Downloaded 163 times

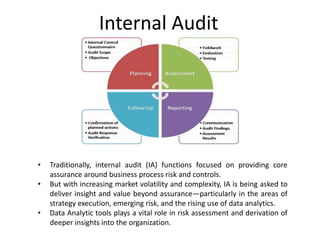

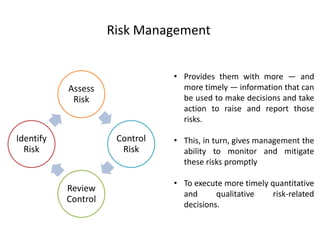

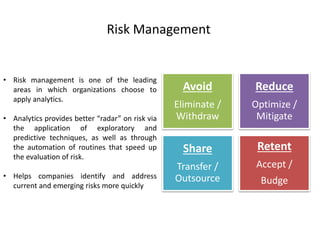

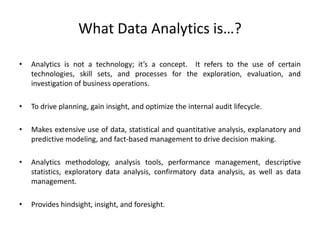

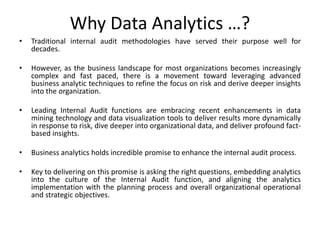

The document discusses the evolving role of internal audit (IA) functions from primarily providing assurance on business processes to delivering deeper insights through data analytics. It emphasizes the importance of analytics in risk management, enabling organizations to identify and address risks promptly, and improving the overall internal audit process. The implementation of advanced analytic techniques is seen as essential for meeting the expectations of management and enhancing the value provided by internal audit functions.

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)