A SUMMARY OFLABOUR CODES

&

IMPACT THEREOF

21/11/25

l

4 labour Codes

India’s labour law regime has undergone a major overhaul.

With effect from 21 November 2025, the Central Government

has notified key provisions of all four labor codes—the Code

on Wages, Industrial Relations Code, Code on Social Security

and the OSHWC Code—consolidating 29 prior laws into a

unified framework. The notified provisions cover universal

minimum wages, expanded social security, uniform working

conditions, simplified dispute procedures and a single

registration/return system.

This Impact analysis with example outlines key features,

compliance obligations and penalties under each code.

Stakeholders must also verify the status of State rules, as

labour is a concurrent subject.”

2.

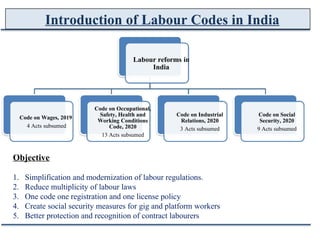

Introduction of LabourCodes in India

Labour reforms in

India

Code on Occupational,

Safety, Health and

Working Conditions

Code, 2020

Code on Industrial

Relations, 2020

Code on Social

Security, 2020

Code on Wages, 2019

4 Acts subsumed

3 Acts subsumed 9 Acts subsumed

13 Acts subsumed

Objective

1. Simplification and modernization of labour regulations.

2. Reduce multiplicity of labour laws

3. One code one registration and one license policy

4. Create social security measures for gig and platform workers

5. Better protection and recognition of contract labourers

3.

Highlights of Codeon Wages, 2019

Uniform applicability of payment of wages to all employees irrespective of wage ceiling and sector

Single and uniform definition of wages. Also, overtime rate cannot be lower than twice the

normal rate of wage

Separation by definition between worker and employee

Introduction of concept of ‘floor wage’ to be determined by CG on account of min living

standards of workers. Min wage rate cannot be lower than floor wage.

Conviction for sexual harassment considered as disqualification ground for receiving bonus.

Threshold limit for triggering applicability of Payment of Wages Act has been removed. Hence, these

provisions shall be applicable on all employees

4.

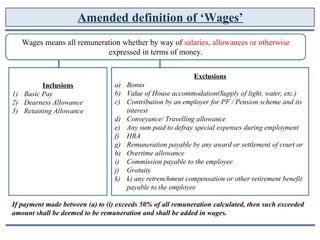

Amended definition of‘Wages’

Wages means all remuneration whether by way of salaries, allowances or otherwise

expressed in terms of money.

Exclusions

Inclusions

1) Basic Pay

2) Dearness Allowance

3) Retaining Allowance

a) Bonus

b) Value of House accommodation(Supply of light, water, etc.)

c) Contribution by an employer for PF / Pension scheme and its

interest

d) Conveyance/ Travelling allowance

e) Any sum paid to defray special expenses during employment

f) HRA

g) Remuneration payable by any award or settlement of court or

h) Overtime allowance

i) Commission payable to the employee

j) Gratuity

k) k) any retrenchment compensation or other retirement benefit

payable to the employee

If payment made between (a) to (i) exceeds 50% of all remuneration calculated, then such exceeded

amount shall be deemed to be remuneration and shall be added in wages.

5.

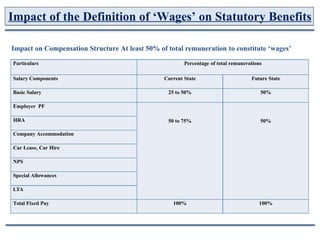

Impact of theDefinition of ‘Wages’ on Statutory Benefits

Impact on Compensation Structure At least 50% of total remuneration to constitute ‘wages’

Particulars Percentage of total remunerations

Salary Components

Basic Salary

Current State Future State

50%

25 to 50%

Employer PF

HRA 50 to 75% 50%

Company Accommodation

Car Lease, Car Hire

NPS

Special Allowances

LTA

Total Fixed Pay 100% 100%

6.

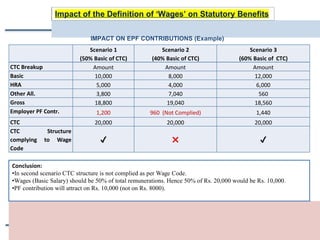

Impact of theDefinition of ‘Wages’ on Statutory Benefits

IMPACT ON EPF CONTRIBUTIONS (Example)

Scenario 1

(50% Basic of CTC)

Amount

Scenario 2

(40% Basic of CTC)

Amount

Scenario 3

(60% Basic of CTC)

Amount

CTC Breakup

Basic 10,000 8,000 12,000

HRA 5,000 4,000 6,000

Other All.

Gross

3,800

18,800

7,040

19,040

560

18,560

Employer PF Contr. 1,200 960 (Not Complied)

20,000

1,440

CTC 20,000 20,000

CTC Structure

complying to Wage

Code

Conclusion:

•In second scenario CTC structure is not complied as per Wage Code.

•Wages (Basic Salary) should be 50% of total remunerations. Hence 50% of Rs. 20,000 would be Rs. 10,000.

•PF contribution will attract on Rs. 10,000 (not on Rs. 8000).

7.

Impact of theDefinition of ‘Wages’ on Statutory Benefits

IMPACT ON MINIMUM WAGES- Contract Labour Centric

Example for minimum wages calculation: For worker (Uttarakhand) getting minimum wages Rs.

12,539 Per Months

Calculation as per

Calculation as per

Code

Sr. No

(a) Basic Salary

Earning Heads Pre-existing

enactments

Impact

9720

2819

12539

0

HRA – No more part of minimum wages.

(b) HRA (50 % of Basic Salary)

(c ) Monthly Gross Salary [ (a) + (b)]

(e) Deductions….

12539

(f) EE-PF Contr. (12 % of Basic Salary)

(g) EE-ESIC Contr. (0.75 % of Gross Salary)

(h) Total Deduction [ (f) + (g)]

1166

95

1505

95

PF contribution increased by Rs. 454

1261

11278

1600

10939

(i) Net Salary [ (c) - (h)] Net Salary decreased by Rs. 339

(j) Employer Contributions

(k) ER-PF Contr. (12 % of Basic Salary)

(l) ER-ESIC Contr. (3.25 % of Gross Salary)

(m) Total Employer Contributions [ (k) + (l)]

1166

408

1505

408

Employer PF contribution increased by Rs. 339

1574

14113

1913

14452

Employer Cost increased by Rs. 454

(n) Monthly CTC [ (c) + (m)] Total Contractor cost increased by Rs. 339

Conclusion:

•Above Analysis is for the Contractor labour, We can see the impact, Since HRA is no more part of minimum wages, Hence PF will be deducted on

minimum wages, resulting worker’s net salary will be reduced.

• Worker’s social security increased.

•Contractor’s cost will be increased.

8.

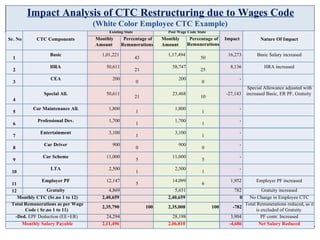

Impact Analysis ofCTC Restructuring due to Wages Code

(White Color Employee CTC Example)

Existing State Post Wage Code State

Sr. No CTC Components Monthly

Amount

Percentage of

Remunerations

Monthly

Amount

Percentage of Impact

Remunerations

Nature Of Impact

Basic

HRA

CEA

1,01,221 1,17,494 16,273 Basic Salary increased

HRA increased

1

2

3

43

21

0

50

25

0

50,611

200

58,747

200

8,136

-

Special Allowance adjusted with

Special All. 50,611 23,468 -27,143 increased Basic, ER PF, Gratuity

21 10

4

5

Car Maintenance All.

Professional Dev.

Entertainment

Car Driver

1,800

1,700

3,100

900

1,800

1,700

3,100

900

-

-

-

-

-

-

1

1

1

0

5

1

5

1

1

1

0

5

1

6

6

7

8

Car Scheme 11,000

2,500

12,147

11,000

2,500

14,099

9

LTA

10

Employer PF

Gratuity

1,952

782

Employer PF increased

11

12 4,869 5,651 Gratuity increased

Monthly CTC (Sr.no 1 to 12) 2,40,659 2,40,659 0 No Change in Employee CTC

Total Remunerations as per Wage

Code ( Sr.no 1 to 11)

Total Remunerations reduced, as it

is excluded of Gratuity

2,35,790 100 2,35,008 100 -782

-Ded. EPF Deduction (EE+ER) 24,294 28,198 3,904 PF contr. Increased

Net Salary Reduced

Monthly Salary Payable 2,11,496 2,06,810 -4,686

9.

Impact on Gratuity& Leave Encashment

Social benefit, Gratuity which was earlier calculated on the basic salary now will be computed on ‘wages’ which could

result in higher pay for the employee and a larger outgo for the employer. Big ticket components include a retrospective

increase in liability for benefits plan, such as Gratuity and leave encashment particularly for organizations where the

employee base is long tenure. Further this not only available to the permanent regular employees but also extended to

fixed term employment hence resulting in the financial cost to the company.

Example: An employee who has completed his continuous service more than 5 years

Monthly CTC

Basic Salary : (30% of Remunerations)

Tenure

1,00,000

30,000

8 years

30

Leave balance to encash

Impact Analysis

Post Wage Code State

Particulars Existing State (50 % of the remunerations will

constitute wages)

Impact Remark

Basic Salary

Completed Months

30,000

96

50000

96

20,000

Basic increased by 67%

-

Gratuity Provision 1,38,528

30,000

1,68,528

2,30,880

50,000

2,80,880

92,352

Gratuity increased by 67%

Leave Encashment increased by

67%

Total Employer Cost increased

by 67%

Leave Encashment Provision 20,000

Total Cost (Gratuity and Leave

Encashment)

1,12,352

Note: If Employer already processing the leave encashment on gross salary, in that case Leave encashment cost will reduce accordingly.

10.

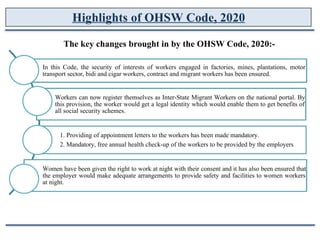

Highlights of OHSWCode, 2020

The key changes brought in by the OHSW Code, 2020:-

In this Code, the security of interests of workers engaged in factories, mines, plantations, motor

transport sector, bidi and cigar workers, contract and migrant workers has been ensured.

Workers can now register themselves as Inter-State Migrant Workers on the national portal. By

this provision, the worker would get a legal identity which would enable them to get benefits of

all social security schemes.

1. Providing of appointment letters to the workers has been made mandatory.

2. Mandatory, free annual health check-up of the workers to be provided by the employers

Women have been given the right to work at night with their consent and it has also been ensured that

the employer would make adequate arrangements to provide safety and facilities to women workers

at night.

11.

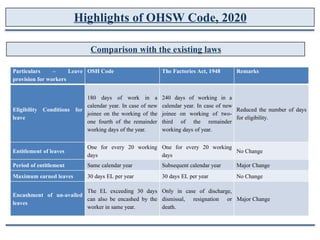

Highlights of OHSWCode, 2020

Comparison with the existing laws

Particulars – Leave OSH Code The Factories Act, 1948 Remarks

provision for workers

180 days of work in a 240 days of working in a

calendar year. In case of new calendar year. In case of new

joinee on the working of the joinee on working of two-

one fourth of the remainder third of the remainder

Eligibility Conditions for

leave

Reduced the number of days

for eligibility.

working days of the year. working days of year.

One for every 20 working One for every 20 working

Entitlement of leaves No Change

days days

Period of entitlement Same calendar year Subsequent calendar year Major Change

No Change

Maximum earned leaves 30 days EL per year 30 days EL per year

The EL exceeding 30 days Only in case of discharge,

Encashment of un-availed

leaves

can also be encashed by the dismissal, resignation or Major Change

worker in same year. death.

12.

Comparison with theexisting laws

Whether

Shops/Offices etc. to

provide such

facilities or not

[Y/N].

Sr. Revised worker Worker strength as per existing

Welfare facilities

No. strength in OSH Code provisions of factories Act, 1948

1 Canteen 100 or more 250 or more workers [Sec. 46]

30 or more women workers [Sec.

48]

Ye s [Sec. 24(1)(V)]

2. Creche facility 50 or more workers Ye s [Sec. 24(3)]

Washing Facilities, Bathing Facilities for

male female separately

Ye s [Sec. 24(1)(i) &

(ii)]

3. All All

4.

5.

Clock room/Locker etc. All

All

All

All

Ye s [Sec. 24(1)(iii)]

Ye s [Sec. 24(1)(iv)]

Sitting arrangement

6.

7.

First aid boxes All All Ye s [Sec. 24(1)(vii)]

No

Ambulance room 500 or more workers 500 or more workers (Sec. 45(4)]

8.

9.

Rest room / Lunch rooms 50 or more workers

250 or more workers

150 or more workers [Sec. 47]

500 or more workers [ Sec 49]

No

No

Welfare Officers in Factories

10. Safety Officer 500 or more workers 1000 or more workers [Sec. 40-B] No

No

11. Medical Officer

500 or more workers /

or carrying on 250 or more workers / or carrying

12. Safety Committee No

hazardous process

wherein 250 or more

on hazardous process

13.

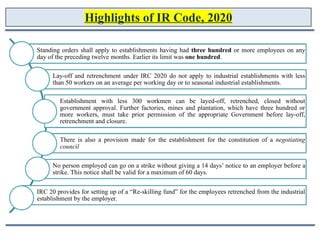

Highlights of IRCode, 2020

Standing orders shall apply to establishments having had three hundred or more employees on any

day of the preceding twelve months. Earlier its limit was one hundred.

Lay-off and retrenchment under IRC 2020 do not apply to industrial establishments with less

than 50 workers on an average per working day or to seasonal industrial establishments.

Establishment with less 300 workmen can be layed-off, retrenched, closed without

government approval. Further factories, mines and plantation, which have three hundred or

more workers, must take prior permission of the appropriate Government before lay-off,

retrenchment and closure.

There is also a provision made for the establishment for the constitution of a negotiating

council

No person employed can go on a strike without giving a 14 days’ notice to an employer before a

strike. This notice shall be valid for a maximum of 60 days.

IRC 20 provides for setting up of a “Re-skilling fund” for the employees retrenched from the industrial

establishment by the employer.

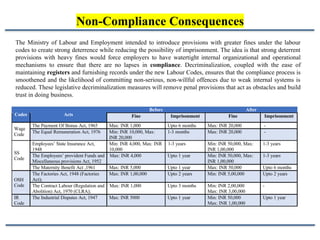

Non-Compliance Consequences

The Ministryof Labour and Employment intended to introduce provisions with greater fines under the labour

codes to create strong deterrence while reducing the possibility of imprisonment. The idea is that strong deterrent

provisions with heavy fines would force employers to have watertight internal organizational and operational

mechanisms to ensure that there are no lapses in compliance. Decriminalization, coupled with the ease of

maintaining registers and furnishing records under the new Labour Codes, ensures that the compliance process is

smoothened and the likelihood of committing non-serious, non-willful offences due to weak internal systems is

reduced. These legislative decriminalization measures will remove penal provisions that act as obstacles and build

trust in doing business.

Before After

Codes Acts Fine Imprisonment Fine Imprisonment

The Payment Of Bonus Act, 1965

The Equal Remuneration Act, 1976

Max: INR 1,000

Min: INR 10,000, Max:

INR 20,000

Upto 6 months

1-3 months

Max: INR 20,000

Max: INR 20,000

-

-

Wage

Code

Employees’ State Insurance Act,

1948

The Employees’ provident Funds and Max: INR 4,000

Miscellaneous provisions Act, 1952

Min: INR 4,000, Max: INR 1-3 years

10,000

Min: INR 50,000, Max:

INR 1,00,000

Min: INR 50,000, Max:

INR 1,00,000

1-3 years

1-3 years

SS

Code

Upto 1 year

The Maternity Benefit Act ,1961

The Factories Act, 1948 (Factories

Act);

The Contract Labour (Regulation and Max: INR 1,000

Abolition) Act, 1970 (CLRA);

Max: INR 5,000

Max: INR 1,00,000

Upto 1 year

Upto 2 years

Max: INR 50,000

Min: INR 5,00,000

Upto 6 months

Upto 2 years

OSH

Code Upto 3 months

Upto 1 year

Min: INR 2,00,000

Max: INR 3,00,000

Min: INR 50,000

Max: INR 1,00,000

-

IR

Code

The Industrial Disputes Act, 1947 Max: INR 5000 Upto 1 year

![Impact of the Definition of ‘Wages’ on Statutory Benefits

IMPACT ON MINIMUM WAGES- Contract Labour Centric

Example for minimum wages calculation: For worker (Uttarakhand) getting minimum wages Rs.

12,539 Per Months

Calculation as per

Calculation as per

Code

Sr. No

(a) Basic Salary

Earning Heads Pre-existing

enactments

Impact

9720

2819

12539

0

HRA – No more part of minimum wages.

(b) HRA (50 % of Basic Salary)

(c ) Monthly Gross Salary [ (a) + (b)]

(e) Deductions….

12539

(f) EE-PF Contr. (12 % of Basic Salary)

(g) EE-ESIC Contr. (0.75 % of Gross Salary)

(h) Total Deduction [ (f) + (g)]

1166

95

1505

95

PF contribution increased by Rs. 454

1261

11278

1600

10939

(i) Net Salary [ (c) - (h)] Net Salary decreased by Rs. 339

(j) Employer Contributions

(k) ER-PF Contr. (12 % of Basic Salary)

(l) ER-ESIC Contr. (3.25 % of Gross Salary)

(m) Total Employer Contributions [ (k) + (l)]

1166

408

1505

408

Employer PF contribution increased by Rs. 339

1574

14113

1913

14452

Employer Cost increased by Rs. 454

(n) Monthly CTC [ (c) + (m)] Total Contractor cost increased by Rs. 339

Conclusion:

•Above Analysis is for the Contractor labour, We can see the impact, Since HRA is no more part of minimum wages, Hence PF will be deducted on

minimum wages, resulting worker’s net salary will be reduced.

• Worker’s social security increased.

•Contractor’s cost will be increased.](https://image.slidesharecdn.com/labourcodes2025-251227111527-543e36bd/85/Labour-Codes-2025-what-are-changes-docx-7-320.jpg)

![Comparison with the existing laws

Whether

Shops/Offices etc. to

provide such

facilities or not

[Y/N].

Sr. Revised worker Worker strength as per existing

Welfare facilities

No. strength in OSH Code provisions of factories Act, 1948

1 Canteen 100 or more 250 or more workers [Sec. 46]

30 or more women workers [Sec.

48]

Ye s [Sec. 24(1)(V)]

2. Creche facility 50 or more workers Ye s [Sec. 24(3)]

Washing Facilities, Bathing Facilities for

male female separately

Ye s [Sec. 24(1)(i) &

(ii)]

3. All All

4.

5.

Clock room/Locker etc. All

All

All

All

Ye s [Sec. 24(1)(iii)]

Ye s [Sec. 24(1)(iv)]

Sitting arrangement

6.

7.

First aid boxes All All Ye s [Sec. 24(1)(vii)]

No

Ambulance room 500 or more workers 500 or more workers (Sec. 45(4)]

8.

9.

Rest room / Lunch rooms 50 or more workers

250 or more workers

150 or more workers [Sec. 47]

500 or more workers [ Sec 49]

No

No

Welfare Officers in Factories

10. Safety Officer 500 or more workers 1000 or more workers [Sec. 40-B] No

No

11. Medical Officer

500 or more workers /

or carrying on 250 or more workers / or carrying

12. Safety Committee No

hazardous process

wherein 250 or more

on hazardous process](https://image.slidesharecdn.com/labourcodes2025-251227111527-543e36bd/85/Labour-Codes-2025-what-are-changes-docx-12-320.jpg)

![Salient features on all labour codes ppt [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/salientfeaturesonalllabourcodes-pptcompatibilitymode-200108112830-thumbnail.jpg?width=640&height=640&fit=bounds)