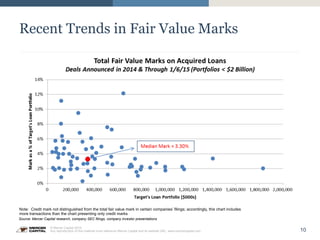

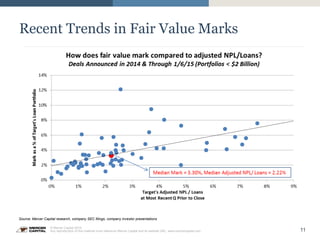

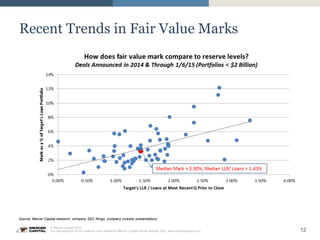

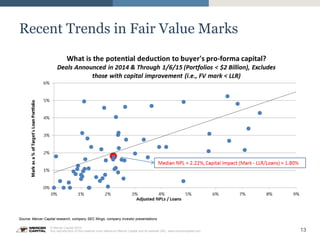

Download as PDF, PPTX

![32

© Mercer Capital 2015.

Any reproduction of this material must reference Mercer Capital and its website URL: www.mercercapital.com

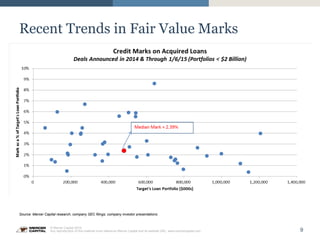

Future Evolution

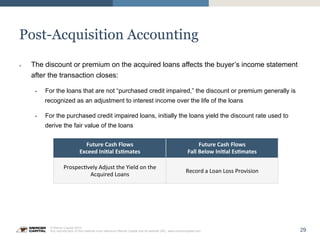

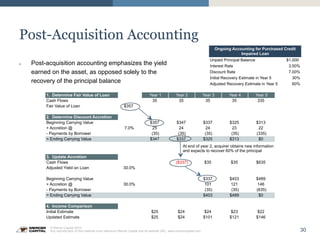

» The Financial Accounting Standards Board has released an exposure draft regarding

credit losses on financial instruments

» Proposed standard supersedes ASC Topic 310-30 (purchased credit impaired loans)

» Acquirer essentially records a reserve against the acquired loans

» Relevant guidance states as follows:

. . . a related allowance for credit losses should be recognized for expected credit losses at the

date of acquisition on the basis of the current amount of expected credit losses considering

contractual cash flows not expected to be collected (that is, the expected credit losses

embedded in the purchase price at acquisition). The expected credit losses embedded in the

purchase price for purchased credit-impaired financial assets should never be accreted into

interest income. [Exposure Draft, p. 111]](https://image.slidesharecdn.com/loanmarksaoba2015akgjkd-150128095741-conversion-gate02/85/Mercer-Capital-Getting-It-Right-Loan-Valuation-and-Credit-Marks-in-Today-s-M-A-Market-January-2015-32-320.jpg)

The document discusses loan valuation and credit marks in the M&A market, emphasizing the importance of assessing credit risks and the fair value of acquired loan portfolios. It outlines practical guidance for evaluating loans, accounting for acquired assets, and emerging trends in fair value marks. Furthermore, it highlights upcoming changes in financial reporting standards related to credit losses on financial instruments.