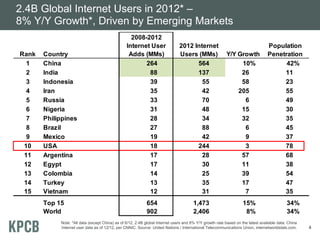

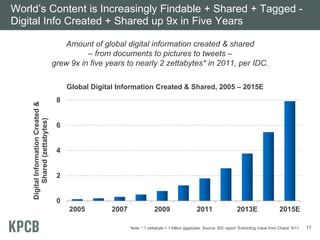

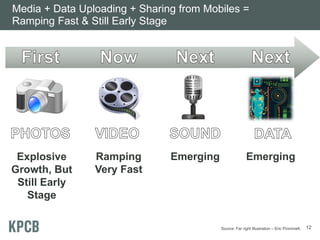

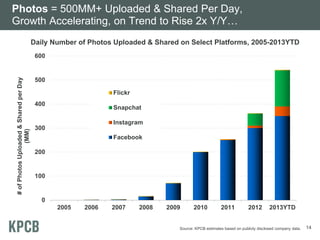

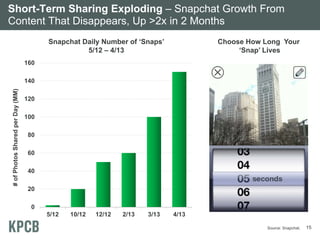

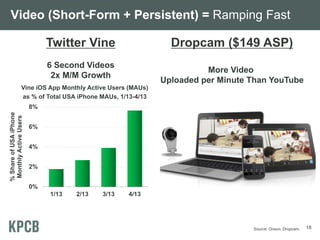

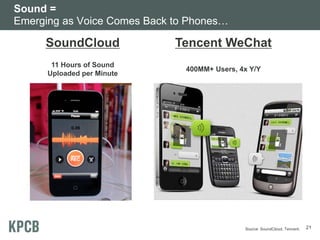

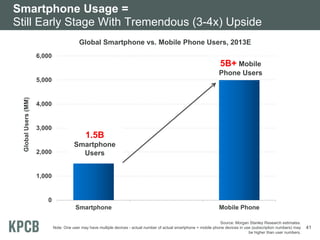

This document summarizes key internet trends from a 2013 conference. It finds that global internet users grew 8% in 2012 to over 2.4 billion users, driven largely by emerging markets like China and India. Mobile internet access is growing aggressively, surpassing 50% of total internet traffic. An increasing amount of content like photos, videos, and data is being uploaded and shared through mobile devices. Social media platforms are also seeing explosive growth in users and user-generated content.