Forward Looking Statement

g

Thispresentation of Guyana Goldfields Inc. (the "Company") contains statements that constitute "forward-looking statements." Such forward-looking statements involve

known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements, or developments in our industry, to differ

materially from the anticipated results, performance or achievements expressed or implied by such forward-looking statements. Forward looking statements are statements

y p , p p p y g g

that are not historical facts and are generally, but not always, identified by the words "expects," "aims," "plans," "anticipates," "believes," "intends," "estimates," "projects,"

"potential" and similar expressions, or that events or conditions "will," "would," "may," "could" or "should" occur. Information inferred from the interpretation of drilling results

and information concerning mineral resource estimates may also be deemed to be forward looking statements, as such information constitutes a prediction of what might

be found to be present when and if a project is actually developed. Forward-looking statements this document includes are statements regarding: the Company's

expectations regarding drilling and exploration activities on properties in which the Company has an interest; and the Company's statements regarding estimates of

resources on properties in which the Company has an interest. There can be no assurance that such statements will prove to be accurate. Actual results and future events

could differ materially from those anticipated in such statements, and readers are cautioned not to place undue reliance on these forward-looking statements that speak

y p p g p

only as of their respective dates. Important factors that could cause actual results to differ materially from the Company's expectations include among others, risks related

to fluctuations in mineral prices; uncertainties related to raising sufficient financing to fund planned work in a timely manner and on acceptable terms; changes in planned

work resulting from weather, logistical, technical or other factors; the possibility that results of work will not fulfill expectations and realize the perceived potential of the

Company's properties; uncertainties involved in the estimation of resources; the possibility that required permits may not be obtained on a timely manner or at all; the

possibility that capital and operating costs may be higher than currently estimated and may preclude commercial development or render operations uneconomic; the

possibility that the estimated recovery rates may not be achieved; risk of accidents, equipment breakdowns and labour disputes or other unanticipated difficulties or

interruptions; the possibility of cost overrun or unanticipated expenses in the work program; the risk of environmental contamination or damage resulting from the

Company's operations; risks associated with title to mineral properties; and other risks and uncertainties discussed appear elsewhere in the Company's documents filed

from time to time with the Toronto Stock Exchange and Canadian securities regulators. These statements are based on a number of assumptions, including assumptions

regarding general market conditions, the availability of financing for proposed transactions and programs on reasonable terms, and the ability of outside service providers

to deliver services in a satisfactory and timely manner. Forward-looking statements are based on the beliefs, estimates and opinions of the Company's management on the

date the statements are made. Except as expressly required by applicable securities laws, the Corporation undertakes no obligation to update these forward-looking

statements in the event that management's beliefs, estimates or opinions, or other factors, should change.

This presentation uses the terms "Inferred Resource", "Indicated Resource" and "Mineral Resource". The Company advises readers that although these terms are

This presentation uses the terms Inferred Resource , Indicated Resource and Mineral Resource . The Company advises readers that although these terms are

recognized and required by Canadian securities regulations (under National Instrument 43-101 "Standards of Disclosure for Mineral Projects"), the US Securities and

Exchange Commission does not recognize these terms. Readers are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be

converted into reserves. In addition, "Inferred Resources" have a great amount of uncertainty as to their existence, and economic and legal feasibility. It cannot be

assumed that any part of an Indicated or Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral

Resources may not form the basis of feasibility or pre-feasibility studies, or economic studies except for a Preliminary Assessment as defined and permitted under National

Instrument 43-101. Readers are cautioned not to assume that part or all of an inferred resource exists, or is economically or legally mineable. The Mineral Resources

stated in this news release are not mineral reserves and, in the absence of a current feasibility study, do not demonstrate economic viability. The determination of mineral

2

, y y, y

reserves can be affected by various factors including environmental, permitting, legal, title, taxation, socio-political, and marketing issues.

3.

Emerging Gold Producer

gg

6.7M oz

Aggressive

2011 drill

programs

growing

Resource

at Aurora

Expanding

on positive

PA results

programs PA results

Highly

prospective

exploration

portfolio

Mining

friendly

jurisdiction

p

Support

from the

IFC of the

Initial Sulphur

Rose Resource

3

IFC of the

World Bank

Group

Rose Resource

Estimate

4.

Corporate Snapshot

March 11,2011

Symbol: TSX: GUY Top 15 Shareholders Shares %

p p

y

Shares Issued 83,295,743

Options 6,893,658

Warrants 0

Diluted: 90 189 401

Top 15 Shareholders Shares %

Acuity (7 funds) 8.1M 9.7%

Franklin Resources (Templeton) 6.3M 7.6%

5.4M 6.5%

Patrick Sheridan Jr. (Founder/CEO)

Diluted: 90,189,401

52 week: Hi/Lo C$11.79 / C$6.13

3-month average volume: 467,702

Market Cap (at C$ 9.65) C$804 million

$

RBC Global 4.9M 5.9%

IFC (World Bank Group) 4.5M 5.4%

Van Eck 4.3M 5.2%

( )

Cash Position C$63 million

Monthly burn rate C$4 million

Debt $0

Symbol: Frankfurt: GG3

Manulife Financial (Canada) 3.0M 3.6%

Sprott (2 funds) 2.8M 3.4%

Tyrus Capital (UK) 2.5M 3.0%

Blackrock (UK) 2 0M 2 4%

Sy bo a u t GG3

WKN A0D975

ISIN CA4035301080

Blackrock (UK) 2.0M 2.4%

Mackenzie Financial 2.0M 2.4%

Columbia Wanger Asset Mgmt. 1.9M 2.3%

Oppenheimer Funds 1.8M 2.2%

Insider,7%

4

Carmignac Gestion 1.7M 2.0%

U.S. Global Investors 1.0M 1.2%

Retail 36%

Instit., 57%

5.

Analyst Coverage

y g

CormarkSecurities Inc.

Richard Gray, Target Price: $15.50 (02/28/11)

Buy

Paradigm Capital Speculative

Paradigm Capital

Don Blyth, Target Price: $15.00 (11/12/10)

Speculative

Buy

Outperform

BMO

Andrew Kaip, Target Price: $12.00 (02/28/11)

TD Newcrest

Speculative

Buy

Buy

TD Newcrest

Daniel Earle, Target Price: $14.00 (02/28/10)

Salman Partners

David West, Target Price: $13.75 (11/12/10)

D hl R & C

Dahlman Rose & Co.

Adam Graf, Target Price: $17.13 (02/28/11)

Buy

Outperform 2

Raymond James

Brad Humphrey, Target Price: $15.00 (02/28/11)

Scotia Capital

Trevor Turnbull, Target Price: $16.50 (02/28/11)

1-Sector

Outperform

Jennings Capital Inc.

Stuart McDougall, Target Price: $16.00 (02/16/11)

Speculative

Buy

5

RBC Capital Markets

Michael Curran, Target Price: $12.00 (03/02/11)

Sector Perform

6.

Management Team

g

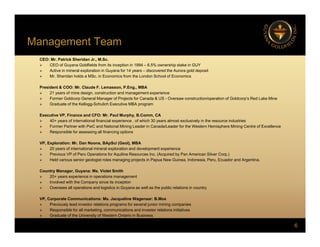

CEO: Mr.Patrick Sheridan Jr., M.Sc.

CEO of Guyana Goldfields from its inception in 1994 – 6.5% ownership stake in GUY

Active in mineral exploration in Guyana for 14 years – discovered the Aurora gold deposit

Mr Sheridan holds a MSc in Economics from the London School of Economics

Mr. Sheridan holds a MSc. in Economics from the London School of Economics

President & COO: Mr. Claude F. Lemasson, P.Eng., MBA

21 years of mine design, construction and management experience

Former Goldcorp General Manager of Projects for Canada & US - Oversaw construction/operation of Goldcorp’s Red Lake Mine

Graduate of the Kellogg-Schulich Executive MBA program

Executive VP, Finance and CFO: Mr. Paul Murphy, B.Comm, CA

40+ years of international financial experience , of which 30 years almost exclusively in the resource industries

Former Partner with PwC and National Mining Leader in Canada/Leader for the Western Hemisphere Mining Centre of Excellence

Responsible for assessing all financing options

VP, Exploration: Mr. Dan Noone, BApSci (Geol), MBA

20 years of international mineral exploration and development experience

Previous VP of Peru Operations for Aquiline Resources Inc. (Acquired by Pan American Silver Corp.)

Held various senior geologist roles managing projects in Papua New Guinea, Indonesia, Peru, Ecuador and Argentina.

Co ntr Manager G ana Ms Violet Smith

Country Manager, Guyana: Ms. Violet Smith

20+ years experience in operations management

Involved with the Company since its inception

Oversees all operations and logistics in Guyana as well as the public relations in country

VP, Corporate Communications: Ms. Jacqueline Wagenaar: B.Mos

6

Previously lead investor relations programs for several junior mining companies

Responsible for all marketing, communications and investor relations initiatives

Graduate of the University of Western Ontario in Business

7.

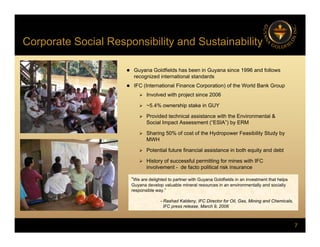

Corporate Social Responsibilityand Sustainability

p p y y

Guyana Goldfields has been in Guyana since 1996 and follows

recognized international standards

recognized international standards

IFC (International Finance Corporation) of the World Bank Group

Involved with project since 2006

~5.4% ownership stake in GUY

p

Provided technical assistance with the Environmental &

Social Impact Assessment (“ESIA”) by ERM

Sharing 50% of cost of the Hydropower Feasibility Study by

MWH

MWH

Potential future financial assistance in both equity and debt

History of successful permitting for mines with IFC

involvement - de facto political risk insurance

“We are delighted to partner with Guyana Goldfields in an investment that helps

Guyana develop valuable mineral resources in an environmentally and socially

responsible way.”

- Rashad Kaldeny IFC Director for Oil Gas Mining and Chemicals

7

- Rashad Kaldeny, IFC Director for Oil, Gas, Mining and Chemicals,

IFC press release, March 9, 2006

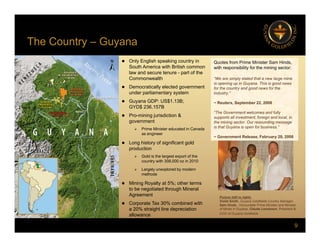

The Country –Guyana

Only English speaking country in

South America with British common

law and secure tenure - part of the

C lth

Quotes from Prime Minister Sam Hinds,

with responsibility for the mining sector:

y y

Commonwealth

Democratically elected government

under parliamentary system

Guyana GDP: US$1.13B;

GYD$ 236 157B

“We are simply elated that a new large mine

is opening up in Guyana. This is good news

for the country and good news for the

industry.”

~ Reuters, September 22, 2008

GYD$ 236.157B

Pro-mining jurisdiction &

government

Prime Minister educated in Canada

as engineer

“The Government welcomes and fully

supports all investment, foreign and local, in

the mining sector. Our resounding message

is that Guyana is open for business.”

~ Government Release, February 28, 2008

Long history of significant gold

production

Gold is the largest export of the

country with 308,000 oz in 2010

Largely unexplored by modern

Largely unexplored by modern

methods

Mining Royalty at 5%; other terms

to be negotiated through Mineral

Agreement

C %

Picture (left to right):

Violet Smith Guyana Goldfields Country Manager

9

Corporate Tax 30% combined with

a 20% straight line depreciation

allowance

Violet Smith, Guyana Goldfields Country Manager,

Sam Hinds, Honourable Prime Minister and Minister

of Mines in Guyana, Claude Lemasson, President &

COO of Guyana Goldfields

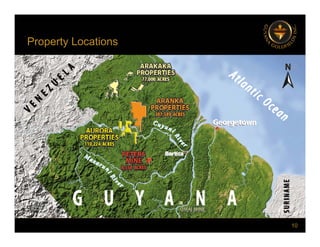

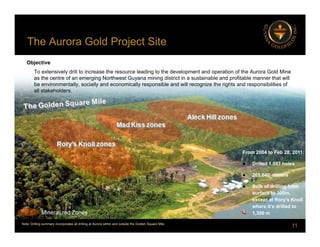

The Aurora GoldProject Site

j

Objective

To extensively drill to increase the resource leading to the development and operation of the Aurora Gold Mine

th t f i N th t G i i di t i t i t i bl d fit bl th t ill

as the centre of an emerging Northwest Guyana mining district in a sustainable and profitable manner that will

be environmentally, socially and economically responsible and will recognize the rights and responsibilities of

all stakeholders.

From 2004 to Feb 28, 2011:

Drilled 1,007 holes

265,640 meters

Bulk of drilling from

surface to 300m,

except at Rory’s Knoll

11

except at Rory s Knoll

where it’s drilled to

1,350 m

Mineralized Zones

Note: Drilling summary incorporates all drilling at Aurora within and outside the Golden Square Mile

12.

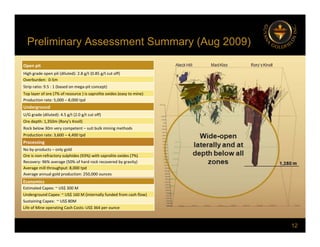

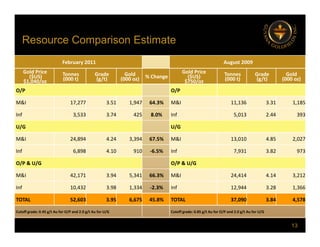

Preliminary Assessment Summary(Aug 2009)

y y ( g )

Open pit

High grade open pit (diluted): 2.8 g/t (0.85 g/t cut off)

Overburden: 0‐5m

Strip ratio: 9.5 : 1 (based on mega‐pit concept)

Top layer of ore (7% of resource ) is saprolite oxides (easy to mine)

Production rate: 5,000 – 8,000 tpd

Underground

Underground

U/G grade (diluted): 4.5 g/t (2.0 g/t cut off)

Ore depth: 1,350m (Rory’s Knoll)

Rock below 30m very competent – suit bulk mining methods

Production rate: 3,600 – 4,400 tpd

Processing

No by‐products – only gold

Ore is non‐refractory sulphides (93%) with saprolite oxides (7%)

Recovery: 96% average (50% of hard rock recovered by gravity)

Average mill throughput: 8,000 tpd

Average annual gold production: 250,000 ounces

Economics

Estimated Capex: ~ US$ 300 M

Underground Capex: ~ US$ 160 M (internally funded from cash flow)

Sustaining Capex: ~ US$ 80M

12

Sustaining Capex: US$ 80M

Life of Mine operating Cash Costs: US$ 364 per ounce

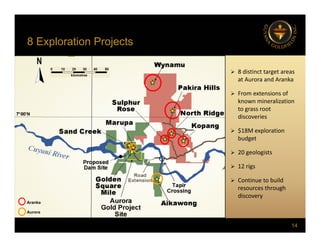

8 Exploration Projects

pj

8 distinct target areas

at Aurora and Aranka

From extensions of

known mineralization

to grass root

to grass root

discoveries

$18M exploration

budget

budget

20 geologists

12 rigs

A k

Continue to build

resources through

discovery

14

Aranka

Aurora

15.

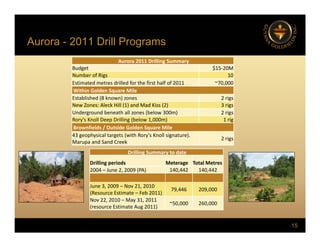

Aurora - 2011Drill Programs

g

Aurora 2011 Drilling Summary

Budget $15‐20M

Number of Rigs 10

Number of Rigs 10

Estimated metres drilled for the first half of 2011 ~70,000

Within Golden Square Mile

Established (8 known) zones 2 rigs

New Zones: Aleck Hill (1) and Mad Kiss (2) 3 rigs

g

Underground beneath all zones (below 300m) 2 rigs

Rory's Knoll Deep Drilling (below 1,000m) 1 rig

Brownfields / Outside Golden Square Mile

43 geophysical targets (with Rory's Knoll signature).

2 rigs

Marupa and Sand Creek

2 rigs

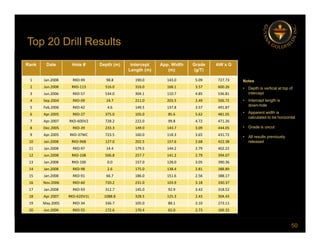

Drilling Summary to date

Drilling periods Meterage Total Metres

2004 – June 2 2009 (PA) 140 442 140 442

2004 – June 2, 2009 (PA) 140,442 140,442

June 3, 2009 – Nov 21, 2010

(Resource Estimate – Feb 2011)

79,446 209,000

Nov 22, 2010 – May 31, 2011

15

Nov 22, 2010 May 31, 2011

(resource Estimate Aug 2011)

~50,000 260,000

16.

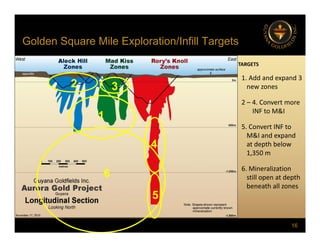

Golden Square MileExploration/Infill Targets

q p g

TARGETS

1 Add and e pand 3

1. Add and expand 3

new zones

2 – 4. Convert more

3

2

INF to M&I

5. Convert INF to

M&I and expand

1

p

at depth below

1,350 m

6. Mineralization

4

6

6. Mineralization

still open at depth

beneath all zones

5

6

16

17.

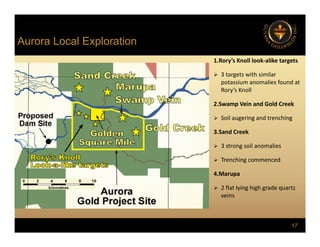

Aurora Local Exploration

p

1.Rory’sKnoll look‐alike targets

3 targets with similar

g

potassium anomalies found at

Rory’s Knoll

2.Swamp Vein and Gold Creek

Soil augering and trenching

3.Sand Creek

3 strong soil anomalies

Trenching commenced

4.Marupa

2 flat lying high grade quartz

veins

17

18.

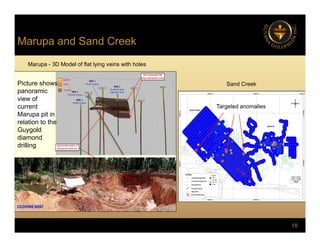

Marupa and SandCreek

p

Marupa - 3D Model of flat lying veins with holes

Picture shows

panoramic

view of

current

Sand Creek

Targeted anomalies

current

Marupa pit in

relation to the

Guygold

diamond

Targeted anomalies

diamond

drilling

18

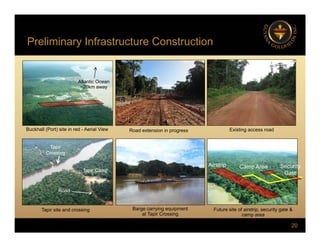

Preliminary Infrastructure Construction

y

AtlanticOcean

~20km away

Buckhall (Port) site in red - Aerial View Existing access road

Road extension in progress

Security

Camp Area

Airstrip

Tapir

Crossing

Tapir Camp

Gate

Tapir Camp

Road

20

Future site of airstrip, security gate &

camp area

Tapir site and crossing Barge carrying equipment

at Tapir Crossing

21.

Conceptual Site Plan– still in progress

p p g

River Dike

River Dike

Water

Management

Pond

Water

Management

Pond Open Pit

Area

Open Pit

Area

Shaft

Shaft

Airstrip

Airstrip

Cuyuni River

Area

Area

Process

Area

Process

Area

Mine Waste

Stockpile

Mine Waste

Stockpile

Camp

& Gate

Camp

& Gate

Mine Waste

Stockpile

Mine Waste

Stockpile

Proposed

Dam site

Proposed

Dam site

1

km

Tailings

Area

Tailings

Area

Clarification

Pond

Clarification

Pond

Access

Access

21

Yearly Rainfall = 2.5m

Yearly Rainfall = 2.5m

Access

Road

Access

Road

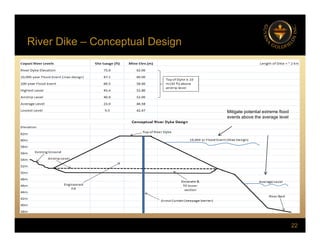

22.

River Dike –Conceptual Design

p g

Mitigate potential extreme flood

events above the average level

22

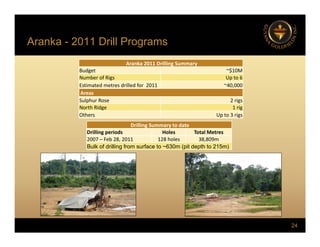

Aranka - 2011Drill Programs

g

Aranka 2011 Drilling Summary

Budget ~$10M

N b f Ri U t 6

Number of Rigs Up to 6

Estimated metres drilled for 2011 ~40,000

Areas

Sulphur Rose 2 rigs

North Ridge 1 rig

North Ridge 1 rig

Others Up to 3 rigs

Drilling Summary to date

Drilling periods Holes Total Metres

2007 Feb 28 2011 128 holes 38 809m

2007 – Feb 28, 2011 128 holes 38,809m

Bulk of drilling from surface to ~630m (pit depth to 215m)

24

25.

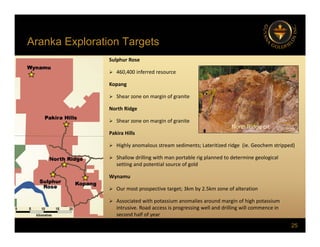

Aranka Exploration Targets

pg

Sulphur Rose

460,400 inferred resource

Kopang

Shear zone on margin of granite

North Ridge

North Ridge

Shear zone on margin of granite

Pakira Hills

North Ridge pit

Highly anomalous stream sediments; Lateritized ridge (ie. Geochem stripped)

Shallow drilling with man portable rig planned to determine geological

setting and potential source of gold

Wynamu

Our most prospective target; 3km by 2.5km zone of alteration

Associated with potassium anomalies around margin of high potassium

25

Associated with potassium anomalies around margin of high potassium

intrusive. Road access is progressing well and drilling will commence in

second half of year

26.

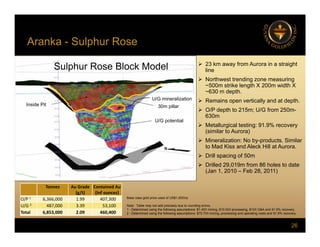

Aranka - SulphurRose

p

23 km away from Aurora in a straight

line

Sulphur Rose Block Model

Northwest trending zone measuring

~500m strike length X 200m width X

~630 m depth.

Remains open vertically and at depth.

O/P d th t 215 U/G f 250

Inside Pit 30m pillar

U/G mineralization

O/P depth to 215m; U/G from 250m-

630m

Metallurgical testing: 91.9% recovery

(similar to Aurora)

Mi li ti N b d t Si il

30m pillar

U/G potential

Mineralization: No by-products. Similar

to Mad Kiss and Aleck Hill at Aurora.

Drill spacing of 50m

Drilled 29,019m from 86 holes to date

(Jan 1 2010 Feb 28 2011)

(Jan 1, 2010 – Feb 28, 2011)

Tonnes Au Grade

(g/t)

Contained Au

(Inf ounces)

O/P 1 6,366,000 1.99 407,300 Base case gold price used of US$1,000/oz

26

U/G 2 487,000 3.39 53,100

Total 6,853,000 2.09 460,400

Note: Table may not add precisely due to rounding errors.

1 - Determined using the following assumptions: $1.45/t mining, $10.02/t processing, $10/t G&A and 91.9% recovery.

2 - Determined using the following assumptions: $75.70/t mining, processing and operating costs and 91.9% recovery.

27.

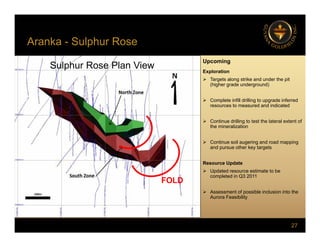

Aranka - SulphurRose

p

Upcoming

Exploration

Sulphur Rose Plan View

Targets along strike and under the pit

(higher grade underground)

Complete infill drilling to upgrade inferred

resources to measured and indicated

Continue drilling to test the lateral extent of

the mineralization

Continue soil augering and road mapping

and pursue other key targets

Resource Update

Updated resource estimate to be

Updated resource estimate to be

completed in Q3 2011

Assessment of possible inclusion into the

Aurora Feasibility

FOLD

27

28.

Plans for 2011

Critical Advancement of the Aurora Gold Project

Strategic Exploration Drilling – Ongoing

Hydropower F.S. – Q3 2011

Obtain Mining License (Permit) – 2011

Aurora revised Resource Estimate – Q3 2011

Evaluate Project Financing – Q3/Q4 2011

F ibilit St d NI43 101 Q4 2011

Feasibility Study - NI43-101 - Q4 2011

Start of Aurora Development & Construction – Q4 2011

Aggressive Exploration at Aranka Properties

Strategic Exploration Drilling – Ongoing

Updated Resource Estimate at Sulphur Rose –Q3 2011

p p Q

28

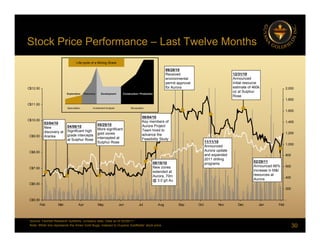

Stock Price Performance– Last Twelve Months

09/28/10

Received

Life-cycle of a Mining Share

12/31/10

C$11.00

C$12.00

1,800

2,000

environmental

permit approval

for Aurora

Speculation Investment Analysis Revaluation

Development Construction / Production

Discovery

Exploration

Announced

initial resource

estimate of 460k

oz at Sulphur

Rose

C$9.00

C$10.00

1,200

1,400

1,600

04/06/10

Significant high

grade intercepts

at Sulphur Rose

05/25/10

More significant

gold zones

intercepted at

03/04/10

New

discovery at

Aranka

08/04/10

Key members of

Aurora Project

Team hired to

advance the

Feasibility Study

Speculation Investment Analysis Revaluation

C$7.00

C$8.00

600

800

1,000

at Sulphur Rose

te cepted at

Sulphur Rose

Feasibility Study

08/18/10

New zones

11/11/10

Announced

Aurora update

and expanded

2011 drilling

programs

02/28/11

Announced 66%

increase in M&I

C$5.00

C$6.00

-

200

400

extended at

Aurora, 70m

@ 3.0 g/t Au

increase in M&I

resources at

Aurora

$

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb

30

Source: FactSet Research Systems, company data. Data as of 02/28/11.

Note: White line represents the Amex Gold Bugs, indexed to Guyana Goldfields' stock price.

31.

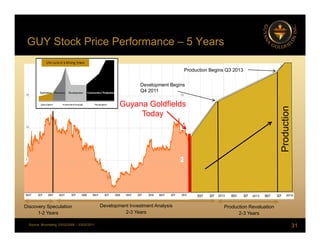

GUY Stock PricePerformance – 5 Years

Production Begins Q3 2013

Guyana Goldfields

Development Begins

Q4 2011

n

y

Today

oduction

Pro

2012 2013 2014

31

Source: Bloomberg, 03/02/2006 – 03/02/2011

Discovery Speculation

1-2 Years

Development Investment Analysis

2-3 Years

Production Revaluation

2-3 Years

32.

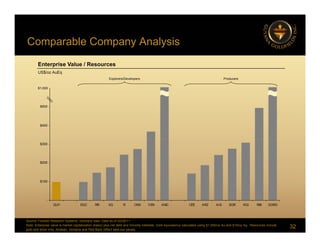

Comparable Company Analysis

pp y y

Enterprise Value / Resources

US$/oz AuEq

$500

$600

Producers

Explorers/Developers

$1,000

$400

$

$200

$300

-

$100

32

Source: FactSet Research Systems, company data. Data as of 02/28/11.

Note: Enterprise value is market capitalization (basic) plus net debt and minority interests. Gold equivalency calculated using $1,000/oz Au and $18/oz Ag. Resources include

gold and silver only. Andean, Ventana and Red Back reflect take-out values.

GUY DGC RR XG R OSK VEN AND CEE ARZ AGI SGR KGI RBI GORO

33.

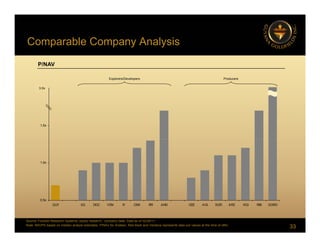

Comparable Company Analysis

pp y y

P/NAV

2.0x

Producers

Explorers/Developers

3.0x

1.5x

1.0x

0.5x

33

Source: FactSet Research Systems, equity research, company data. Data as of 02/28/11.

Note: NAVPS based on median analyst estimates. P/NAV for Andean, Red Back and Ventana represents take-out values at the time of offer.

GUY XG DGC VEN R OSK RR AND CEE AGI SGR ARZ KGI RBI GORO

34.

Summary Checklist

y

Company Establishedwith cash

Management & Development Teams

Region

C t ( t d it )

In place with experience and depth

Guiana Shield – known gold region

P i i ll t l ti

Country (government and community)

Sustainability

Exploration Activities

Pro-mining, excellent relations

International standards with IFC

Active with key targets

Potential Mega-pit in Golden Mile

Over 6.7M Oz with strong grades

Significant with more drilling

Exploration Activities Active with key targets

Aurora Project

Current Resources & Grades

Resource Upside Significant with more drilling

Excellent accessible location

Awarded and in progress

Highly profitable mine

Resource Upside

Key Infrastructure

Key Studies & Permitting

Current Internal Assessment

34

Plan and Budget for 2011 Advancing all key activities

35.

The Future

The AuroraProject is progressing

to be a large, highly profitable

The Aurora Project is progressing

to be a large, highly profitable

world-class gold mine developed

and coming on-line in the next 3

world-class gold mine developed

and coming on-line in the next 3

TSX: GUY

Frankfurt: GG3

www.guygold.com

and coming on line in the next 3

years!

and coming on line in the next 3

years!

35

36.

Contact Information

Head Office:

HeadOffice:

Guyana Goldfields Inc. Telephone: (416) 628 5936

141 Adelaide St. West, Suite 1608 Fax: (416) 628 5935

Toronto ON M5H 3L5 Email: info@guygold com

Toronto, ON M5H 3L5 Email: info@guygold.com

Investor Queries:

Vice-President , Corporate Communications

Jacqueline Wagenaar

Jacqueline Wagenaar

Telephone: (416) 628 5936 Ext. 2295

Email: jwagenaar@guygold.com

36

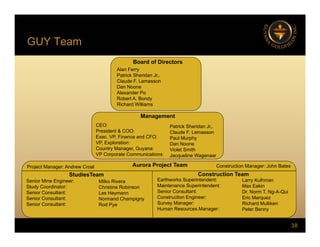

GUY Team

Board ofDirectors

Alan Ferry

Patrick Sheridan Jr,.

Patrick Sheridan Jr,.

Claude F. Lemasson

Dan Noone

Alexander Po

Robert A. Bondy

Richard Williams

Management

CEO:

President & COO:

Exec. VP, Finance and CFO:

Patrick Sheridan Jr,.

Claude F. Lemasson

Paul Murphy

,

VP, Exploration:

Country Manager, Guyana:

VP Corporate Communications:

Aurora Project Team

Project Manager: Andrew Croal

Paul Murphy

Dan Noone

Violet Smith

Jacqueline Wagenaar

Construction Manager: John Bates

Senior Mine Engineer:

Study Coordinator:

Senior Consultant:

Senior Consultant:

StudiesTeam Construction Team

Earthworks Superintendent:

Maintenance Superintendent:

Senior Consultant:

Construction Engineer:

S M

Milko Rivera

Christine Robinson

Les Heymann

Normand Champigny

Larry Kulhman

Max Eakin

Dr. Norm T. Ng-A-Qui

Eric Marquez

38

Senior Consultant: Survey Manager:

Human Resources Manager:

p g y

Rod Pye Richard Mulliken

Peter Benny

39.

Board of Directors

AlanFerry, CFA, Geologist: Director (Lead)

Alan Ferry is an independent businessman since 2007 following over 27 years as a mining analyst and mining corporate finance specialist. Prior

to that, he worked as a geologist.

Patrick Sheridan Jr., MSc: Founder, CEO and Director

Mr. Sheridan has depth of experience, working in the mining industry for more than 20 years. He holds a B.Sc. and M.Sc. from the London

School of Economics and Political Science, United Kingdom.

Claude F. Lemasson, P.Eng., MBA: President , COO and Director

, g , ,

Mr. Lemasson is a professional engineer with 20 years of experience in mining construction and operations across Canada and the United

States. From May 2006 to present, Mr. Lemasson was Goldcorp's General Manager of Projects for Canada and U.S. He was previously

employed (2000-2006) with Goldcorp Inc. as the Mine General Manager of the Red Lake mine.

Dan Noone, MBA, Geologist: VP, Exploration and Director

Mr Noone has 20 years experience in mineral exploration in Australasia and South America He was previously V P of Peru Operations for

Mr. Noone has 20 years experience in mineral exploration in Australasia and South America. He was previously V.P.of Peru Operations for

Aquiline Resources and prior to that was CEO of Absolut Resources.

Alexander Po, Geologist: Exploration Manager and Director

Mr. Po is a freelance mining and exploration geologist with strong management experience. He has managed projects in over 16 different

countries. He holds a Master of Engineering Degree (Mining Geology) from the Institute of Mining Geology, Akita University, Japan.

Robert A. Bondy, LLB: Director

Mr. Bondy recently retired from Blake, Cassels & Graydon LLP where he spent over 30 years in the Securities and Corporate Law Groups .

Richard Williams, LLB: Director

Mr. Williams is the Director of First Metals Inc. and of Waseco Resources Inc. He is also the President and founder of Blackwell Investor

39

Relations Corp., an investor relations firm specializing in establishing and strengthening relationships between public companies and the

investment community.

40.

Studies Team

Feasibility StudyManager: Mr. Andrew Croal

25 years of solid international mining experience, including senior level project development, management, cost control, supervisory and technical

experience, with such companies as Barrick Corporation, Iamgold and Cambior

Previous Chief Engineer at Rosebel Gold Mines in Suriname for Cambior and Iamgold from 2002 to 2007, and held senior engineering roles at Omai

Gold Mines in Guyana where he was a central figure in the mine design and implementation for these two successful projects

Gold Mines in Guyana, where he was a central figure in the mine design and implementation for these two successful projects

Will lead and manage the Feasibility Study work

Senior Mine Engineer: Mr. Milko Rivera

14 years of experience as a Geological and Mining Engineer with solid knowledge and experience in design, construction, cost control, and project

management in the areas of mining/processing/environmental including exploration

Experience in QA/QC construction and assay lab reporting, underground mine design, ground control, pre-feasibility and feasibility studies, and mine

d l t

development

Help support all feasibility study work

Study Coordinator: Mrs. Christine Robinson

15 years experience in general business management

Responsible for overall coordination and review of studies work

Senior Consultant: Mr. Les Heymann, P.Eng.

35 years of experience in metallurgical and process work, including gold operations internationally

Responsible for technical review of metallurgical/process work and design

Senior Consultant: Mr. Normand Champigny, M.A.Sc., P.Eng

30 years of experience in feasibility studies, geology, resource estimation and economic analysis

Responsible for technical review of geological modeling, geostatistics and resource estimation, and economic and financial modeling

p g g g, g , g

Senior Consultant: Mr. Rod Pye, BSc, ARSM

40 years of experience in mine engineering, mine operations and development of large mining projects

Responsible for technical review of mining reserve estimates, open pit and underground mine planning and associated capital and operating cost

estimates

40

41.

ConstructionTeam

Construction Manager: Mr.John Bates

30 years including industrial plant construction, technical project management, business planning & project budgeting, logistics, estimating & scheduling

Formerly the Plant Manager - Technical Projects for the Bauxite Company of Guyana Inc. – Rusal in Guyana, where he oversaw all technical aspects of

project engineering and construction for a bauxite mining operation

Will l d d th C t ti T l ki ft ll f th l th i il d t ti k l t d t th A j t

Will lead and manage the Construction Team looking after all of the early earth, civil and construction works related to the Aurora project

Earthworks Superintendent: Mr. Larry Kulhman

Seasoned earthworks specialist with 40+ years of extensive experience in road and mine construction as well as civil projects, including working in

tropical environments

Previously involved in the early development of the Omai Gold Mine in Guyana and is very familiar with Guyana

Responsible for all the earthworks related to the Aurora project

Senior Consultant: Dr. Norm T. Ng-A-Qui

30 years of experience in civil works, mining, environmental and water resources

Responsible for technical review of infrastructure, mining and water management

Construction Engineer: Mr. Eric Marquez

22 years construction engineering experience

22 years construction engineering experience

Support of the early earth, civil and construction works related to the Aurora Gold Project

Survey Manager: Mr. Richard Mulliken

20 years surveying experience

Responsible for all survey work and managing survey crews related to the Aurora Gold Project

Human Resources Manager: Mr Peter Benny

Human Resources Manager: Mr. Peter Benny

30+ years experience in industrial relations and mining projects

Worked on a multitude of projects in Guyana, Suriname and Haiti and was involved in the operation of the Omai Gold Mine and Bosai Minerals

Responsible for managing the human resources function of the Aurora Gold Project

41

42.

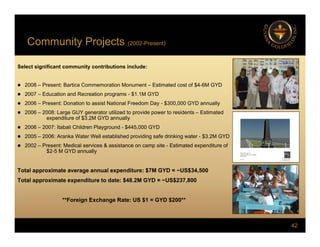

Community Projects (2002-Present)

yj ( )

Select significant community contributions include:

2008 – Present: Bartica Commemoration Monument – Estimated cost of $4-6M GYD

2007 – Education and Recreation programs - $1.1M GYD

2006 – Present: Donation to assist National Freedom Day - $300,000 GYD annually

2006 – 2008: Large GUY generator utilized to provide power to residents – Estimated

expenditure of $3.2M GYD annually

2006 – 2007: Itabali Children Playground - $445,000 GYD

2005 – 2006: Aranka Water Well established providing safe drinking water - $3.2M GYD

p g g

2002 – Present: Medical services & assistance on camp site - Estimated expenditure of

$2-5 M GYD annually

Total approximate average annual expenditure: $7M GYD = ~US$34 500

Total approximate average annual expenditure: $7M GYD = ~US$34,500

Total approximate expenditure to date: $48.2M GYD = ~US$237,800

**Foreign Exchange Rate: US $1 = GYD $200**

42

Foreign Exchange Rate: US $1 GYD $200

43.

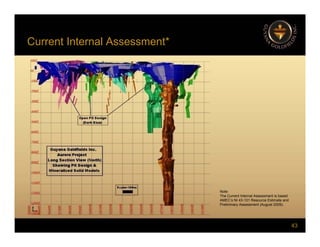

Current Internal Assessment*

Note:

TheCurrent Internal Assessment is based

AMEC’s NI 43-101 Resource Estimate and

43

AMEC s NI 43 101 Resource Estimate and

Preliminary Assessment (August 2009).

44.

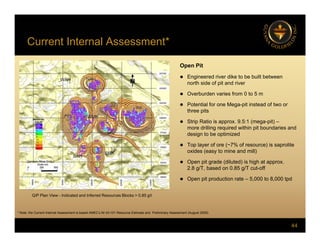

Current Internal Assessment*

OpenPit

Engineered river dike to be built between

Engineered river dike to be built between

north side of pit and river

Overburden varies from 0 to 5 m

Potential for one Mega-pit instead of two or

three pits

Strip Ratio is approx. 9.5:1 (mega-pit) –

more drilling required within pit boundaries and

design to be optimized

Top layer of ore (~7% of resource) is saprolite

oxides (easy to mine and mill)

Open pit grade (diluted) is high at approx.

2.8 g/T, based on 0.85 g/T cut-off

g , g

Open pit production rate – 5,000 to 8,000 tpd

Q/P Plan View - Indicated and Inferred Resources Blocks > 0.85 g/t

44

* Note: the Current Internal Assessment is based AMEC’s NI 43-101 Resource Estimate and Preliminary Assessment (August 2009)

45.

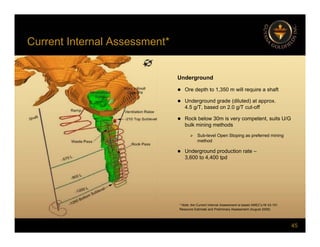

Current Internal Assessment*

Underground

Underground

Ore depth to 1,350 m will require a shaft

Underground grade (diluted) at approx.

4 5 g/T based on 2 0 g/T cut-off

4.5 g/T, based on 2.0 g/T cut off

Rock below 30m is very competent, suits U/G

bulk mining methods

Sub-level Open Stoping as preferred mining

method

Underground production rate –

3,600 to 4,400 tpd

45

* Note: the Current Internal Assessment is based AMEC’s NI 43-101

Resource Estimate and Preliminary Assessment (August 2009)

46.

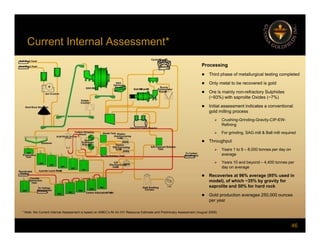

Current Internal Assessment*

Processing

Third phase of metallurgical testing completed

Only metal to be recovered is gold

Ore is mainly non-refractory Sulphides

(~93%) with saprolite Oxides (~7%)

Initial assessment indicates a conventional

gold milling process

Crushing-Grinding-Gravity-CIP-EW-

Refining

For grinding, SAG mill & Ball mill required

Throughput

Years 1 to 9 – 8,000 tonnes per day on

average

Years 10 and beyond – 4,400 tonnes per

day on average

Recoveries at 96% average (95% used in

model), of which ~35% by gravity for

saprolite and 50% for hard rock

Gold production averages 250,000 ounces

per year

46

per year

* Note: the Current Internal Assessment is based on AMEC’s NI 43-101 Resource Estimate and Preliminary Assessment (August 2009)

47.

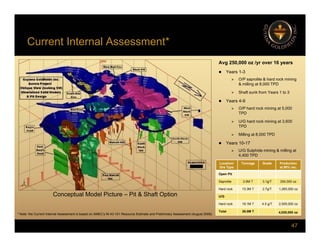

Current Internal Assessment*

Avg250,000 oz /yr over 16 years

Years 1-3

O/P saprolite & hard rock mining

& milling at 8,000 TPD

Shaft sunk from Years 1 to 3

Years 4-9

O/P hard rock mining at 5 000

O/P hard rock mining at 5,000

TPD

U/G hard rock mining at 3,600

TPD

Milling at 8,000 TPD

Years 10-17

U/G Sulphide mining & milling at

4,400 TPD

Location/

Ore Type

Tonnage Grade Production

at 95% rec.

Conceptual Model Picture – Pit & Shaft Option

Open Pit

Saprolite 2.6M T 3.1g/T 250,000 oz

Hard rock 15.3M T 2.7g/T 1,265,000 oz

U/G

47

Hard rock 18.1M T 4.5 g/T 2,505,000 oz

Total 36.0M T

* Note: the Current Internal Assessment is based on AMEC’s NI 43-101 Resource Estimate and Preliminary Assessment (August 2009)

4,020,000 oz

48.

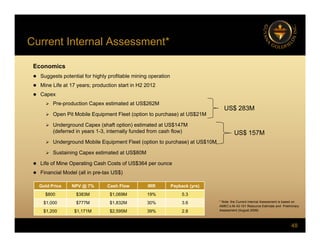

Current Internal Assessment*

Economics

Suggests potential for highly profitable mining operation

Suggests potential for highly profitable mining operation

Mine Life at 17 years; production start in H2 2012

Capex

Pre-production Capex estimated at US$262M

US$ 283M

Open Pit Mobile Equipment Fleet (option to purchase) at US$21M

Underground Capex (shaft option) estimated at US$147M

(deferred in years 1-3, internally funded from cash flow)

US$ 283M

US$ 157M

Underground Mobile Equipment Fleet (option to purchase) at US$10M

Sustaining Capex estimated at US$80M

Life of Mine Operating Cash Costs of US$364 per ounce

$

Financial Model (all in pre-tax US$)

Gold Price NPV @ 7% Cash Flow IRR Payback (yrs)

$800 $383M $1,069M 19% 5.3

$1 000 $777M $1 832M 30% 3 6 * Note: the Current Internal Assessment is based on

48

$1,000 $777M $1,832M 30% 3.6

$1,200 $1,171M $2,595M 39% 2.8

* Note: the Current Internal Assessment is based on

AMEC’s NI 43-101 Resource Estimate and Preliminary

Assessment (August 2009)

49.

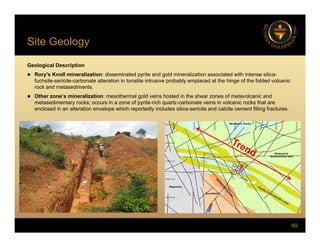

Site Geology

gy

Geological Description

Rory's Knoll mineralization: disseminated pyrite and gold mineralization associated with intense silica-

y py g

fuchsite-sericite-carbonate alteration in tonalite intrusive probably emplaced at the hinge of the folded volcanic

rock and metasediments.

Other zone’s mineralization: mesothermal gold veins hosted in the shear zones of metavolcanic and

metasedimentary rocks; occurs in a zone of pyrite-rich quartz-carbonate veins in volcanic rocks that are

enclosed in an alteration envelope which reportedly includes silica sericite and calcite cement filling fractures

enclosed in an alteration envelope which reportedly includes silica-sericite and calcite cement filling fractures.

49