Downloaded 30 times

![What is public sectors Bank?

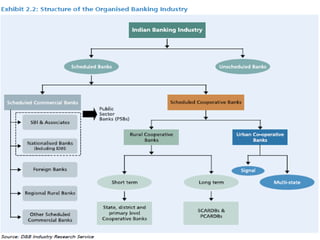

• Public Sector Banks (PSBs) are banks where a

majority stake (i.e. more than 50%) is held by a

government. The shares of these banks are listed

on stock exchanges. There are a total of 27 PSBs in

India [19 Nationalized banks + 6 State bank group

(SBI + 5 associates) + 1 IDBI bank (Other Public

Sector-Indian Bank) = 26 PSBs + 1 recent Bhartiya

Mahila Bank].](https://image.slidesharecdn.com/mfsassignment-141029010540-conversion-gate02/85/Public-Sectors-Bank-It-s-Services-3-320.jpg)

This document provides an overview of public sector banks in India. It discusses the history of banking in India beginning with banks established by the British East India Company in the early 19th century. It notes that many major banks were nationalized by the government in 1969 and 1980. The document defines public sector banks as those where the government holds over 50% stake and are listed on stock exchanges. It then outlines various banking services provided by public sector banks like deposits, credits, general services, customized services and products.