New Zealand: GST on cross-border supplies of remote services – are you ready?

•

1 like•294 views

New Zealand has now enacted new legislation that requires offshore suppliers of digital products and ‘remote services’ to register for, charge and remit GST (@ 15%) when they sell to New Zealand private consumers. This change takes effect on supplies made on or after 1 October 2016.

Recommended

More Related Content

What's hot

What's hot (14)

Similar to New Zealand: GST on cross-border supplies of remote services – are you ready?

Similar to New Zealand: GST on cross-border supplies of remote services – are you ready? (20)

More from Alex Baulf

More from Alex Baulf (20)

Recently uploaded

Recently uploaded (20)

New Zealand: GST on cross-border supplies of remote services – are you ready?

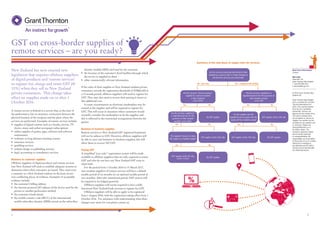

- 1. 21 GST on cross-border supplies of remote services – are you ready? New Zealand has now enacted new legislation that requires offshore suppliers of digital products and ‘remote services’ to register for, charge and remit GST (@ 15%) when they sell to New Zealand private consumers. This change takes effect on supplies made on or after 1 October 2016. A remote service is defined as a service that, at the time of the performance, has no necessary connection between the physical location of the recipient and the place where the services are performed. Examples of remote services include: • supplies of digital content such as e-books, movies, TV shows, music and online newspaper subscriptions • online supplies of games, apps, software and software maintenance • webinars or long distance learning courses • insurance services • gambling services • website design or publishing services • legal, accounting or consultancy services. Business to customer supplies Offshore suppliers of digital products and remote services into New Zealand will need to establish adequate systems to determine where their customers are based. They must treat a customer as a New Zealand resident on the basis of two non-conflicting pieces of evidence. Examples of acceptable evidence include: • the customer’s billing address • the internet protocol (IP) address of the device used by the person or another geolocation method • the customer’s bank details • the mobile country code (MCC) of the international mobile subscriber identity (IMSI) stored on the subscriber identity module (SIM) card used by the customer • the location of the customer’s fixed landline through which the service is supplied to them • other commercially relevant information. If the value of their supplies to New Zealand resident private consumers exceeds the registration threshold of NZ$60,000 in a 12 month period, offshore suppliers will need to register for GST. They may also need to review their pricing to factor in this additional cost. In some circumstances an electronic marketplace may be treated as the supplier and will be required to register for GST. This will occur in situations where customers would normally consider the marketplace to be the supplier, and this is reflected in the contractual arrangements between the parties. Business to business supplies Remote services to New Zealand GST registered businesses will not be subject to GST. However, offshore suppliers will be able to zero-rate business-to-business supplies; this will allow them to recover NZ GST. Paying GST A simplified “pay-only” registration system will be made available to offshore suppliers that are only required to return GST and who do not have any New Zealand GST costs to claim back. For the period from 1 October 2016 to 31 March 2017, non-resident suppliers of remote services will have a default taxable period of six months (or an optional taxable period of two months). After this transitional period, GST returns will be required to be lodged quarterly. Offshore suppliers will not be required to have a fully functional New Zealand bank account to register for GST. Offshore suppliers will be able to apply to be registered from 1 August 2016, with the registration taking effect from 1 October 2016. For assistance with understanding what these changes may mean for you please contact us. Need more information? Contact: Dan Lowe Associate, Tax Grant Thornton New Zealand T +64 (0)9 308 2531 E dan.lowe@nz.gt.com © 2016 Grant Thornton New Zealand Ltd. Grant Thornton New Zealand Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another’s acts or omissions. Please see www.grantthornton.co.nz for further details. This brochure is general in nature and its brevity could lead to misrepresentation. No responsibility can be accepted for those who act on its content without first consulting us and obtaining specific advice. Articles may be reprinted with our written permission. Are the services “remote services” supplied to a person resident in New Zealand? section 8(3)(c) Are the services supplied to a registered person for the purposes of their taxable activity? section 8(4) Are the services physically performed in New Zealand by a person who is in New Zealand at the time the services are performed? Are the services supplied to a registered person for the purposes of their taxable activity? section 8(4D) No GST applies The supplier chooses to treat the supply as a taxable supply? GST applies at the 15% rate GST applies at the 0% rate section 11A(1)(x) No GST applies Do the supplier and the registered person agree that the supply will be a taxable supply? GST applies at the 15% rate No GST applies GST applies at the 15% rate Summary of the new place of supply rules for services No - new rules Yes – existing section 8(3)(b) No No NoNo No YesYes Yes Yes Yes