Downloaded 103 times

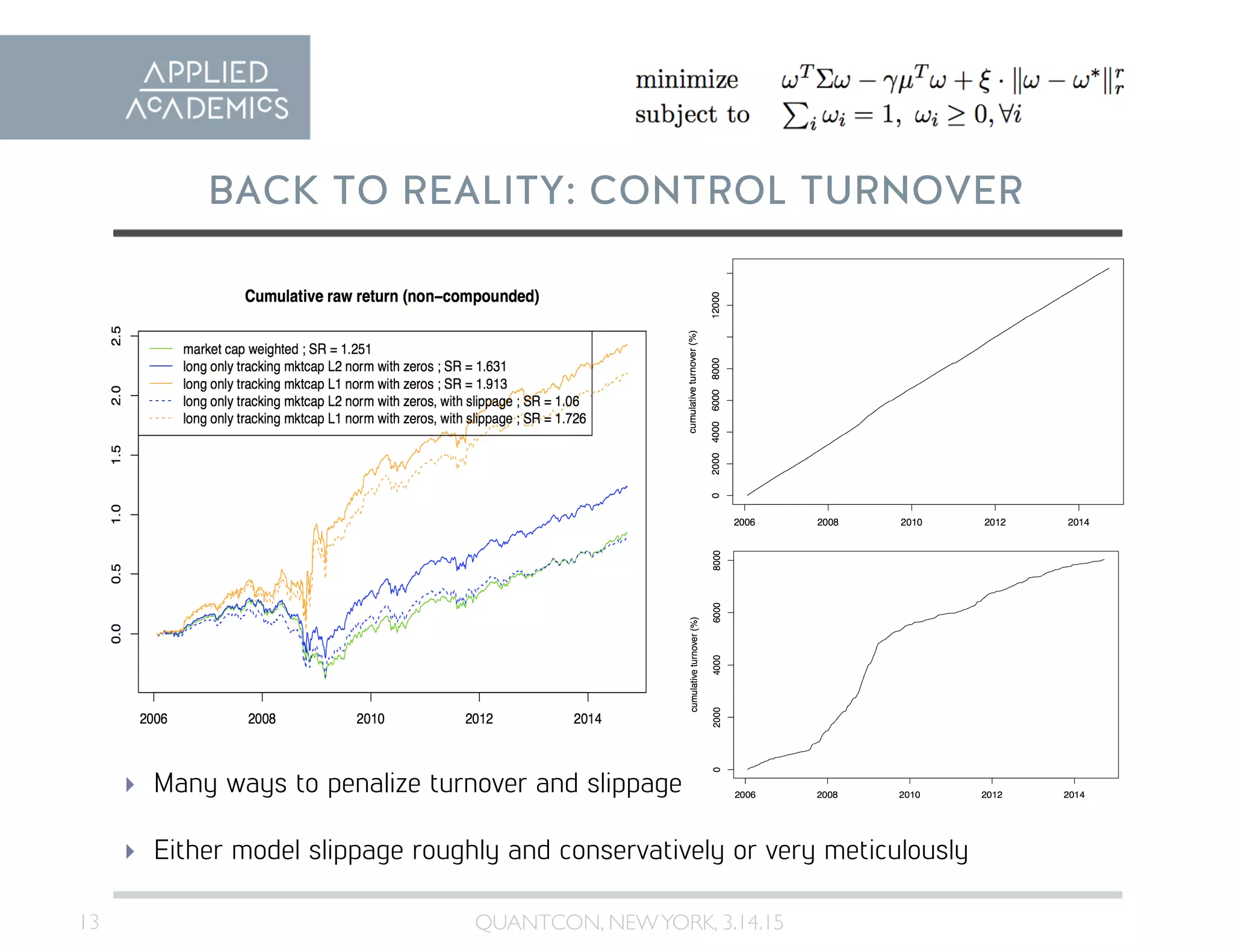

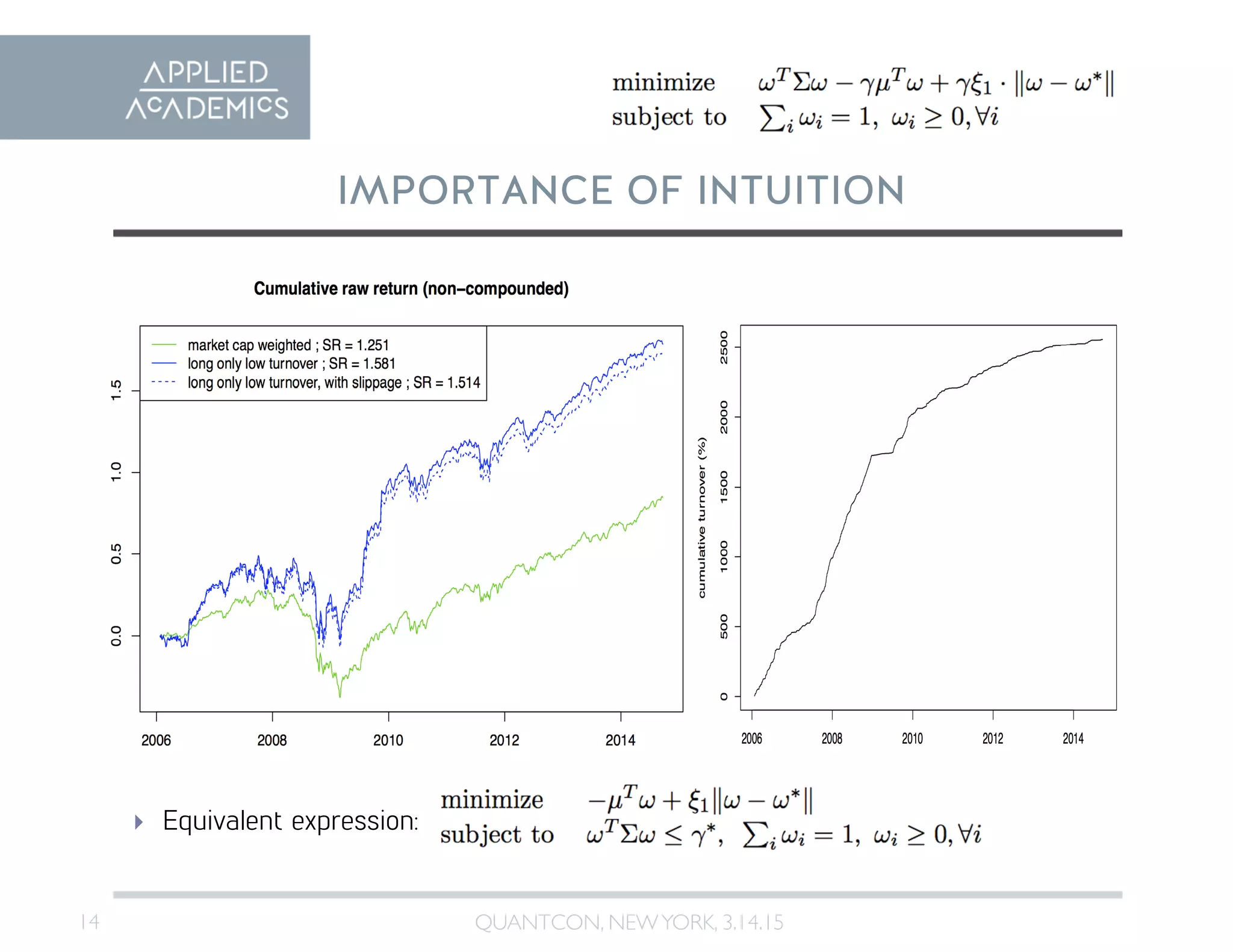

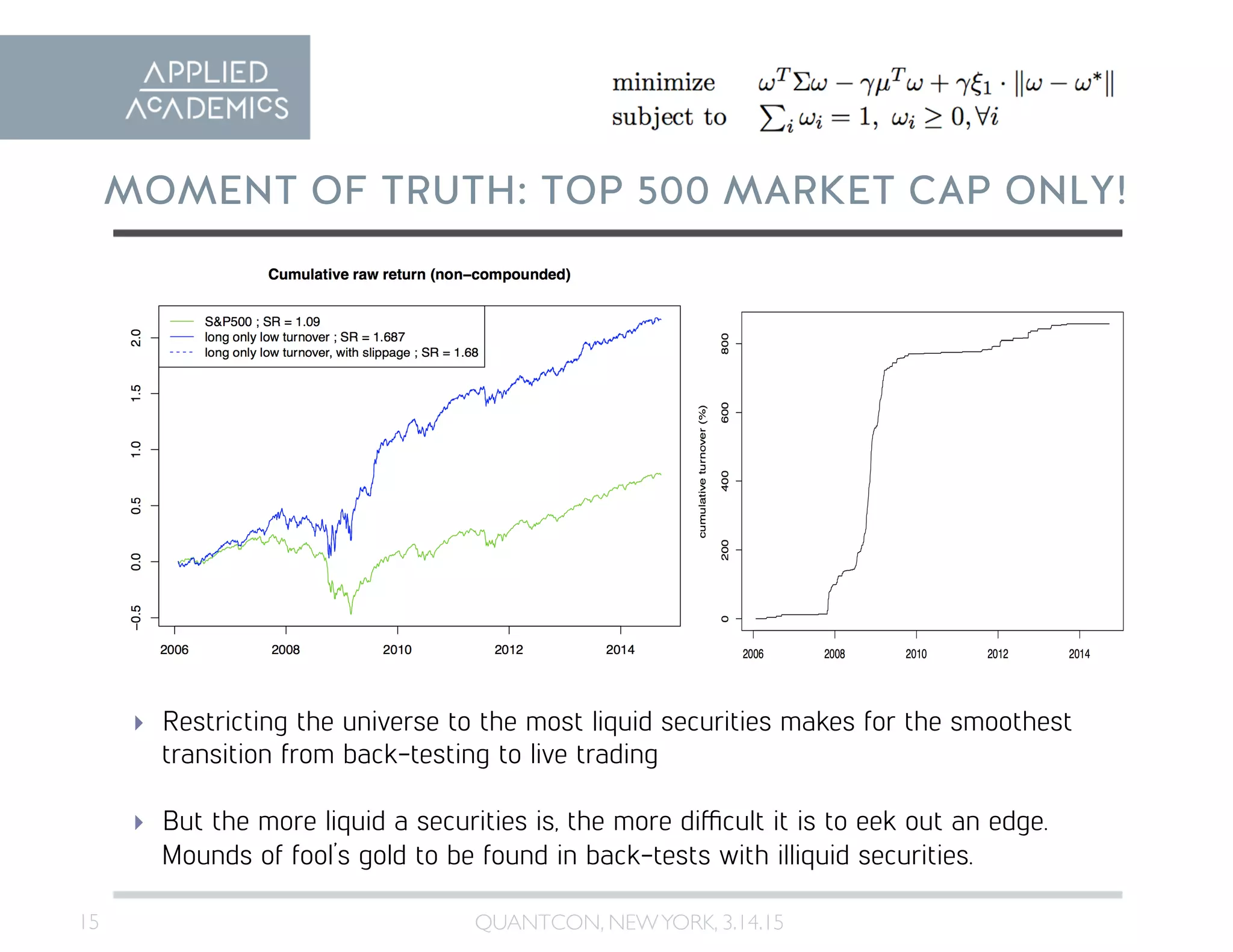

The document discusses the process of developing and executing trading strategies, highlighting the importance of refining ideas and investing time wisely. It covers techniques such as back-testing, parameter estimation, and signal interpretation, emphasizing the need for a clear understanding of strategy mechanics. Finally, it touches on practical considerations like liquidity, transaction costs, and the transition from back-testing to live trading.

![[Data Meetup] Data Science in Finance - Building a Quant ML pipeline](https://cdn.slidesharecdn.com/ss_thumbnails/buildingaquantmlpipeline-191009091209-thumbnail.jpg?width=640&height=640&fit=bounds)