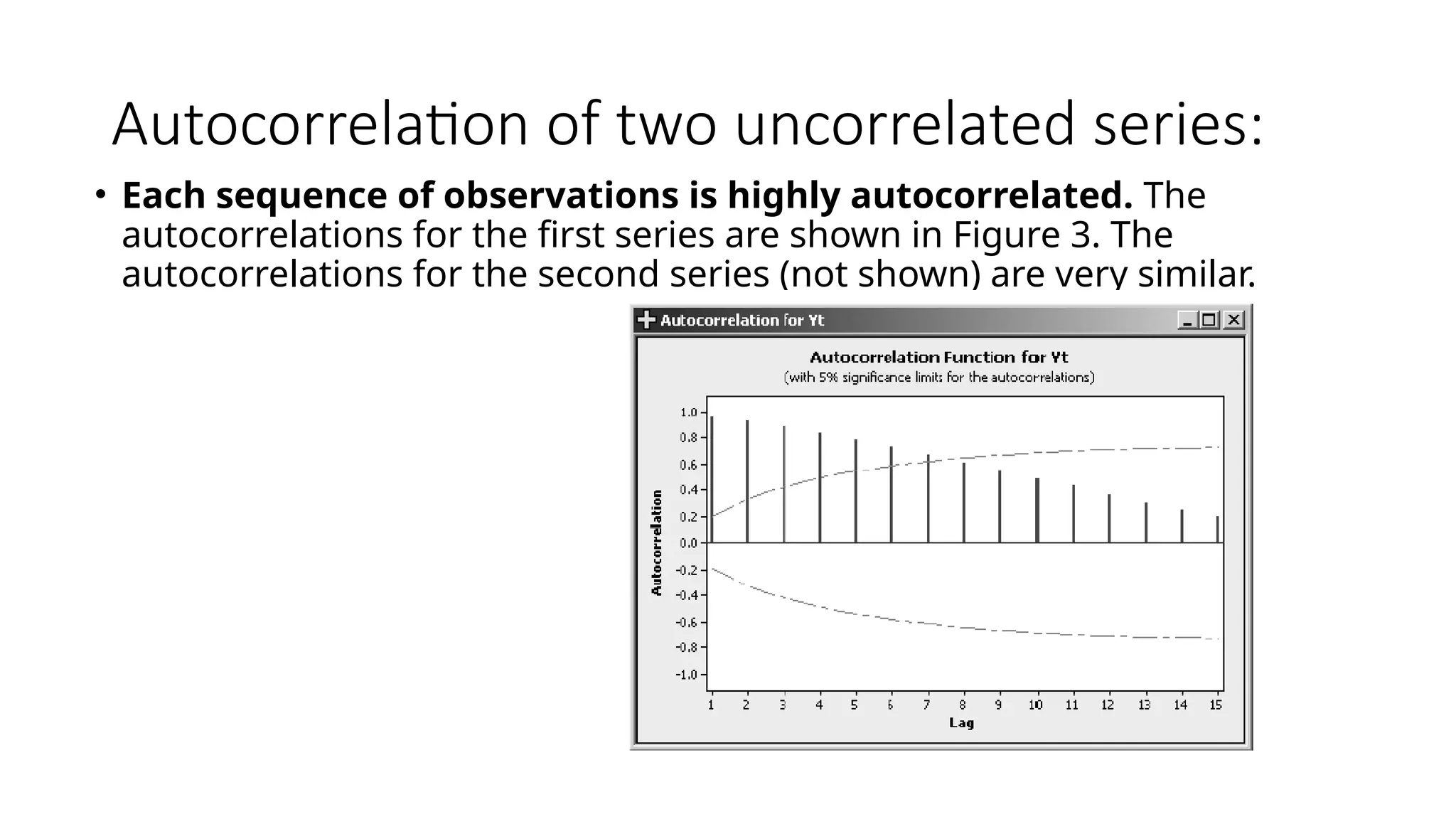

Autocorrelation of twouncorrelated series:

• Each sequence of observations is highly autocorrelated. The

autocorrelations for the first series are shown in Figure 3. The

autocorrelations for the second series (not shown) are very similar.

12.

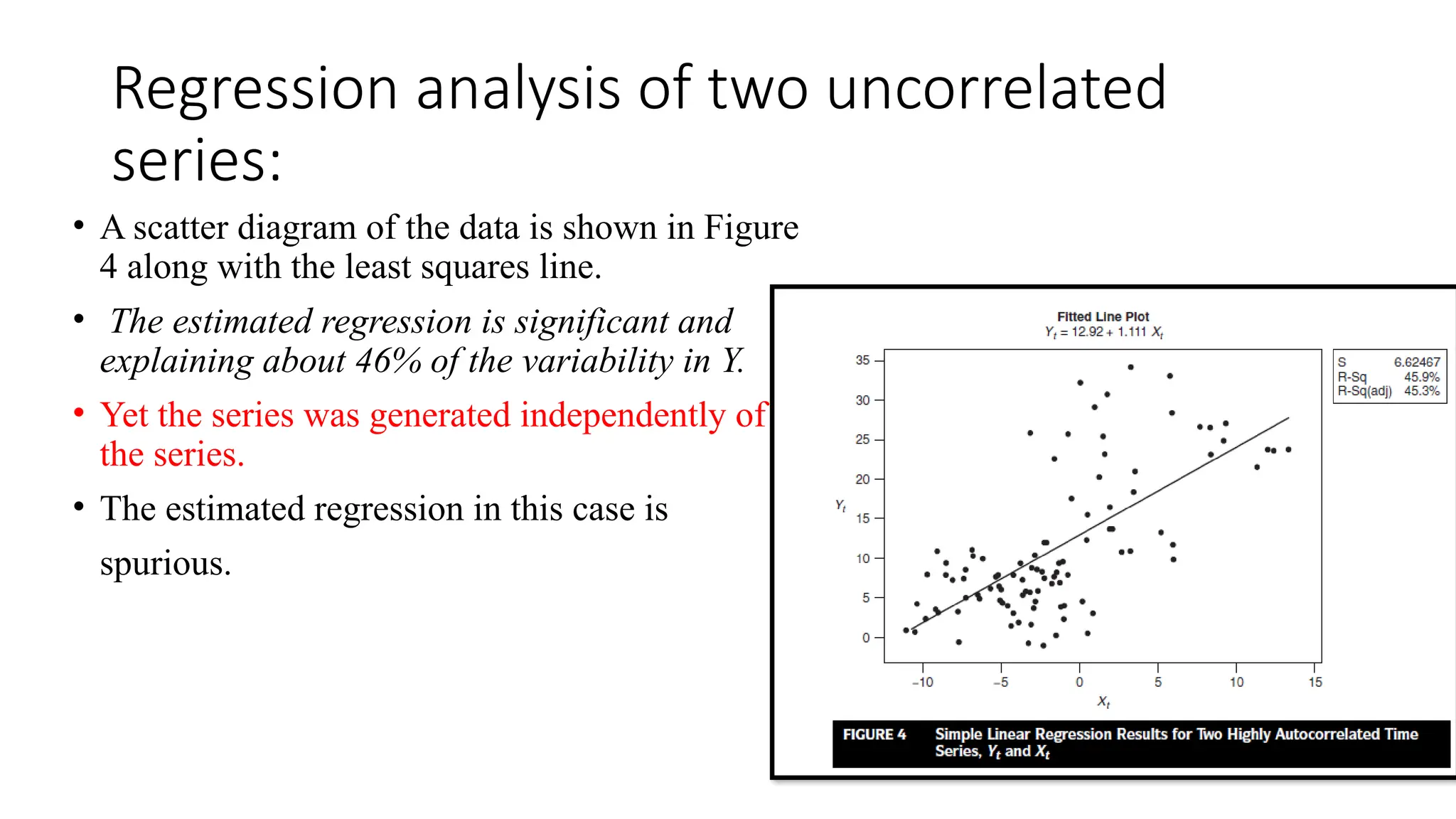

Regression analysis oftwo uncorrelated

series:

• A scatter diagram of the data is shown in Figure

4 along with the least squares line.

• The estimated regression is significant and

explaining about 46% of the variability in Y.

• Yet the series was generated independently of

the series.

• The estimated regression in this case is

spurious.

13.

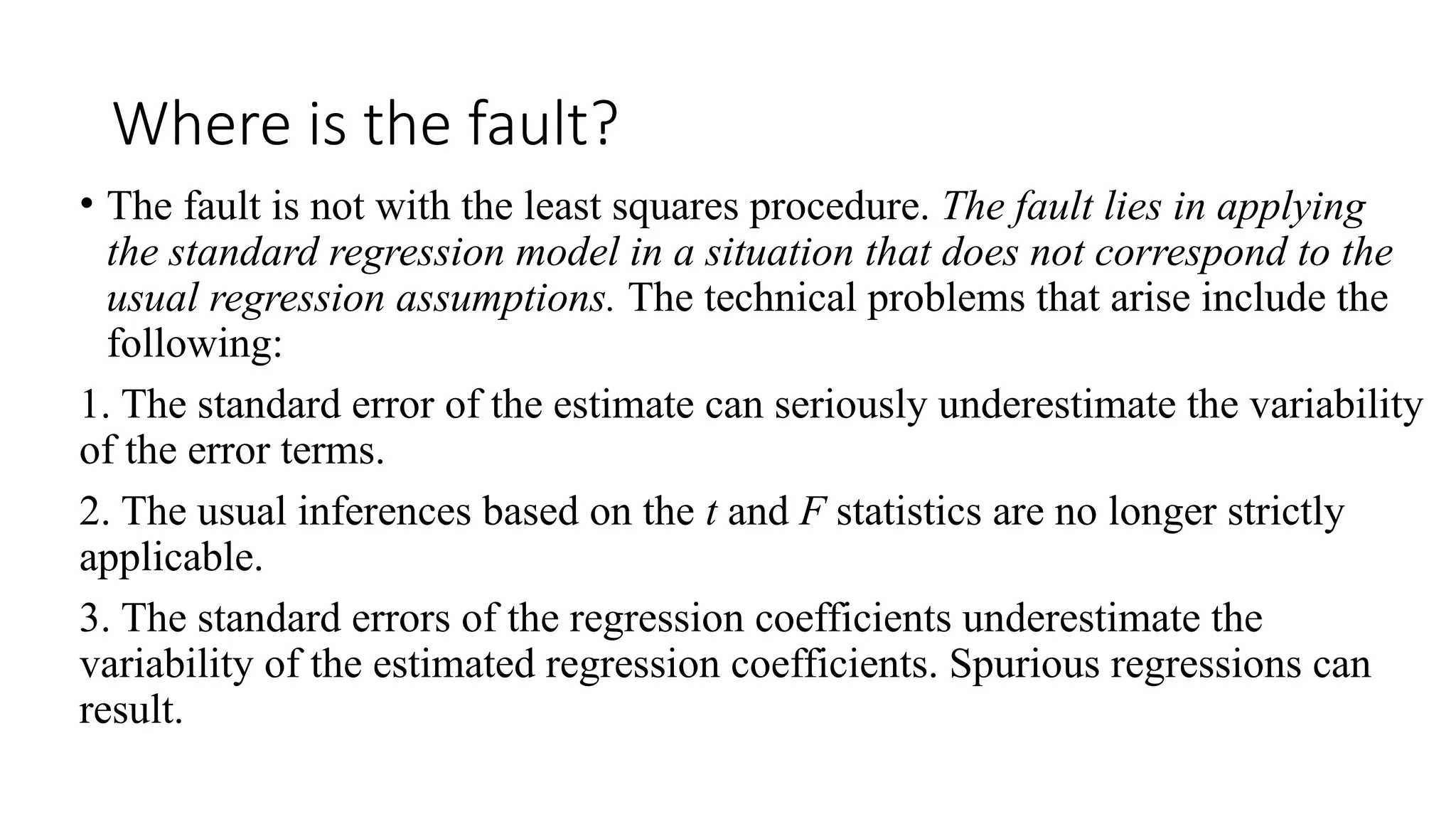

Where is thefault?

• The fault is not with the least squares procedure. The fault lies in applying

the standard regression model in a situation that does not correspond to the

usual regression assumptions. The technical problems that arise include the

following:

1. The standard error of the estimate can seriously underestimate the variability

of the error terms.

2. The usual inferences based on the t and F statistics are no longer strictly

applicable.

3. The standard errors of the regression coefficients underestimate the

variability of the estimated regression coefficients. Spurious regressions can

result.

14.

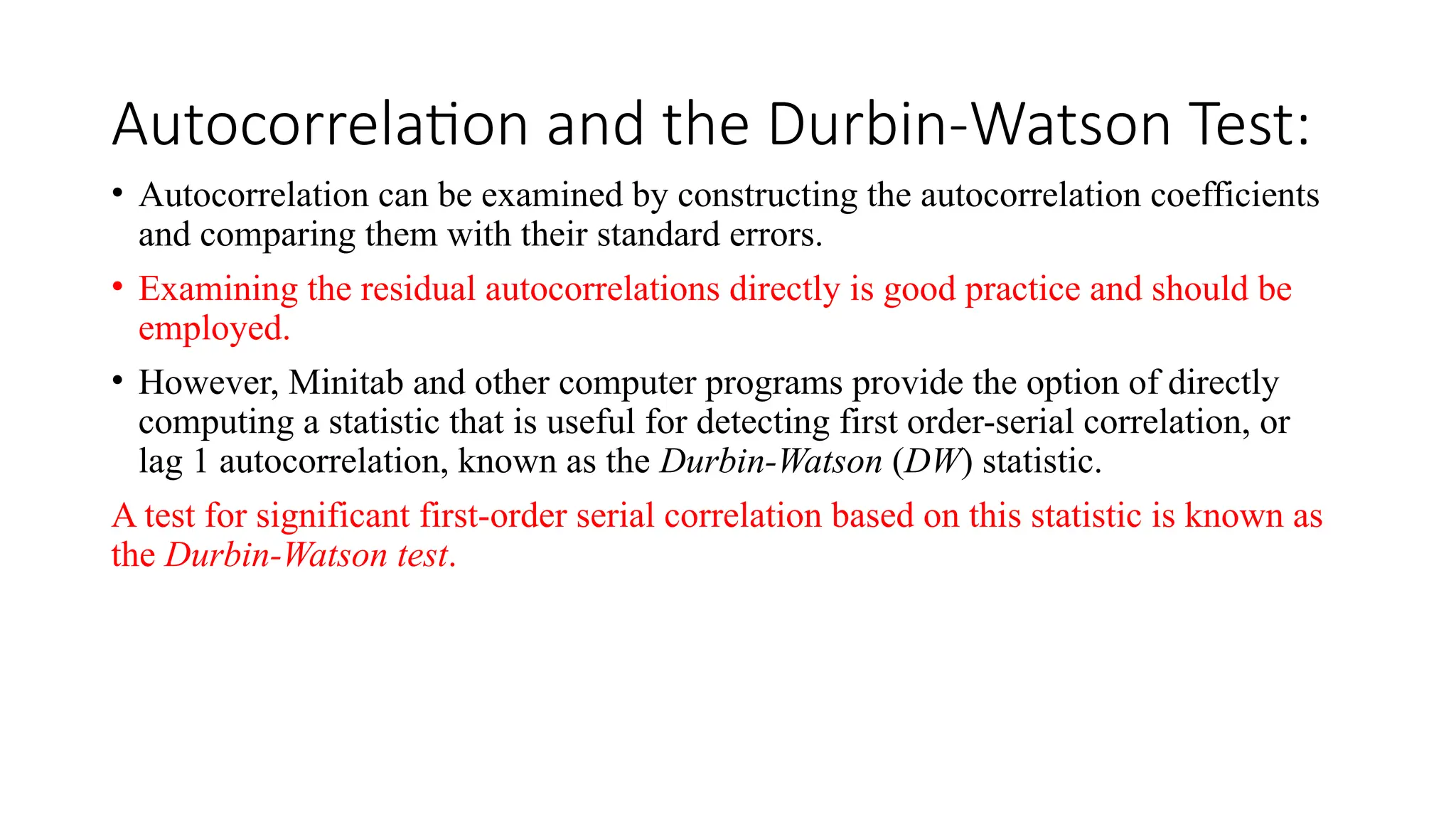

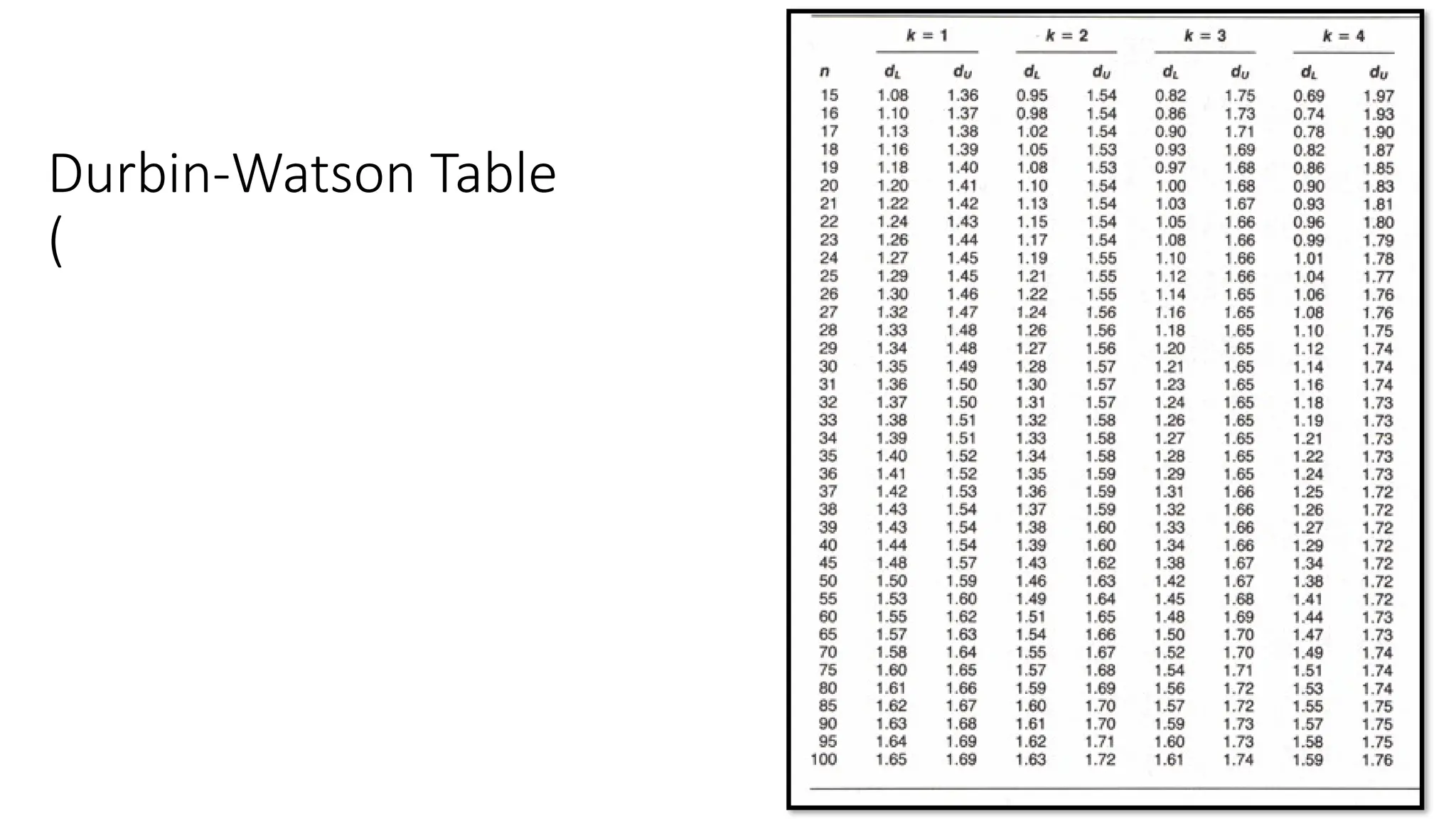

Autocorrelation and theDurbin-Watson Test:

• Autocorrelation can be examined by constructing the autocorrelation coefficients

and comparing them with their standard errors.

• Examining the residual autocorrelations directly is good practice and should be

employed.

• However, Minitab and other computer programs provide the option of directly

computing a statistic that is useful for detecting first order-serial correlation, or

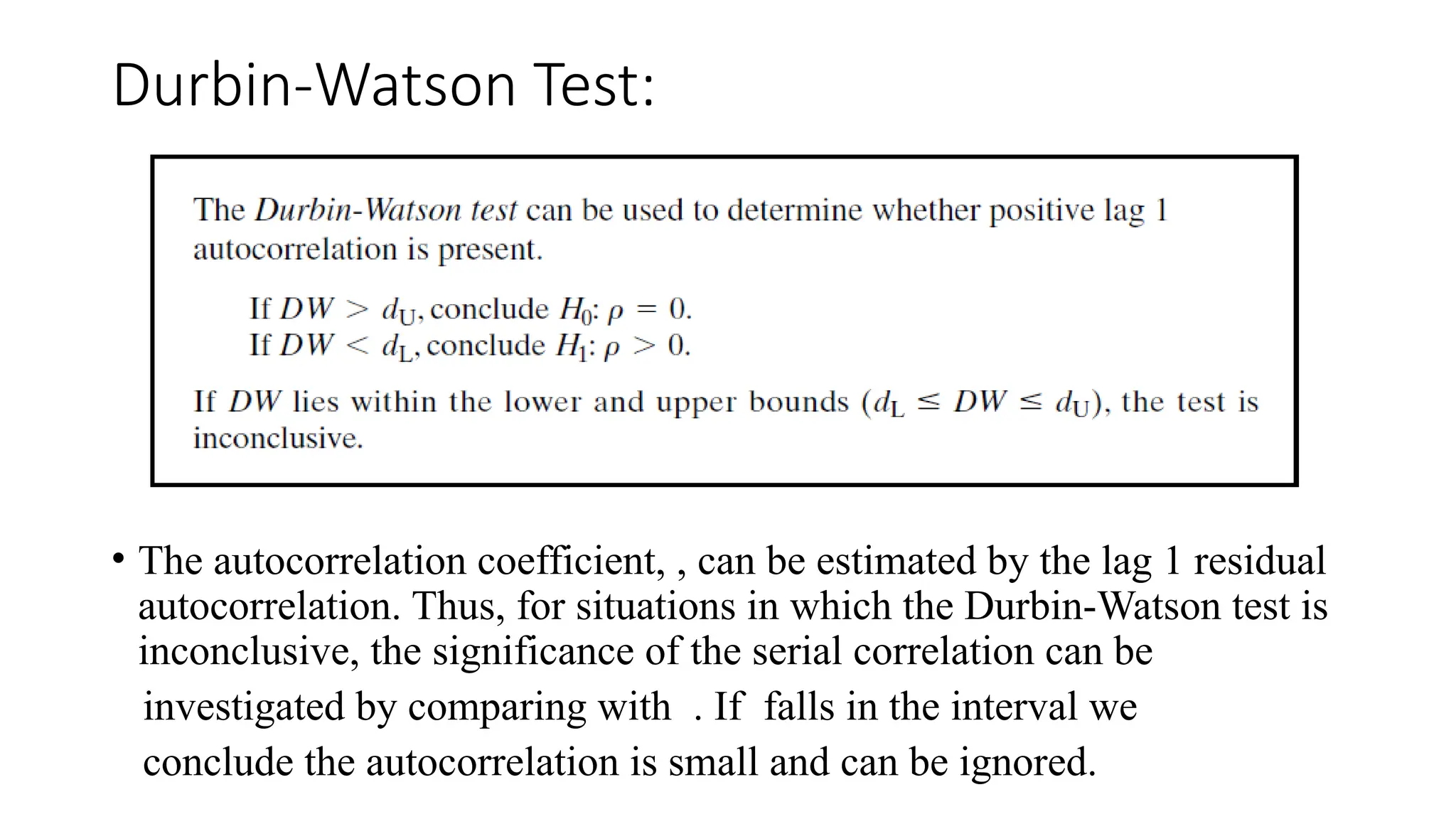

lag 1 autocorrelation, known as the Durbin-Watson (DW) statistic.

A test for significant first-order serial correlation based on this statistic is known as

the Durbin-Watson test.

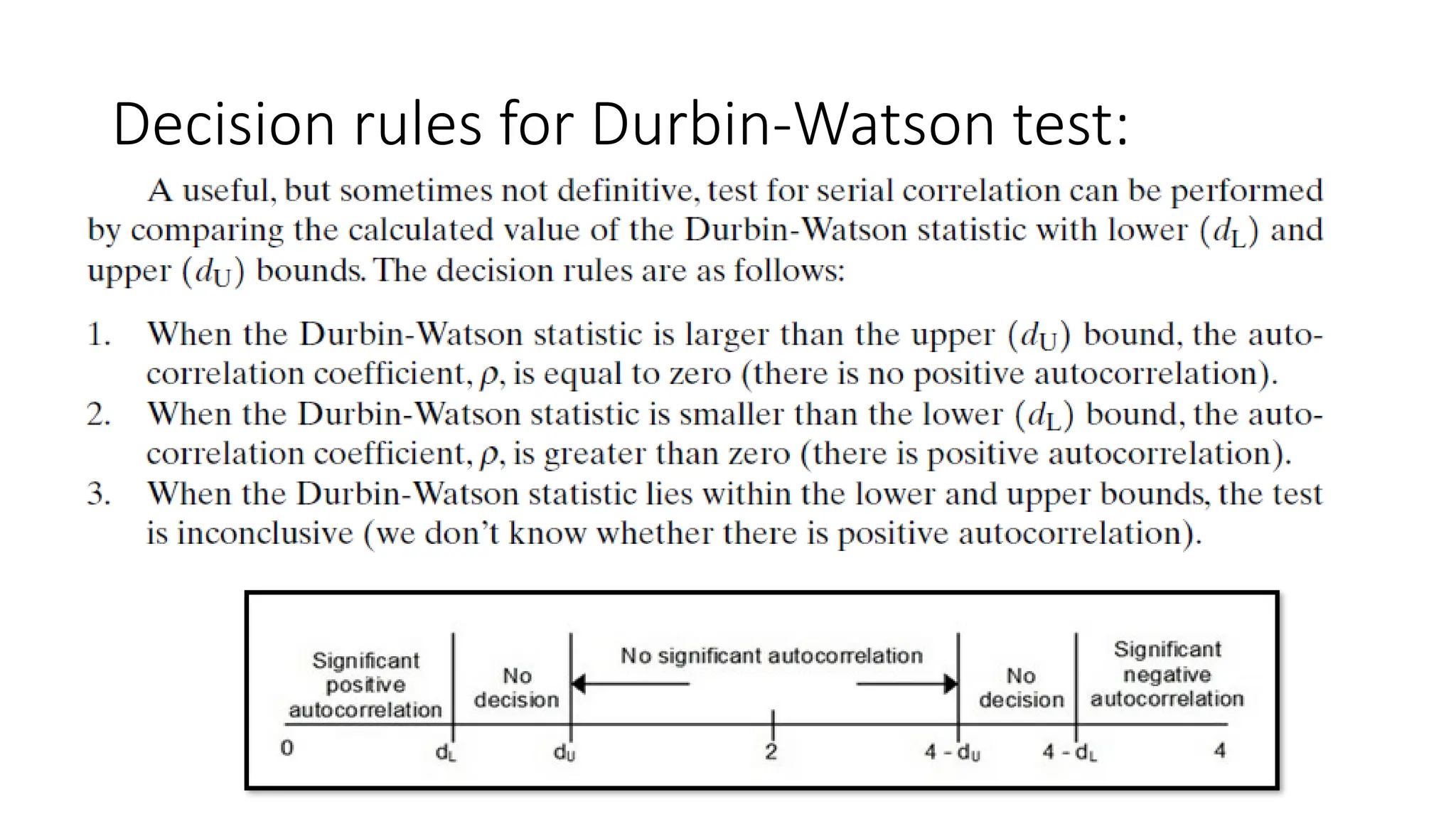

Durbin-Watson Test:

• Theautocorrelation coefficient, , can be estimated by the lag 1 residual

autocorrelation. Thus, for situations in which the Durbin-Watson test is

inconclusive, the significance of the serial correlation can be

investigated by comparing with . If falls in the interval we

conclude the autocorrelation is small and can be ignored.

19.

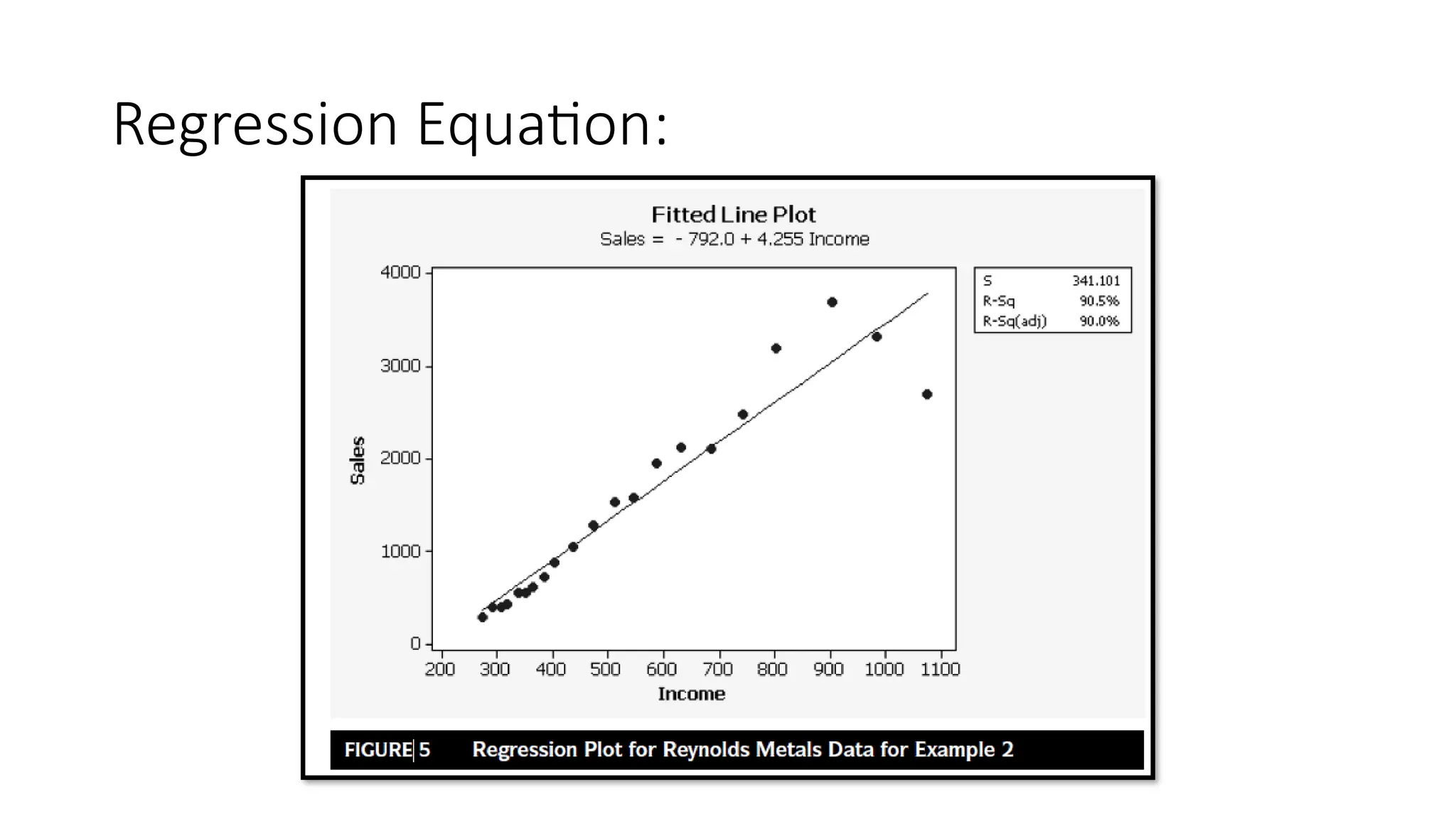

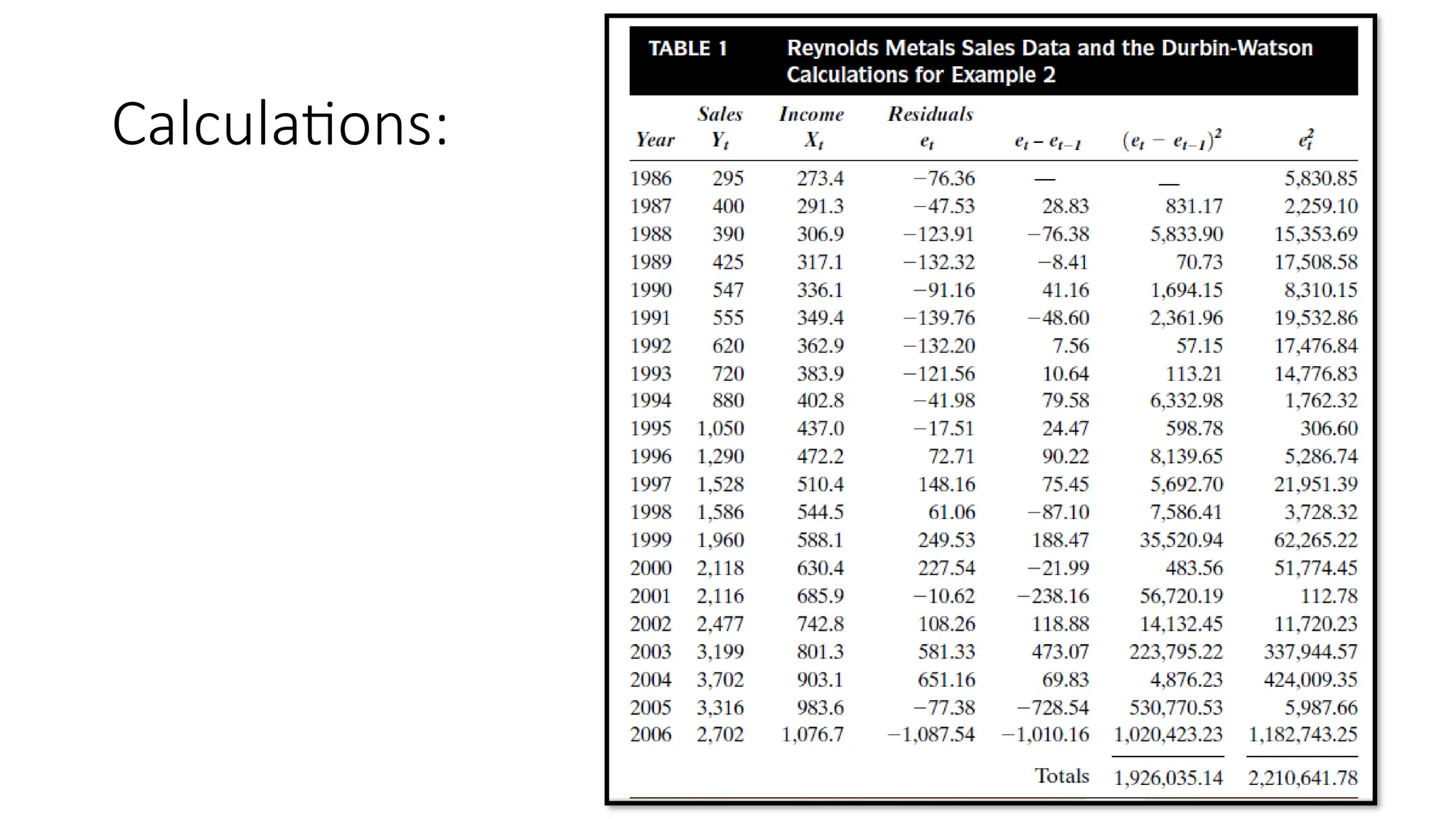

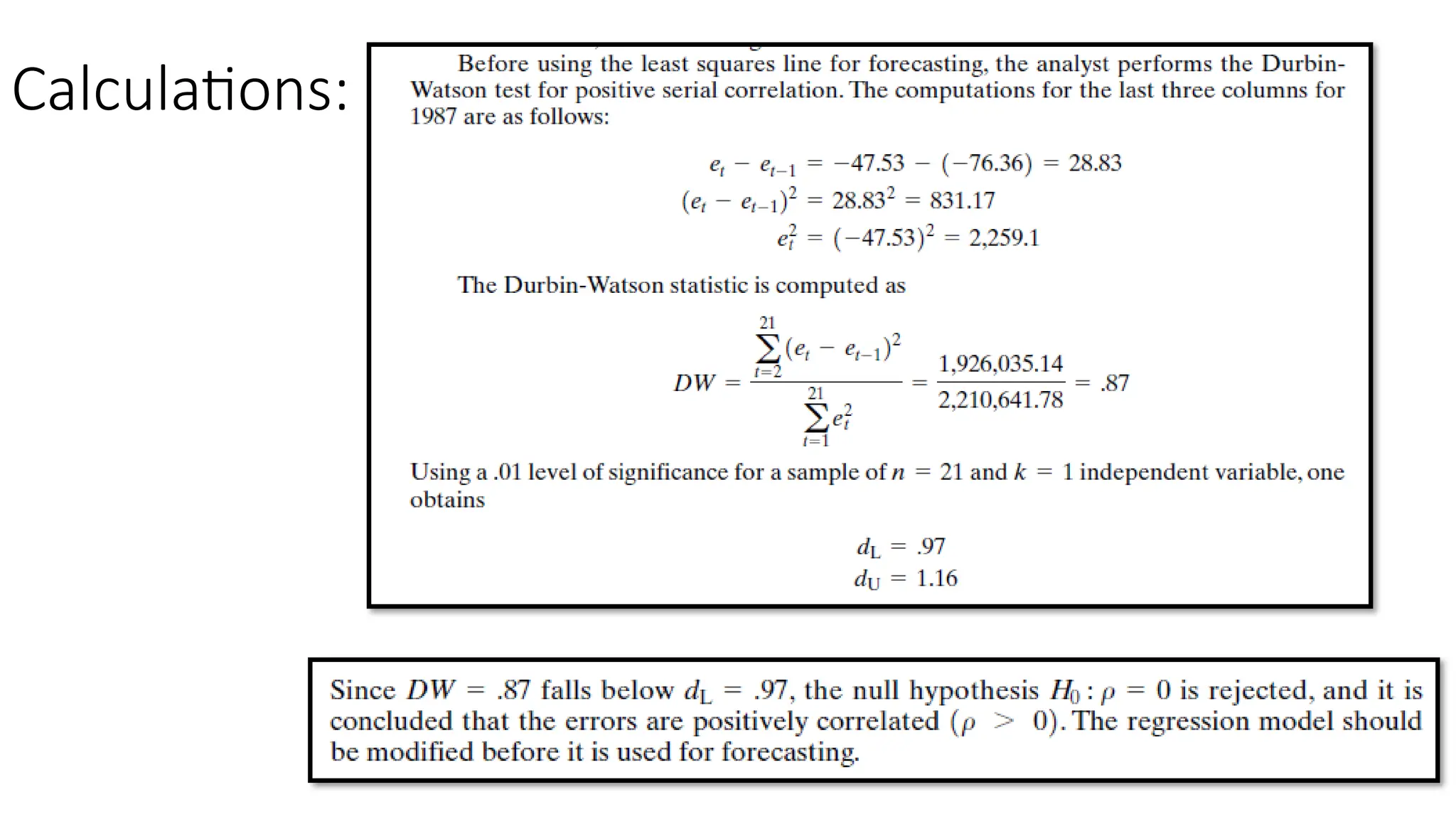

Example:

• Suppose ananalyst is engaged in forward planning for Reynolds Metals

Company, an aluminum producer, and wishes to establish a quantitative

basis for projecting future sales. Since the company sells regionally, a

measure of disposable personal income for the region should be closely

related to sales.

• Table 1 shows sales and income for the period from 1986 to 2006. Also

shown in the table are the columns necessary to calculate the DW statistic

(see the Minitab Applications section at end of chapter).

• The residuals come from a least squares line fit to the data, as shown in

Figure 5. Before using the least squares line for forecasting, the analyst

performs the Durbin-Watson test for positive serial correlation

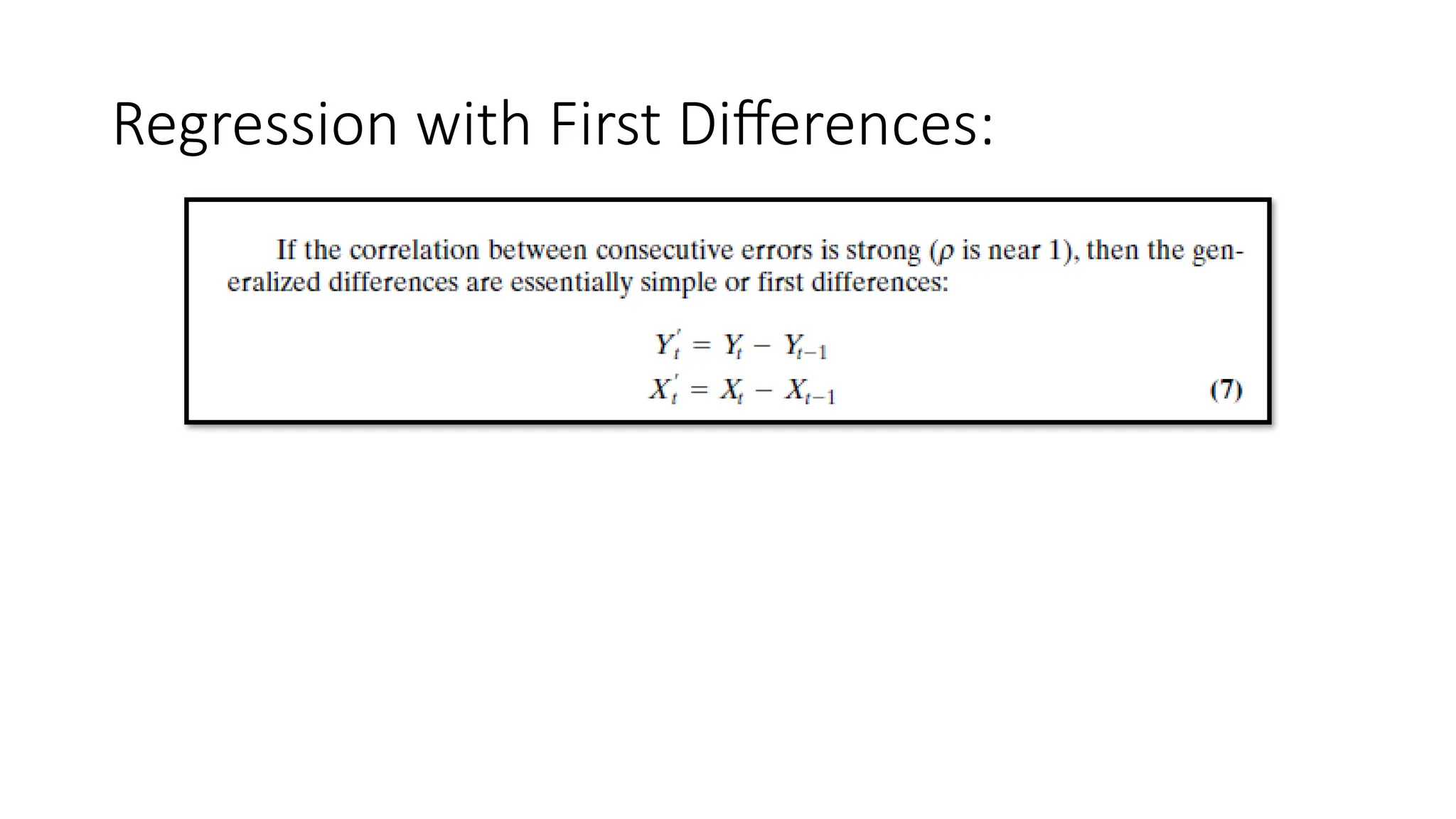

Solution to autocorrelationproblems:

• The solution to the problem of autocorrelation begins with an

evaluation of the model specification.

• Is the functional form correct?

• Were any important variables omitted?

• Are there effects that might have some pattern over time that could

have introduced autocorrelation into the errors?

24.

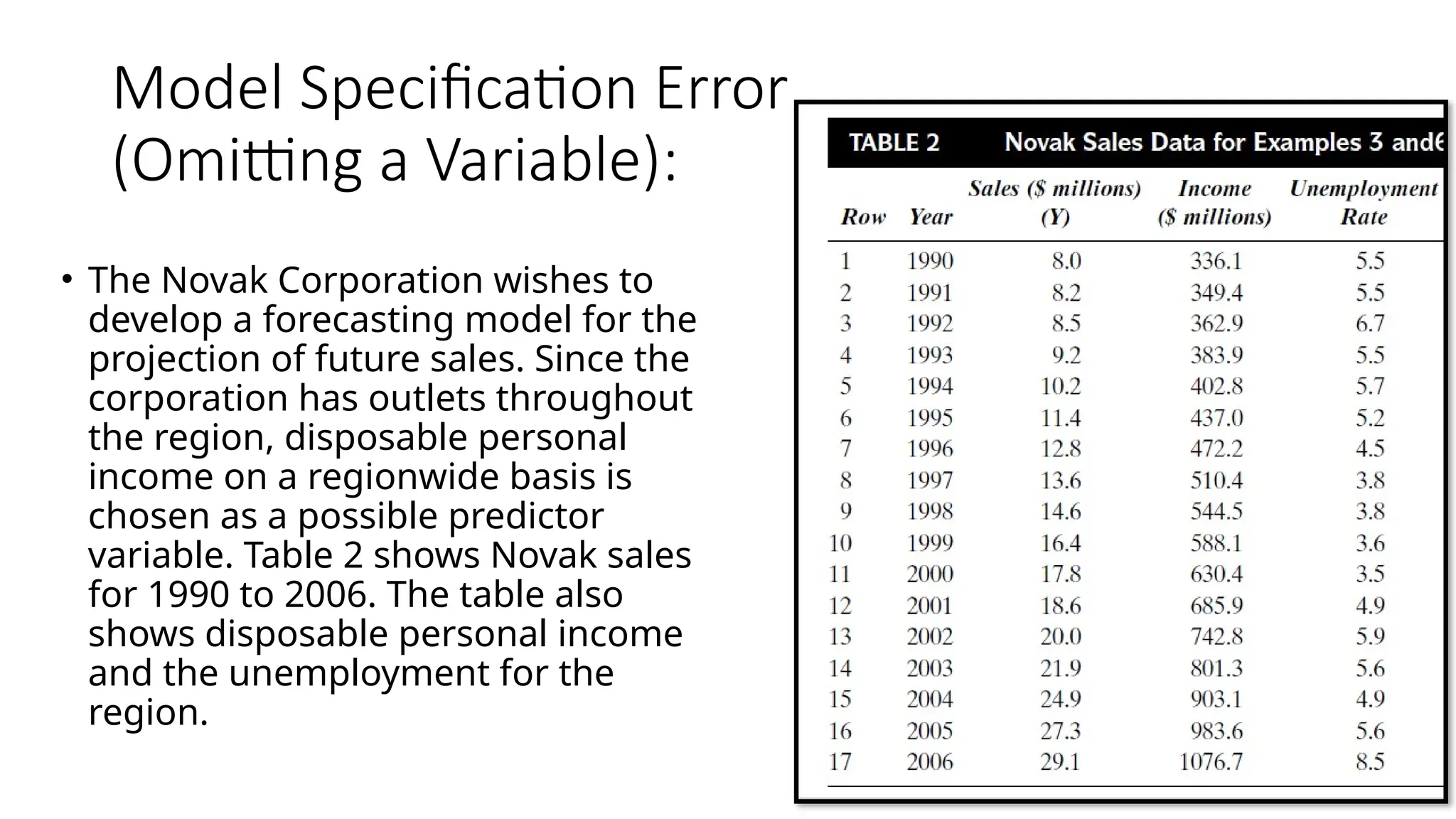

Model Specification Error

(Omittinga Variable):

• The Novak Corporation wishes to

develop a forecasting model for the

projection of future sales. Since the

corporation has outlets throughout

the region, disposable personal

income on a regionwide basis is

chosen as a possible predictor

variable. Table 2 shows Novak sales

for 1990 to 2006. The table also

shows disposable personal income

and the unemployment for the

region.

25.

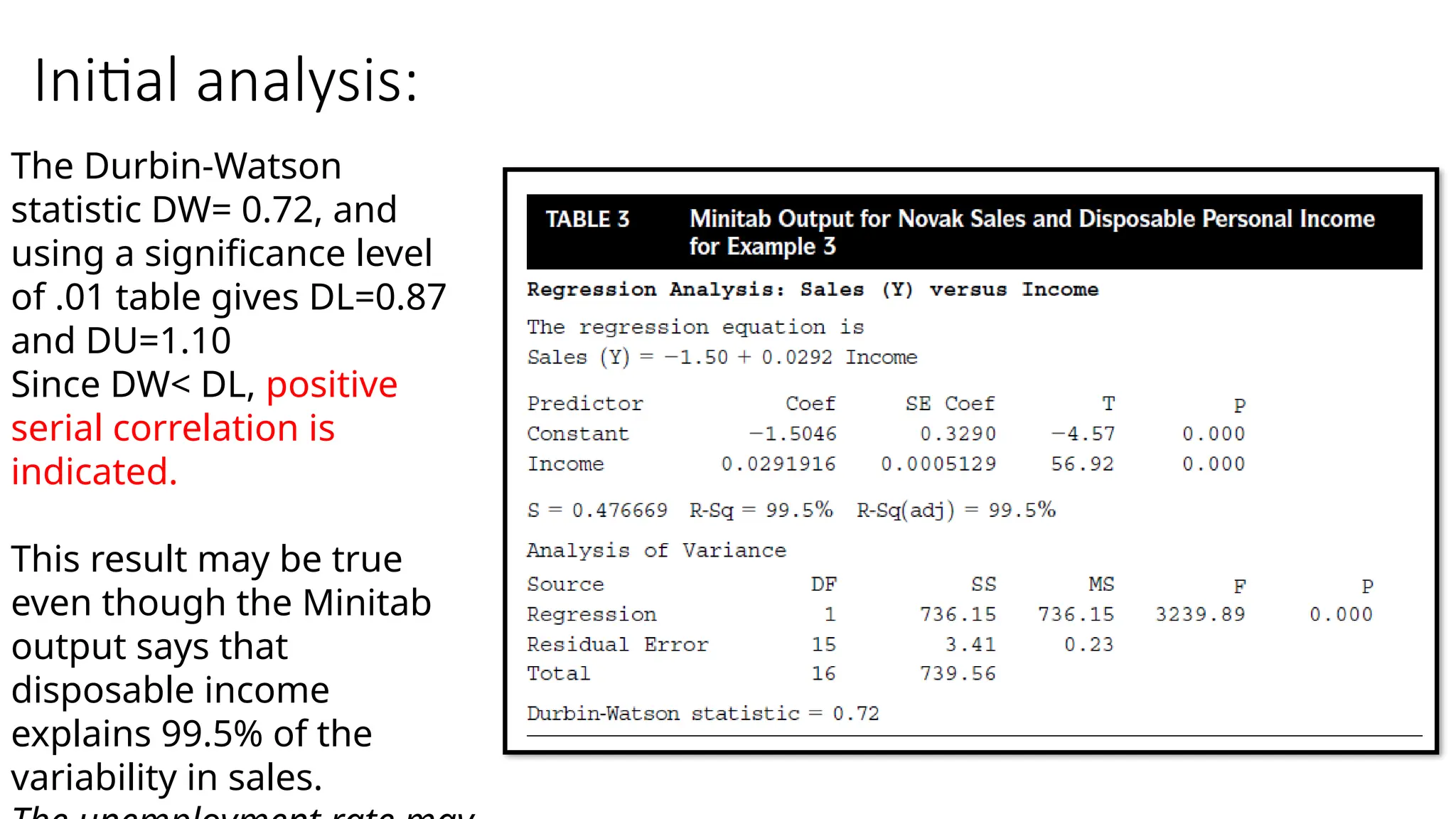

Initial analysis:

The Durbin-Watson

statisticDW= 0.72, and

using a significance level

of .01 table gives DL=0.87

and DU=1.10

Since DW< DL, positive

serial correlation is

indicated.

This result may be true

even though the Minitab

output says that

disposable income

explains 99.5% of the

variability in sales.

26.

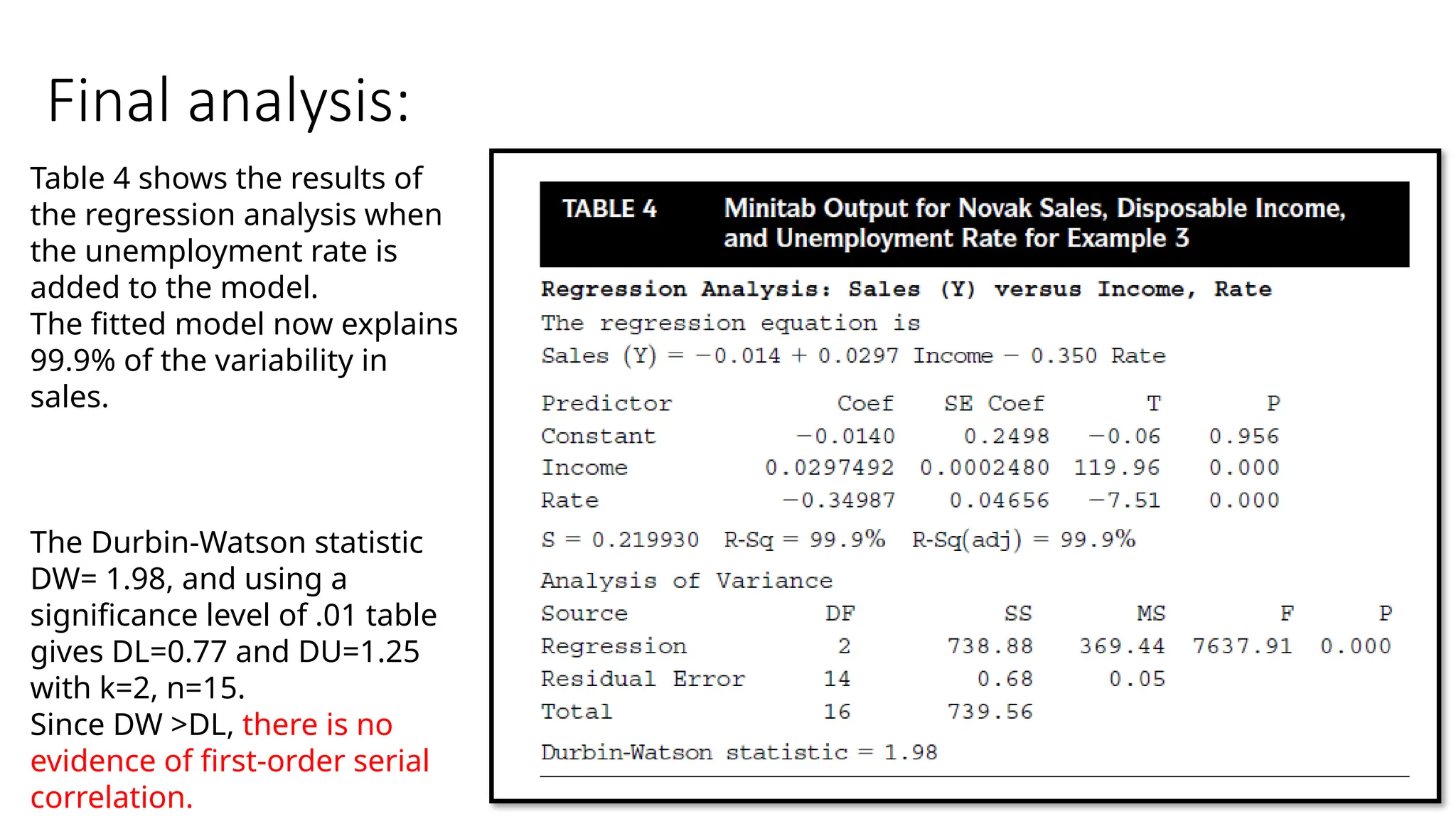

Final analysis:

Table 4shows the results of

the regression analysis when

the unemployment rate is

added to the model.

The fitted model now explains

99.9% of the variability in

sales.

The Durbin-Watson statistic

DW= 1.98, and using a

significance level of .01 table

gives DL=0.77 and DU=1.25

with k=2, n=15.

Since DW >DL, there is no

evidence of first-order serial

correlation.

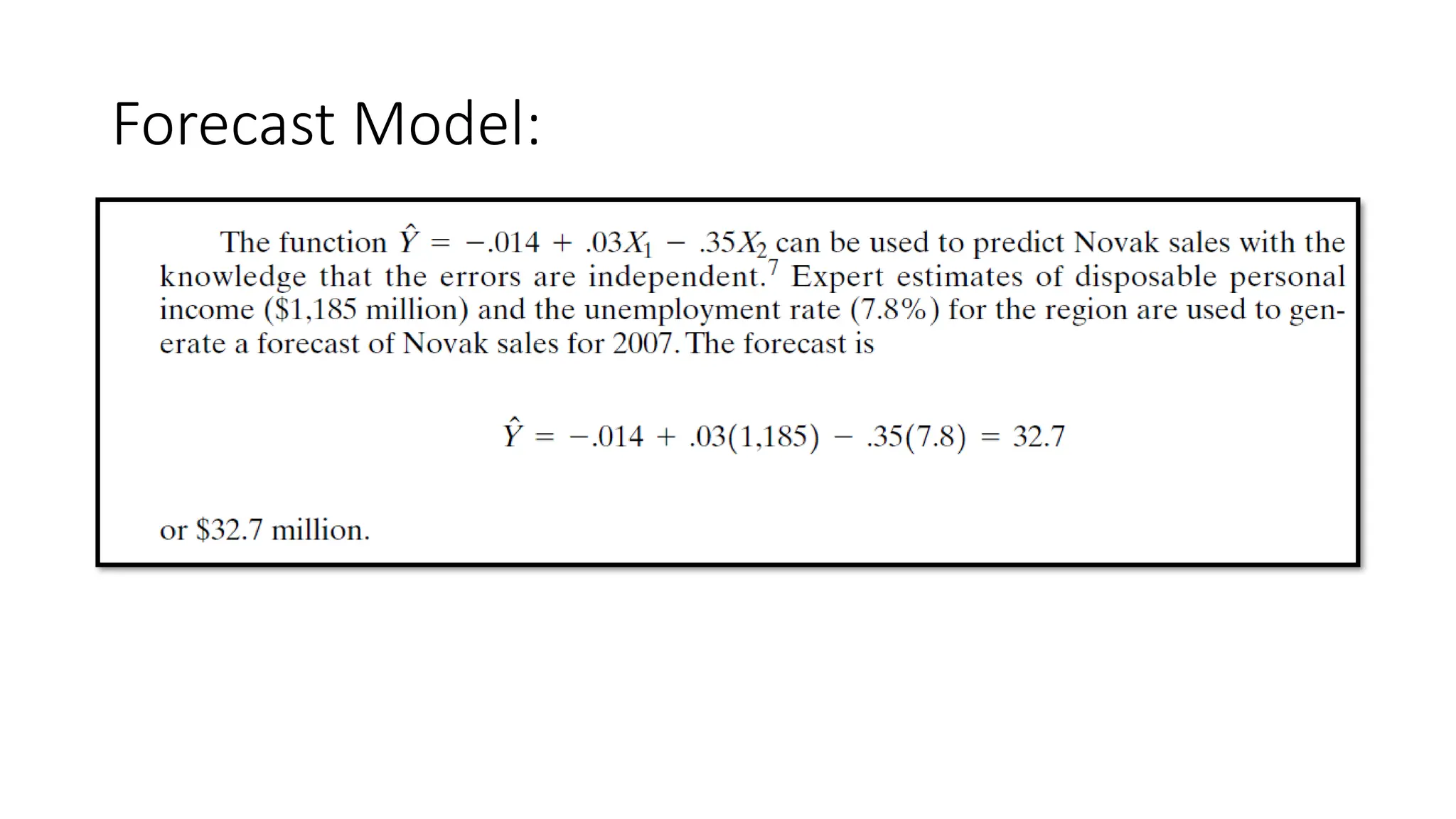

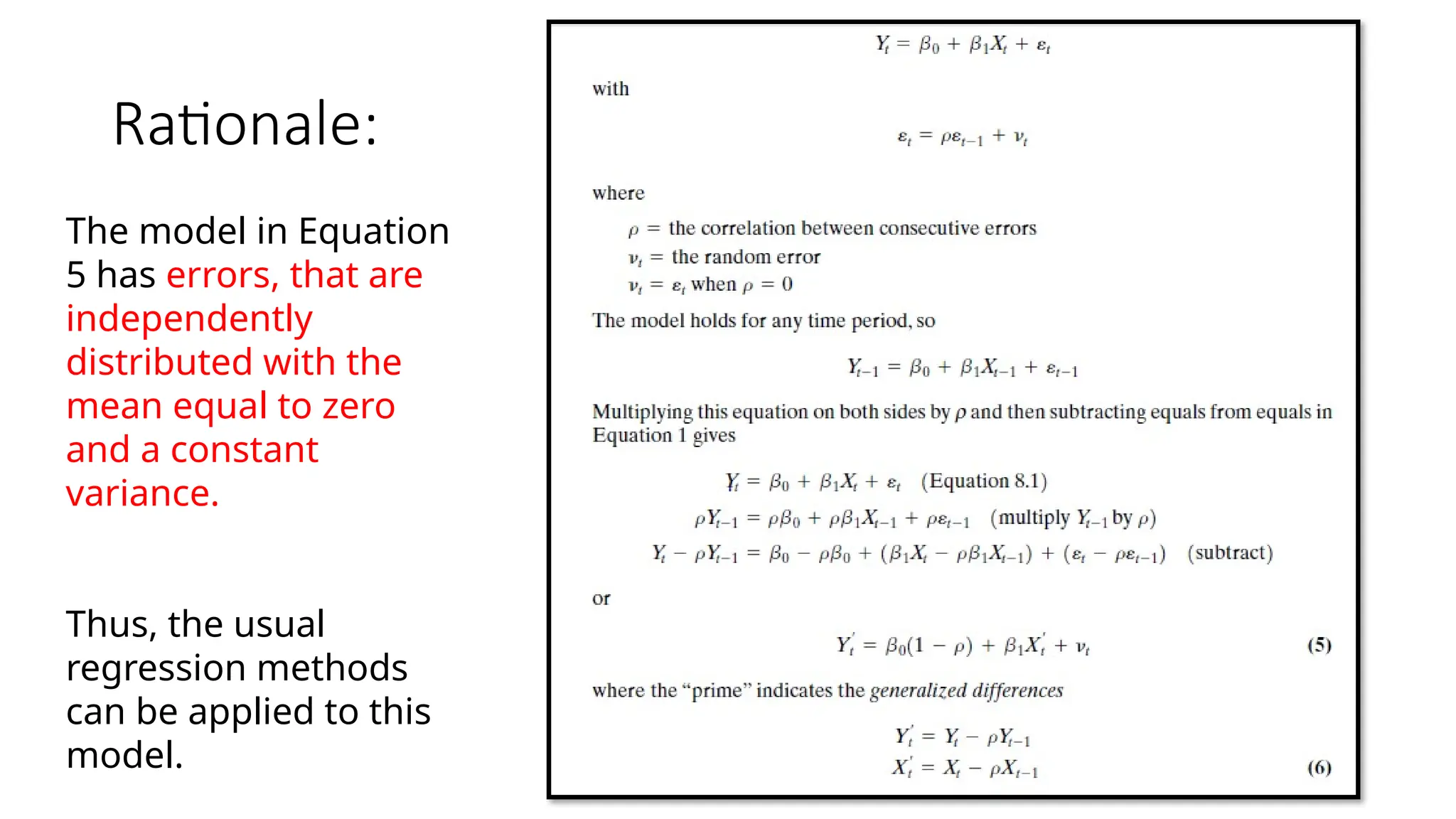

Rationale:

The model inEquation

5 has errors, that are

independently

distributed with the

mean equal to zero

and a constant

variance.

Thus, the usual

regression methods

can be applied to this

model.

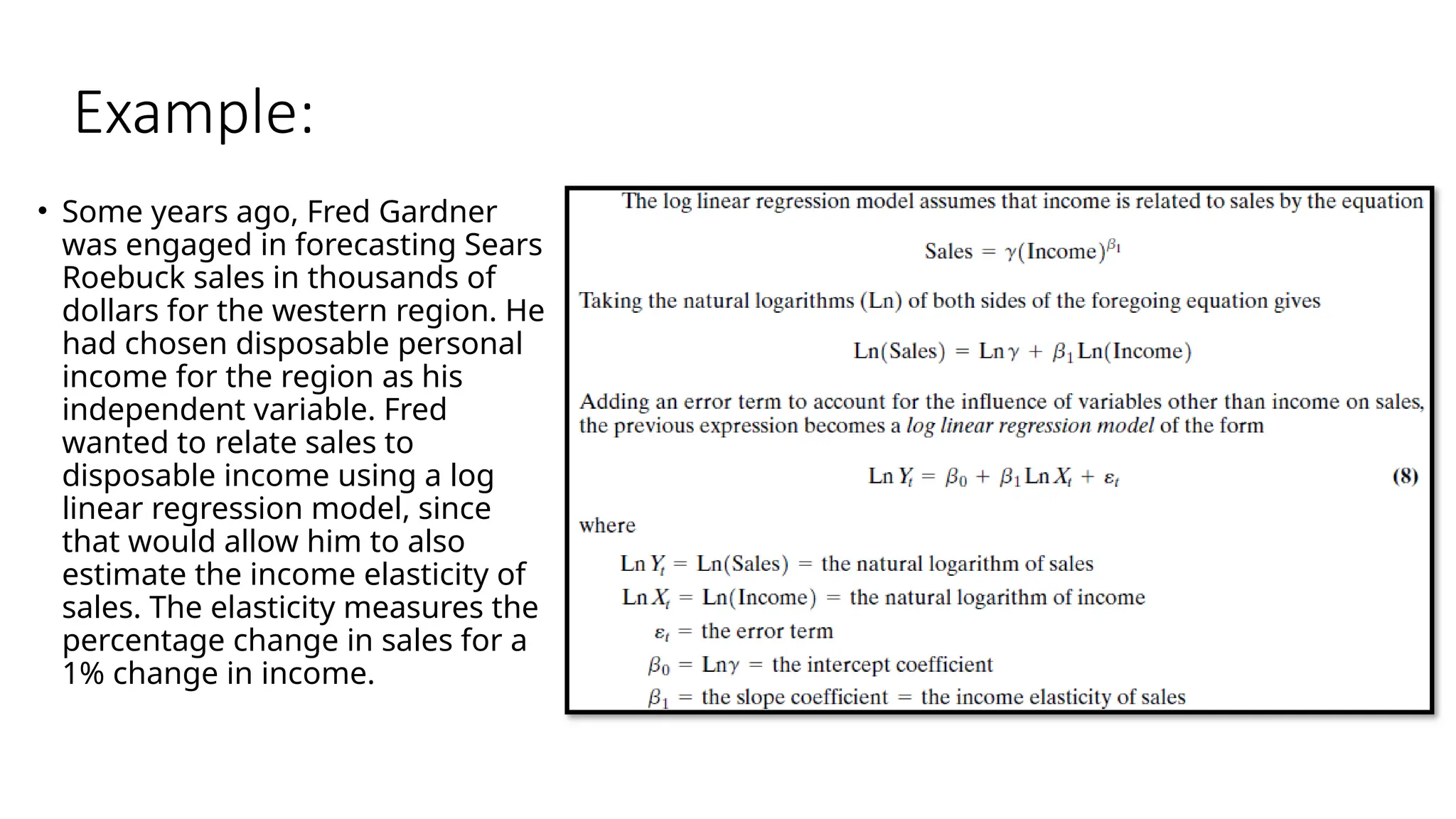

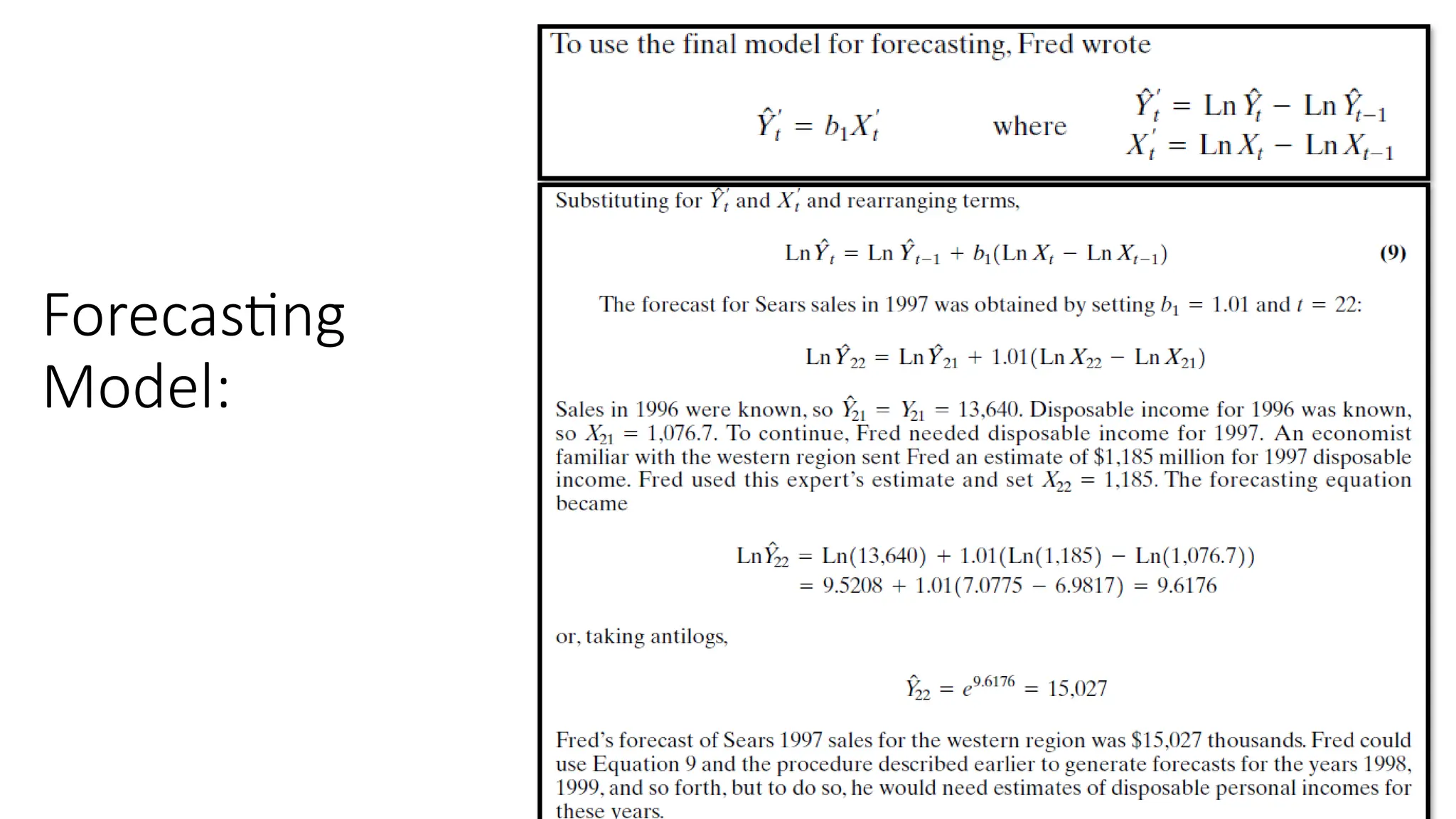

Example:

• Some yearsago, Fred Gardner

was engaged in forecasting Sears

Roebuck sales in thousands of

dollars for the western region. He

had chosen disposable personal

income for the region as his

independent variable. Fred

wanted to relate sales to

disposable income using a log

linear regression model, since

that would allow him to also

estimate the income elasticity of

sales. The elasticity measures the

percentage change in sales for a

1% change in income.

32.

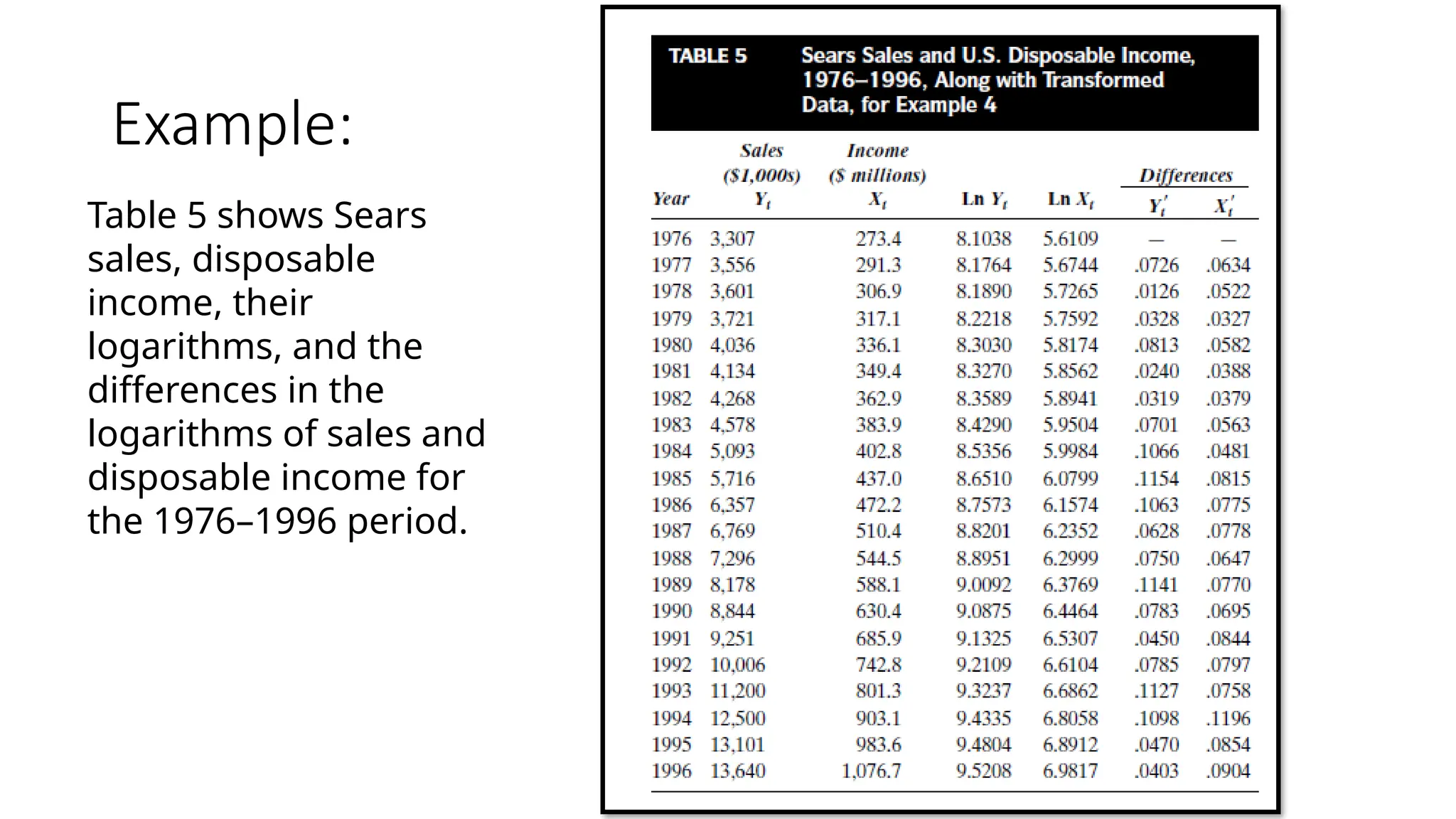

Example:

Table 5 showsSears

sales, disposable

income, their

logarithms, and the

differences in the

logarithms of sales and

disposable income for

the 1976–1996 period.

33.

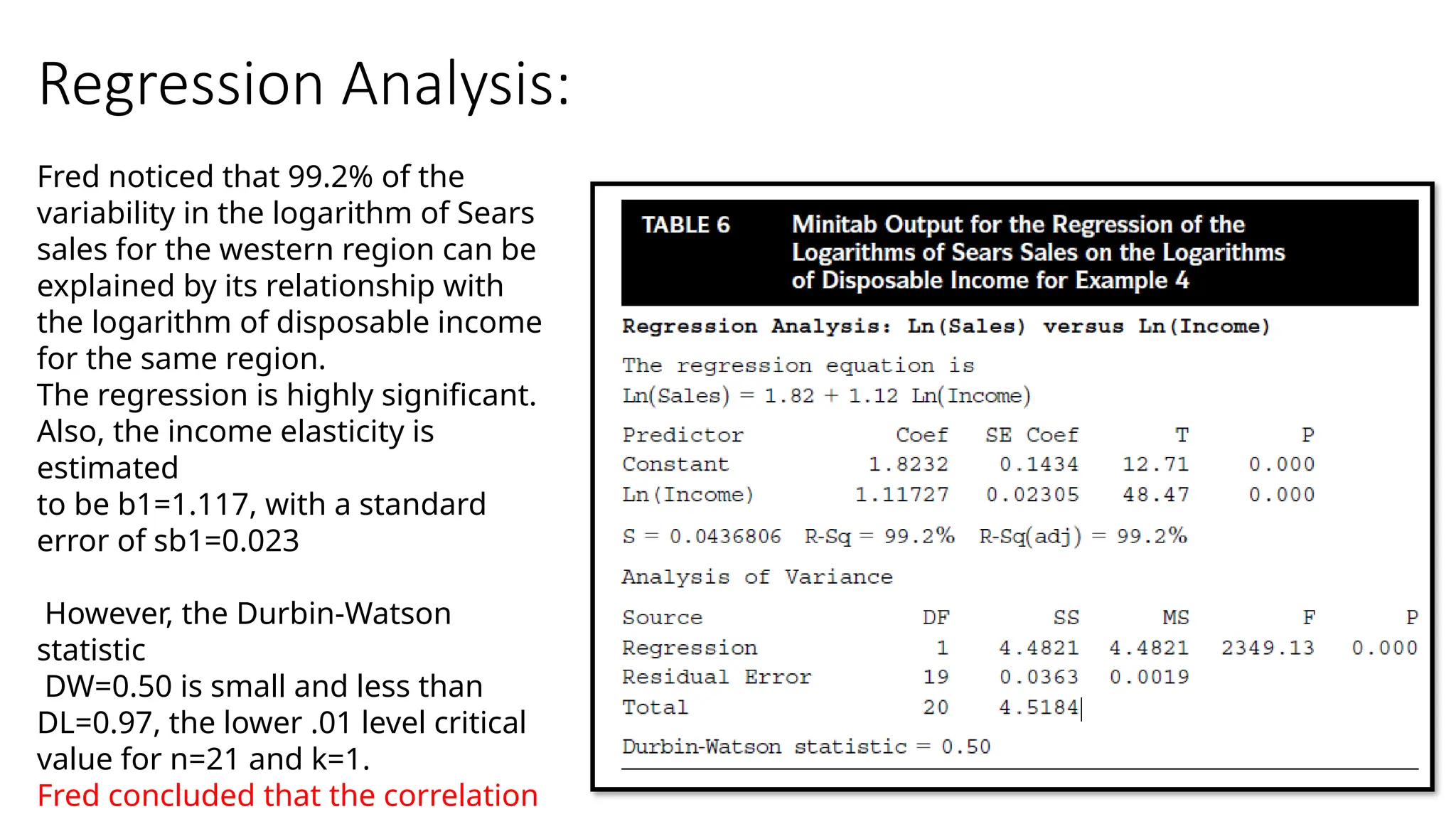

Regression Analysis:

Fred noticedthat 99.2% of the

variability in the logarithm of Sears

sales for the western region can be

explained by its relationship with

the logarithm of disposable income

for the same region.

The regression is highly significant.

Also, the income elasticity is

estimated

to be b1=1.117, with a standard

error of sb1=0.023

However, the Durbin-Watson

statistic

DW=0.50 is small and less than

DL=0.97, the lower .01 level critical

value for n=21 and k=1.

Fred concluded that the correlation

34.

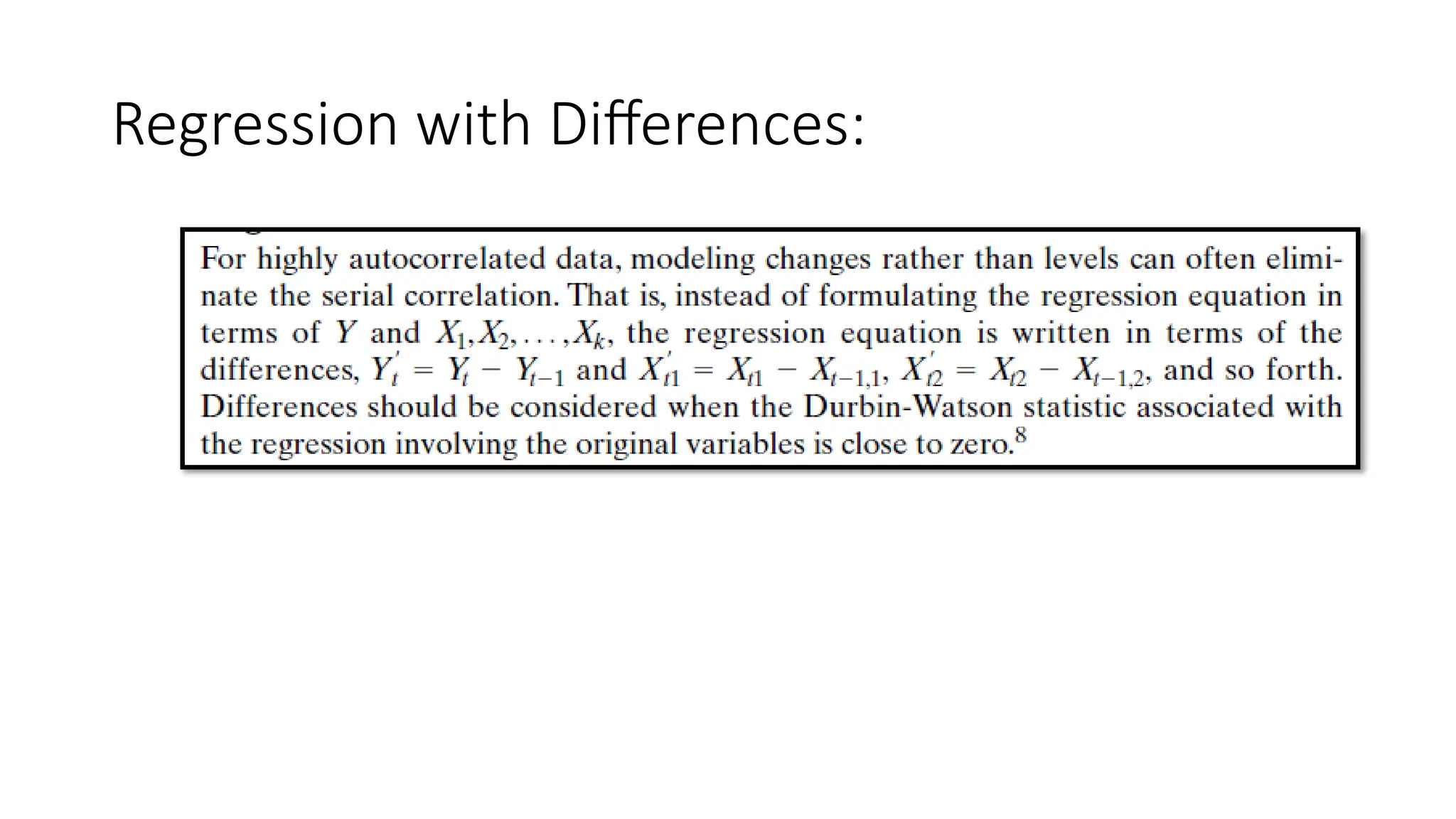

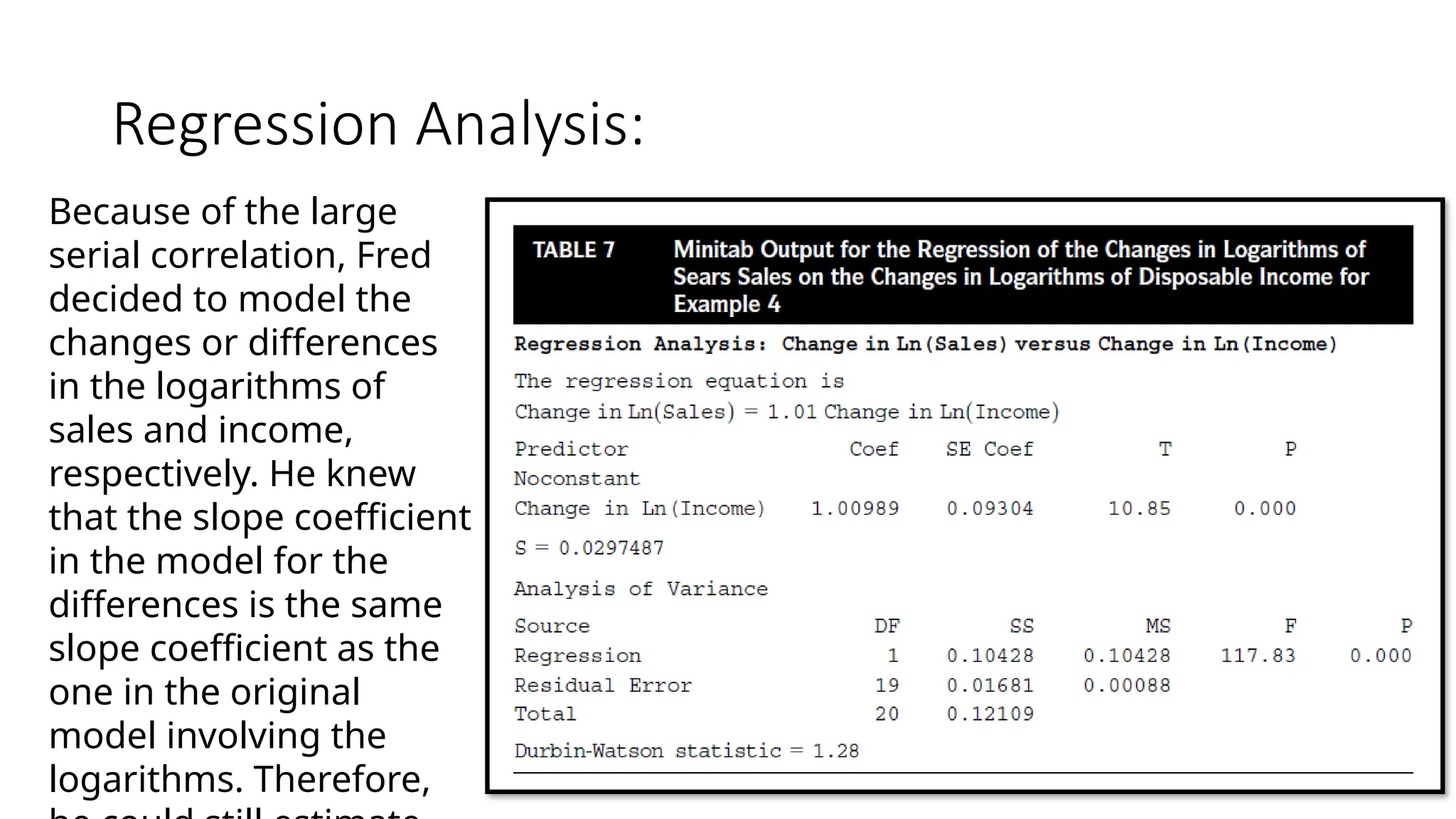

Regression Analysis:

Because ofthe large

serial correlation, Fred

decided to model the

changes or differences

in the logarithms of

sales and income,

respectively. He knew

that the slope coefficient

in the model for the

differences is the same

slope coefficient as the

one in the original

model involving the

logarithms. Therefore,

35.

Interpretation:

• The incomeelasticity is estimated to be b1=1.010, with a standard

error of sb1=0.093.The elasticity estimate b1 did not change too much

from the first regression (a 1% increase in disposable income leads to

an approximate 1% increase in annual sales in both cases), but its

current standard error sb1=0.093 is about four times as large as the

previous standard error sb1=0.023.The previous standard error is

likely to understate the true standard error due to the serial

correlation.

• Checking the Durbin-Watson statistic for n=20,k=1, and a significance

level of 0.05, Fred found that DL=1.20 ,DW=1.28 and DU=1.41, so the

test for positive serial correlation is inconclusive.

36.

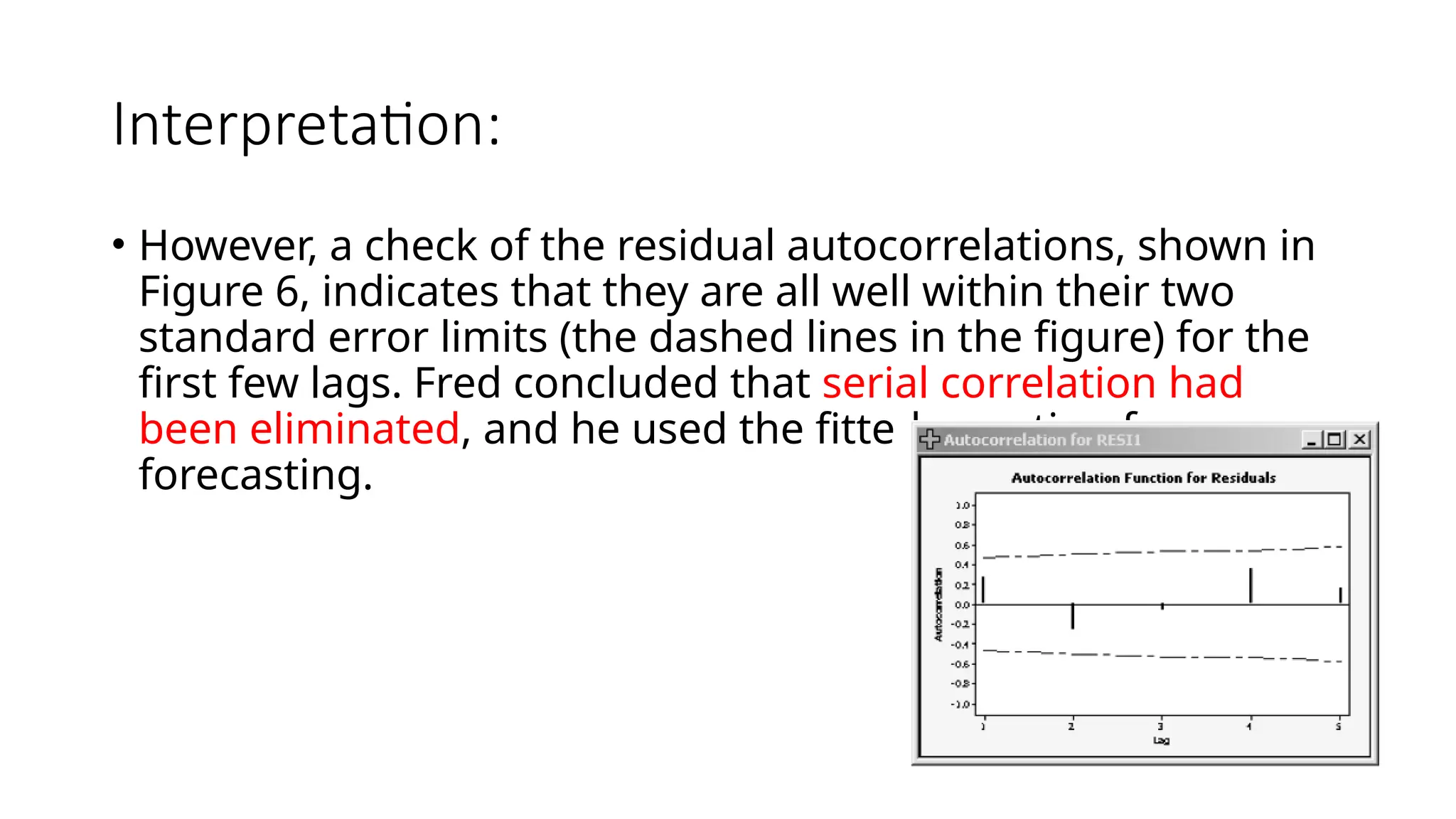

Interpretation:

• However, acheck of the residual autocorrelations, shown in

Figure 6, indicates that they are all well within their two

standard error limits (the dashed lines in the figure) for the

first few lags. Fred concluded that serial correlation had

been eliminated, and he used the fitted equation for

forecasting.

![[DSC Europe 25] Dusan Nesic - Securing Tomorrow’s Infrastructure: Why Cyber-P...](https://cdn.slidesharecdn.com/ss_thumbnails/qikbszfftyowjm2q6duw-1-251211083848-8f2ead6b-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dobrica Cosic - Savings by the Second: How Dynamic Pricing an...](https://cdn.slidesharecdn.com/ss_thumbnails/znp09f3smtqz3w2sq6wn-1-dobrica-cosic-savings-by-the-second-how-dynamic-pricing-and-smart-data-are-bu-251208151905-26e6f41e-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Milan Zdravkovic - The road less traveled in District Heating...](https://cdn.slidesharecdn.com/ss_thumbnails/nfaboniqwsz4ucyctnmy-2-milan-zdravkovic-dsc2025-the-road-less-traveled-in-district-heating-operation-251208151905-f56388a5-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Imai Jen-La Plante - The New Generation: AI and the Future of...](https://cdn.slidesharecdn.com/ss_thumbnails/kxi8t2l5rggivgcenyba-1-jenlaplante-dsc-251208152532-d1e076c2-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Milan Sekuloski - Data, Defence, and Development: Cybersecuri...](https://cdn.slidesharecdn.com/ss_thumbnails/dfrkwwx4qly6atqpbl4z-4-251209104645-c3d4b0ca-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dusan Pavlov - There Is No Spoon: Inferring Vision from Neura...](https://cdn.slidesharecdn.com/ss_thumbnails/wg0v1umoqjm4nnbd3p0v-there-is-no-spoon-251205085715-6d81d6c5-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Goran Obradovic - The Rise of Sovereign AI: Building the Regi...](https://cdn.slidesharecdn.com/ss_thumbnails/7nw2xxixrxqdxvrb5wca-6-251205085714-ab09a2ac-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dusan Jovicic - AI Story: From on-prem to cloud and back agai...](https://cdn.slidesharecdn.com/ss_thumbnails/8kp49m6uq22ifnbwhfnk-2-251205085715-964d11a6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Bogdan Daniel Maruneac - AI - It starts with you.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/odov3snhrcqs9hx5ny2n-4-251205085715-f1daacfe-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Sara Polak - The Ancient Operating System: What Archaeology T...](https://cdn.slidesharecdn.com/ss_thumbnails/3vch2p6tttdnwhsgazoz-3-sara-polak-smart-cities-251208152532-64404202-thumbnail.jpg?width=640&height=640&fit=bounds)