Download to read offline

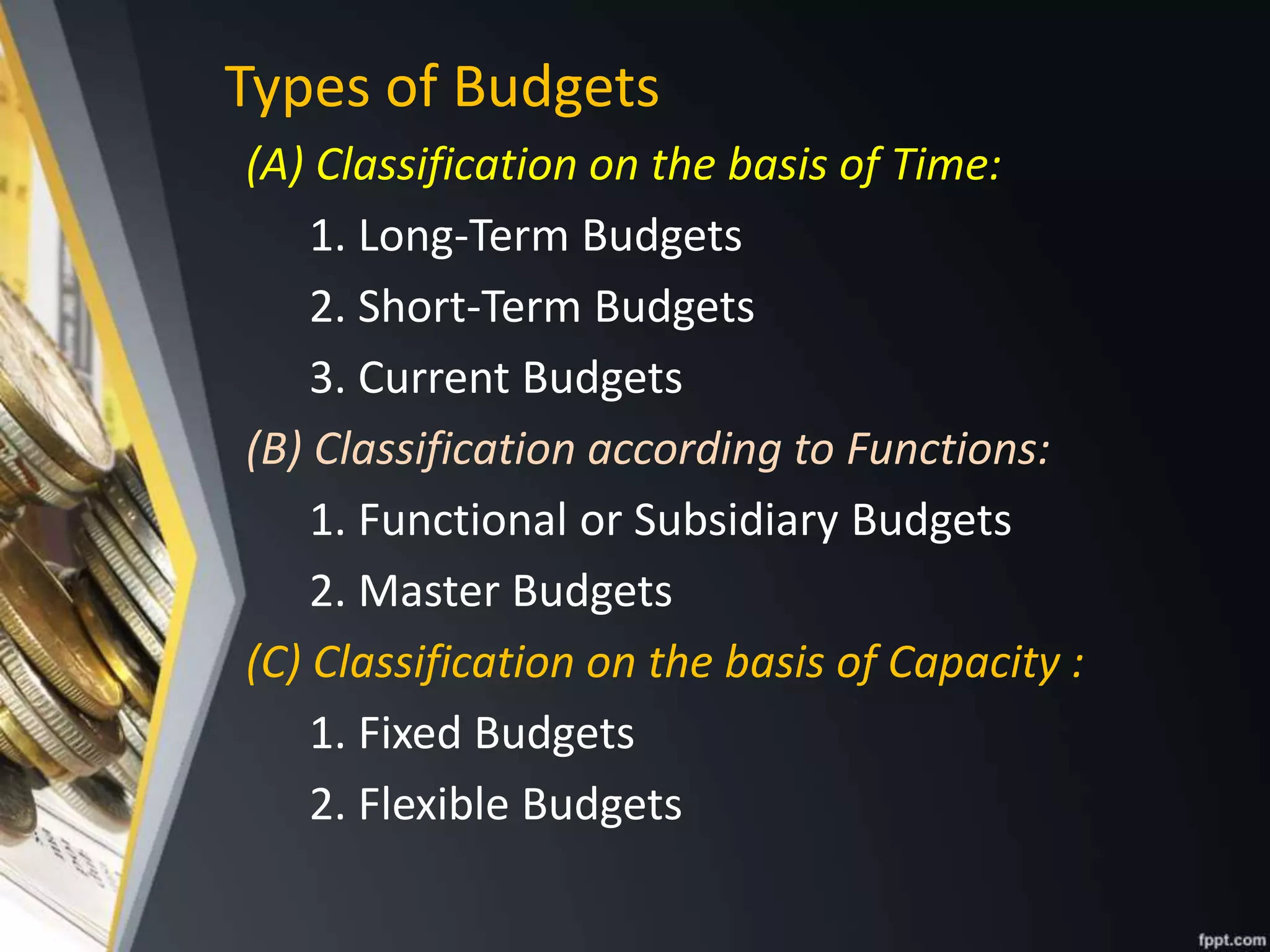

Budgetary control system involves creating budgets for financial planning and control. It includes: - Defining a budget as a financial plan for expenses and revenues over a period of time. - Describing features of budgets like being for a specific period and including definite numbers. - Explaining types of budgets like short-term vs long-term and functional vs master budgets. - Detailing approaches like zero-based budgeting, which requires justifying all spending, and performance budgeting, which relates costs to performance outcomes. - Noting the importance of flexible budgets that can adapt to different activity levels for planning and control.