Downloaded 21 times

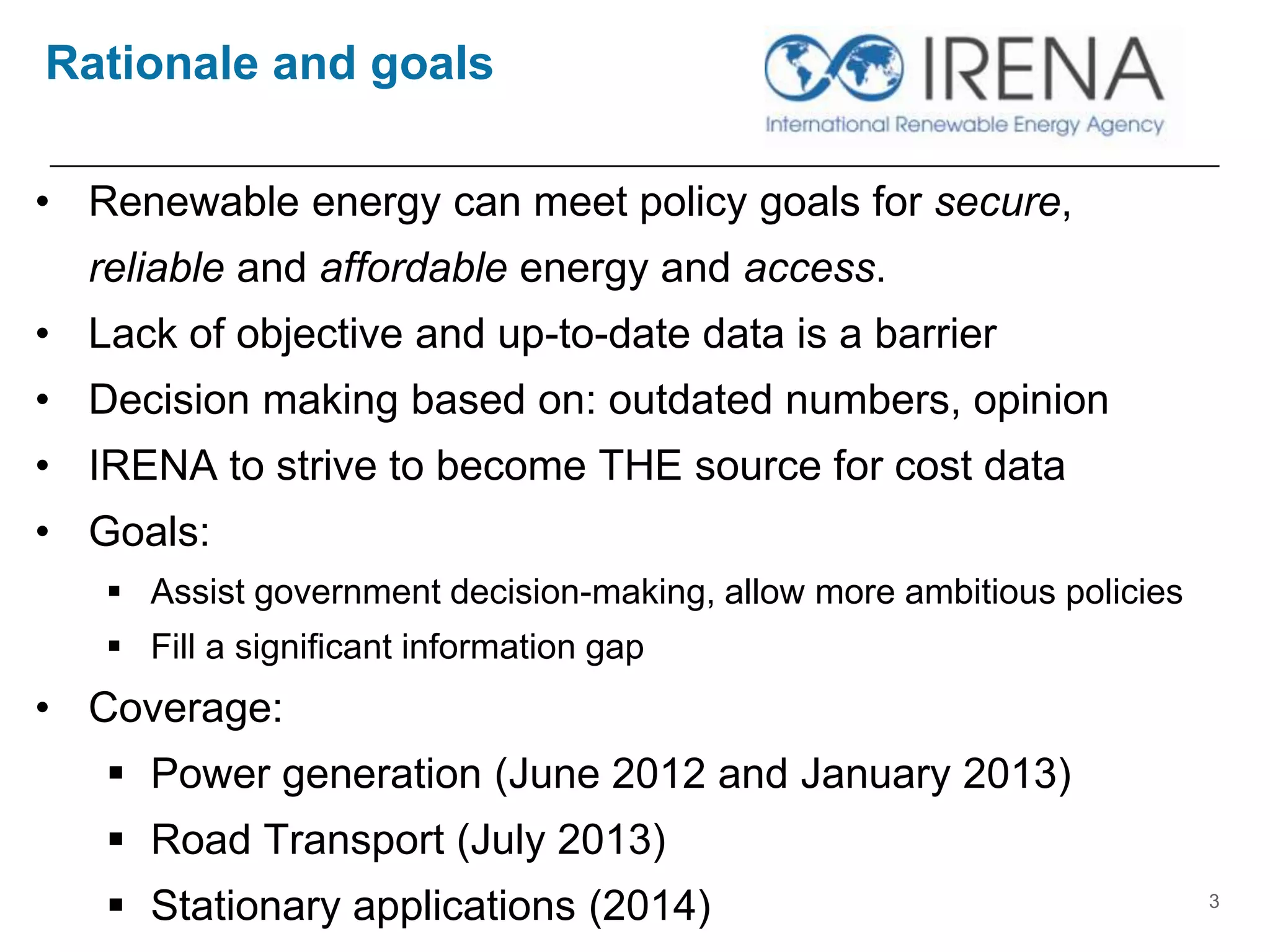

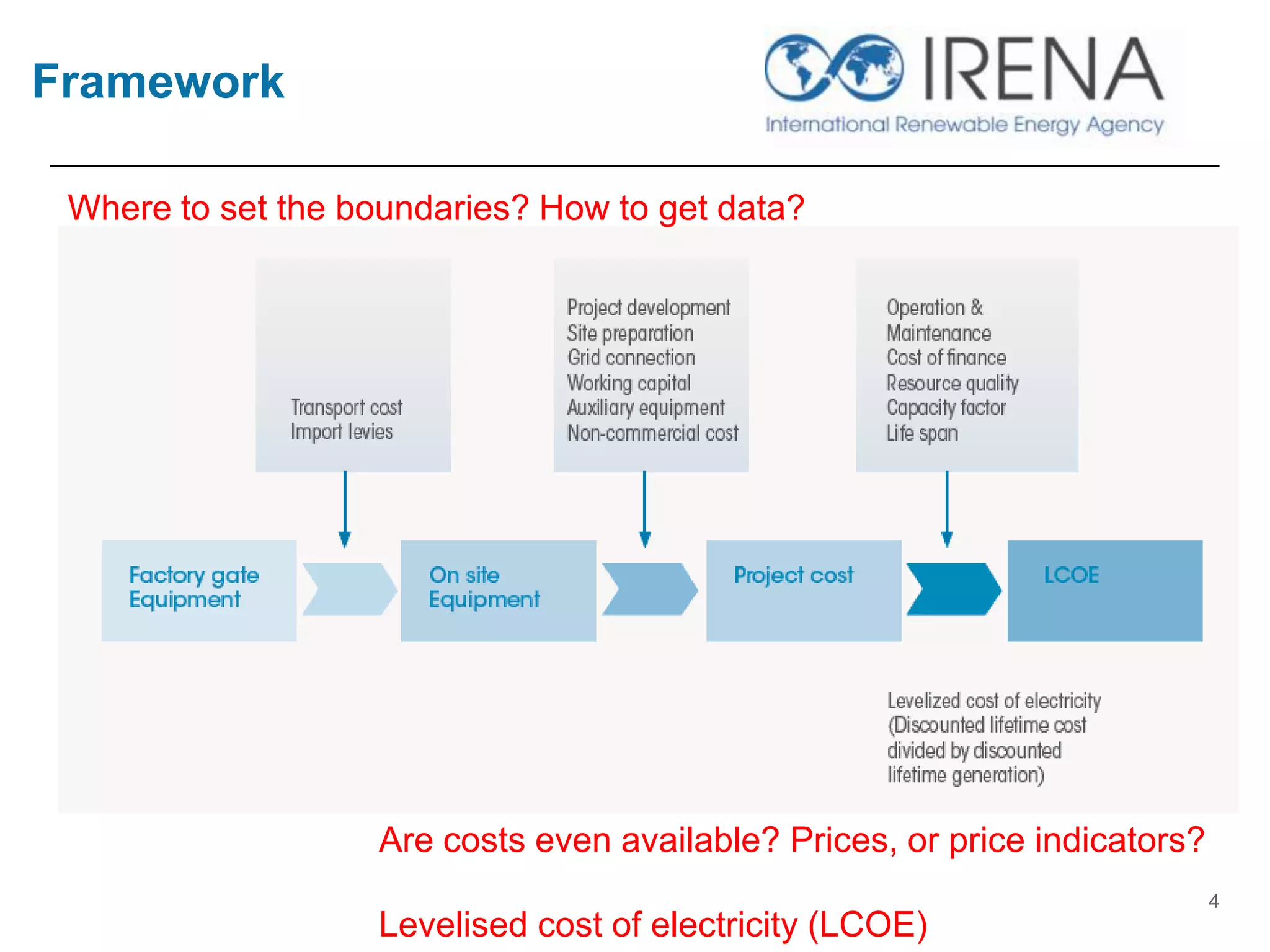

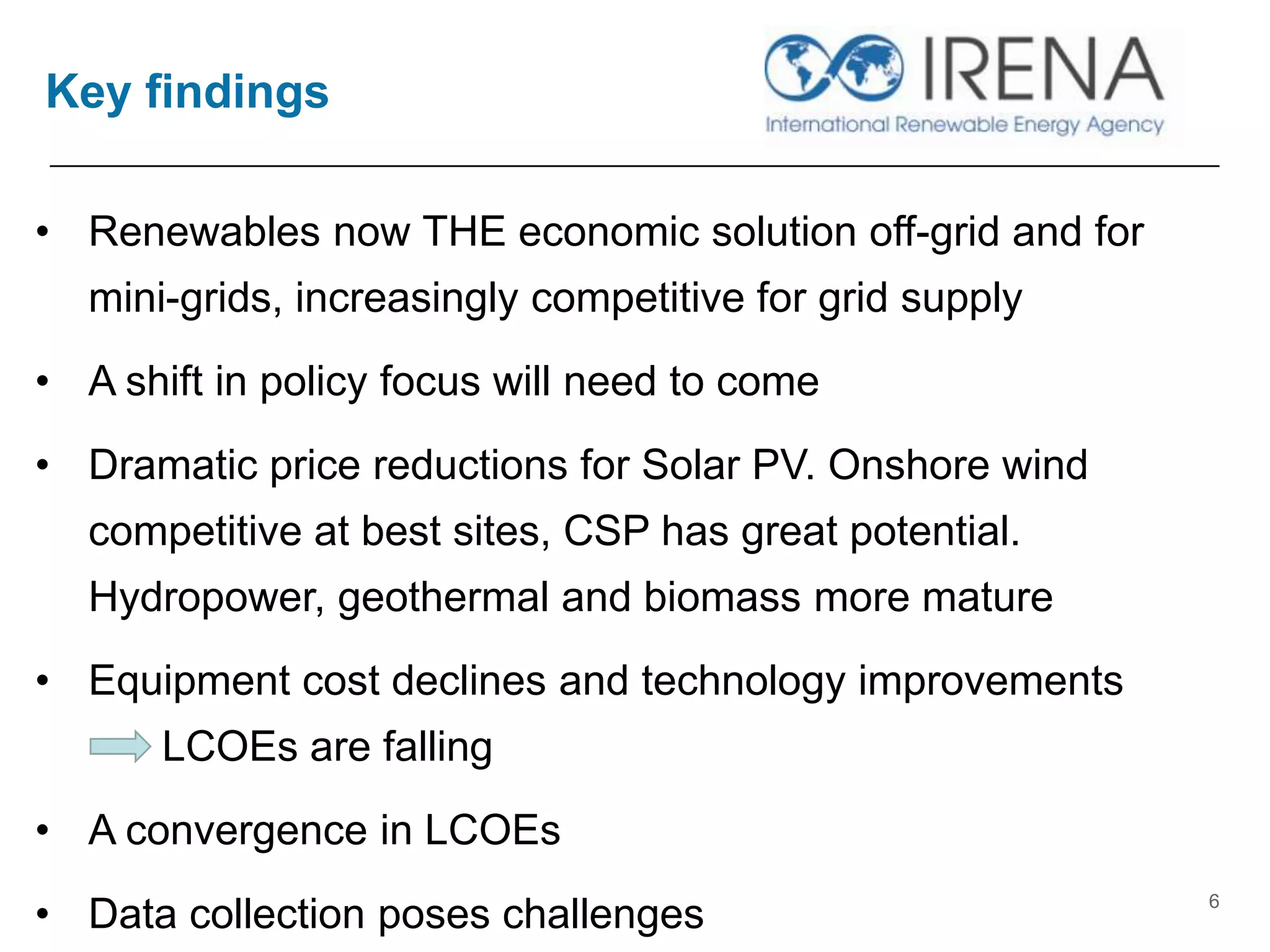

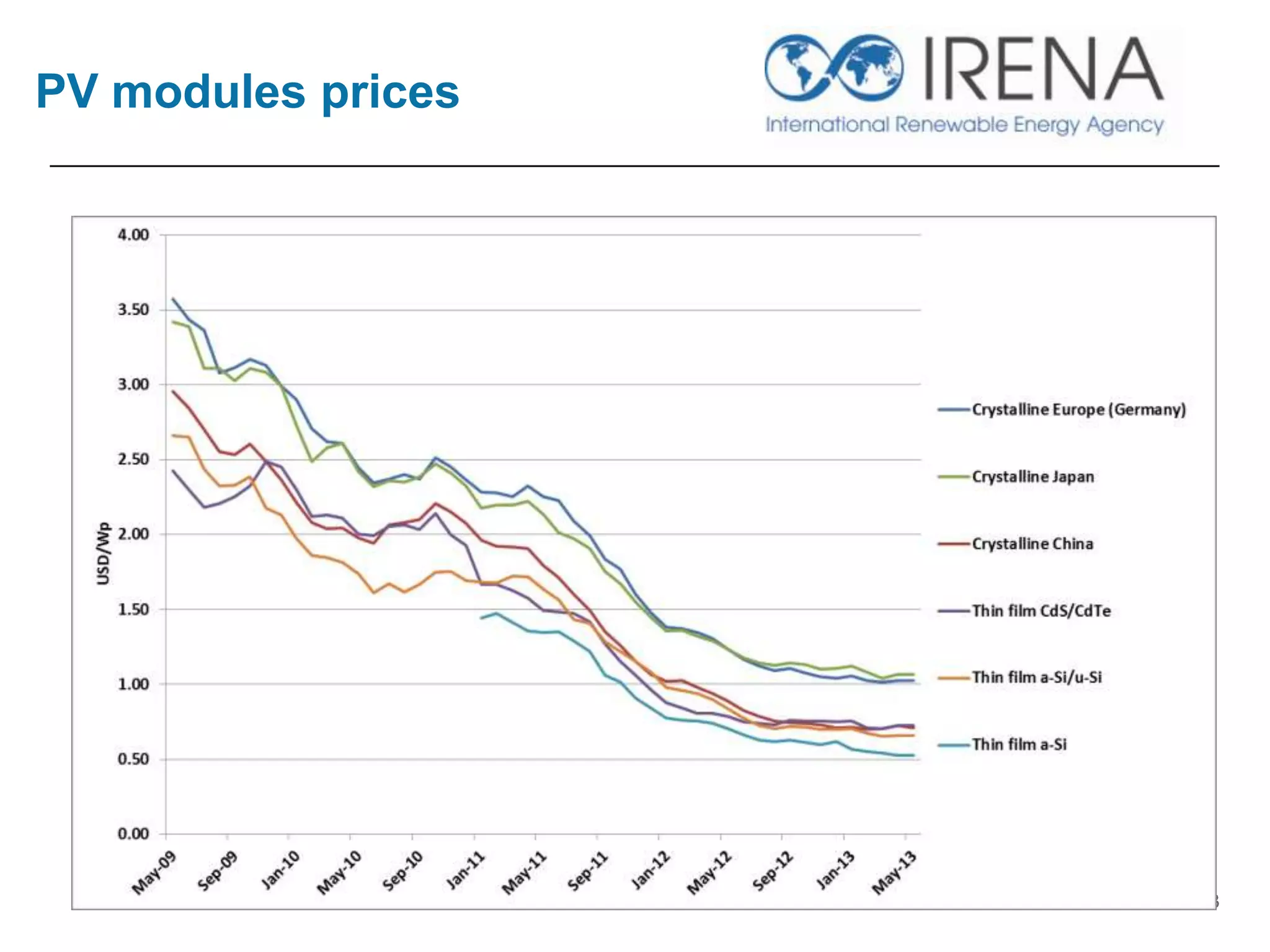

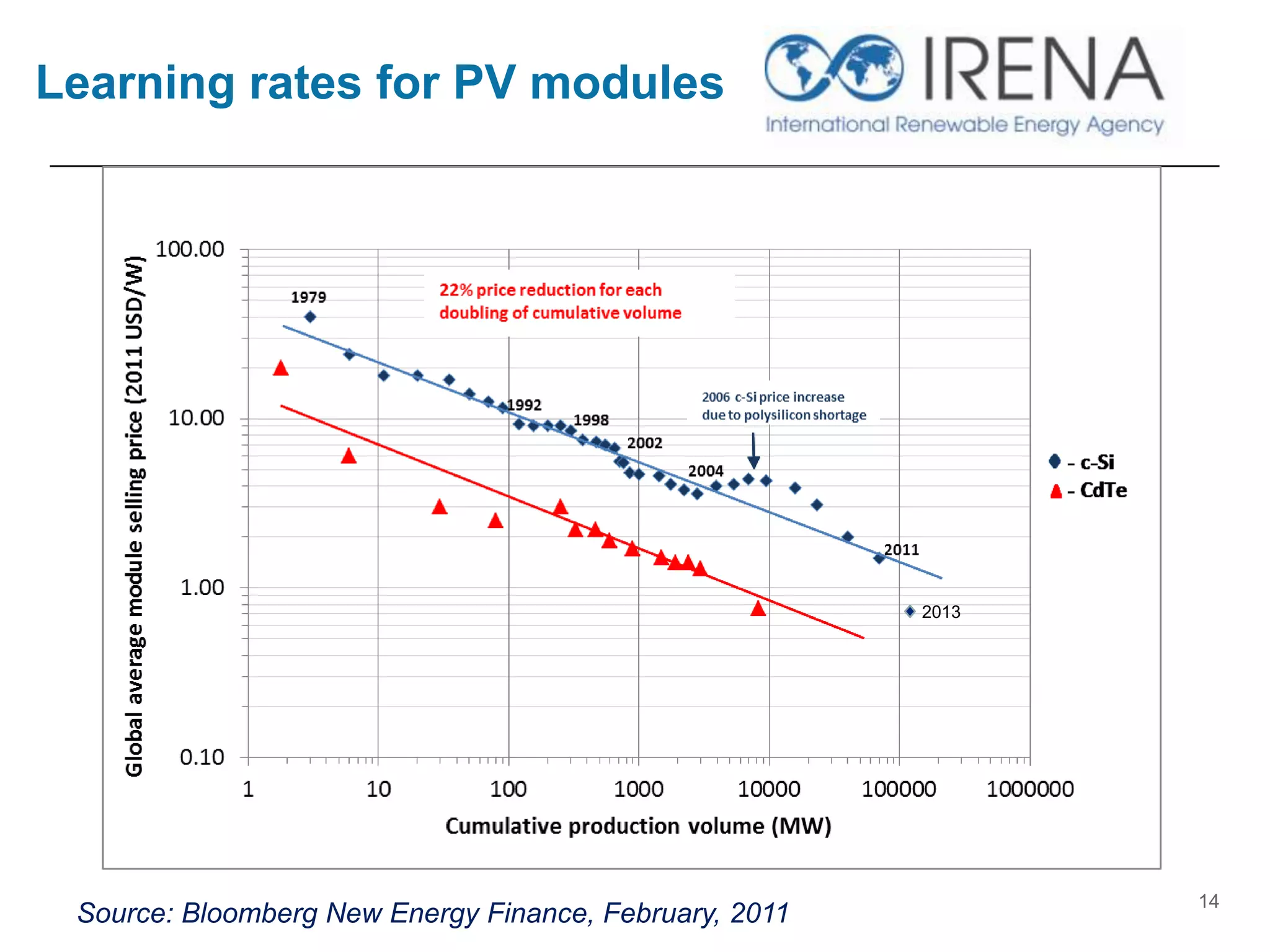

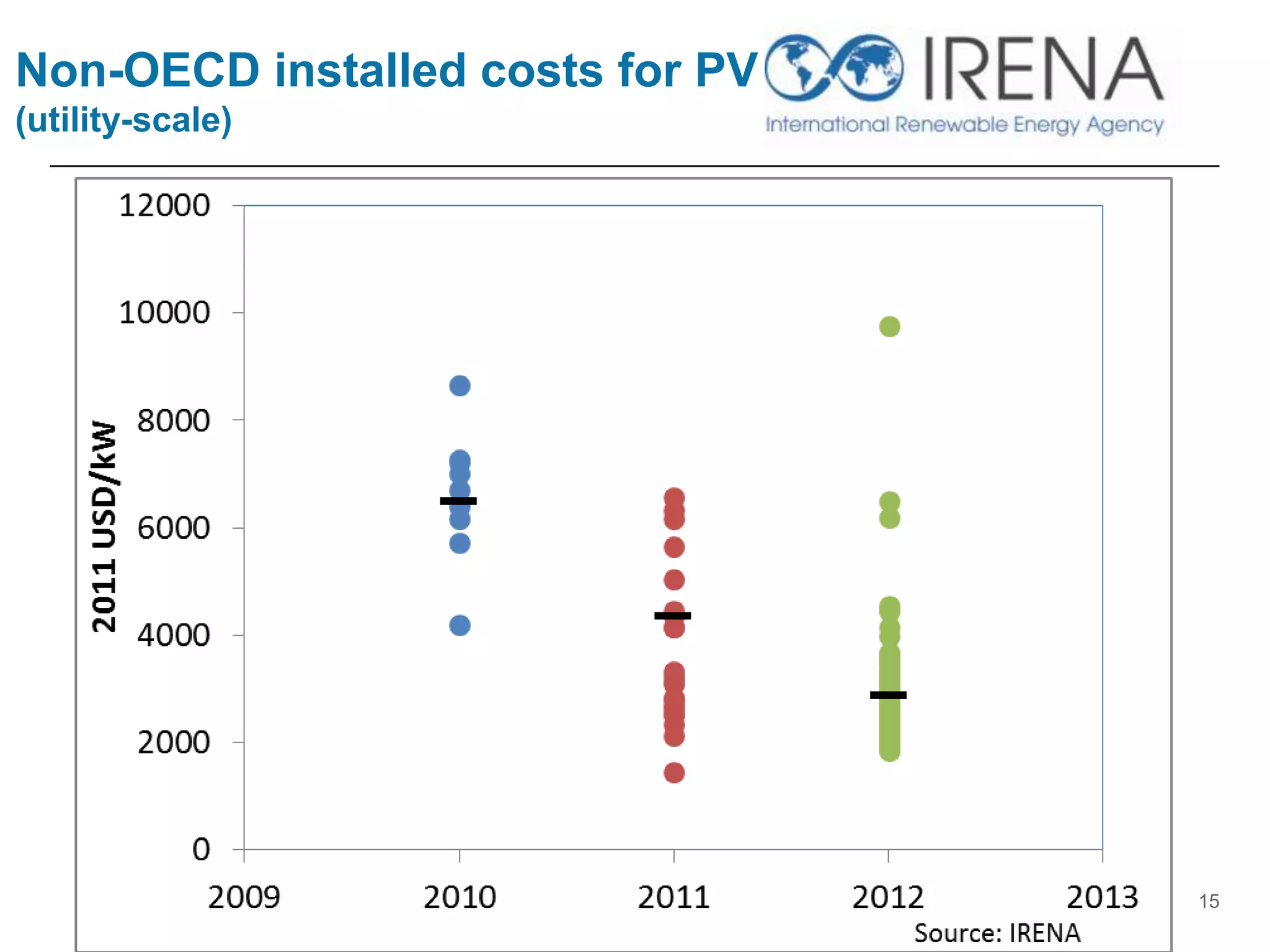

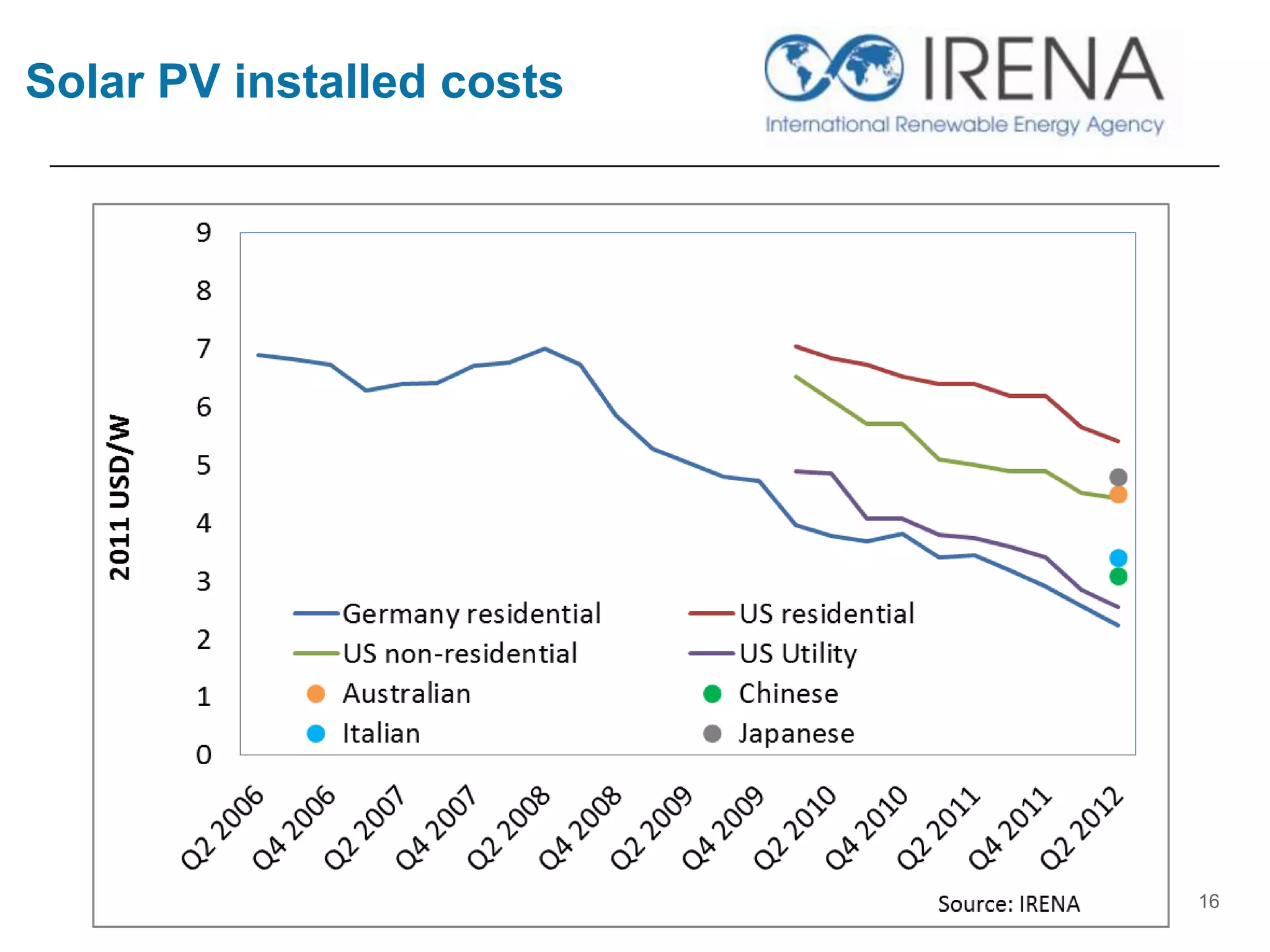

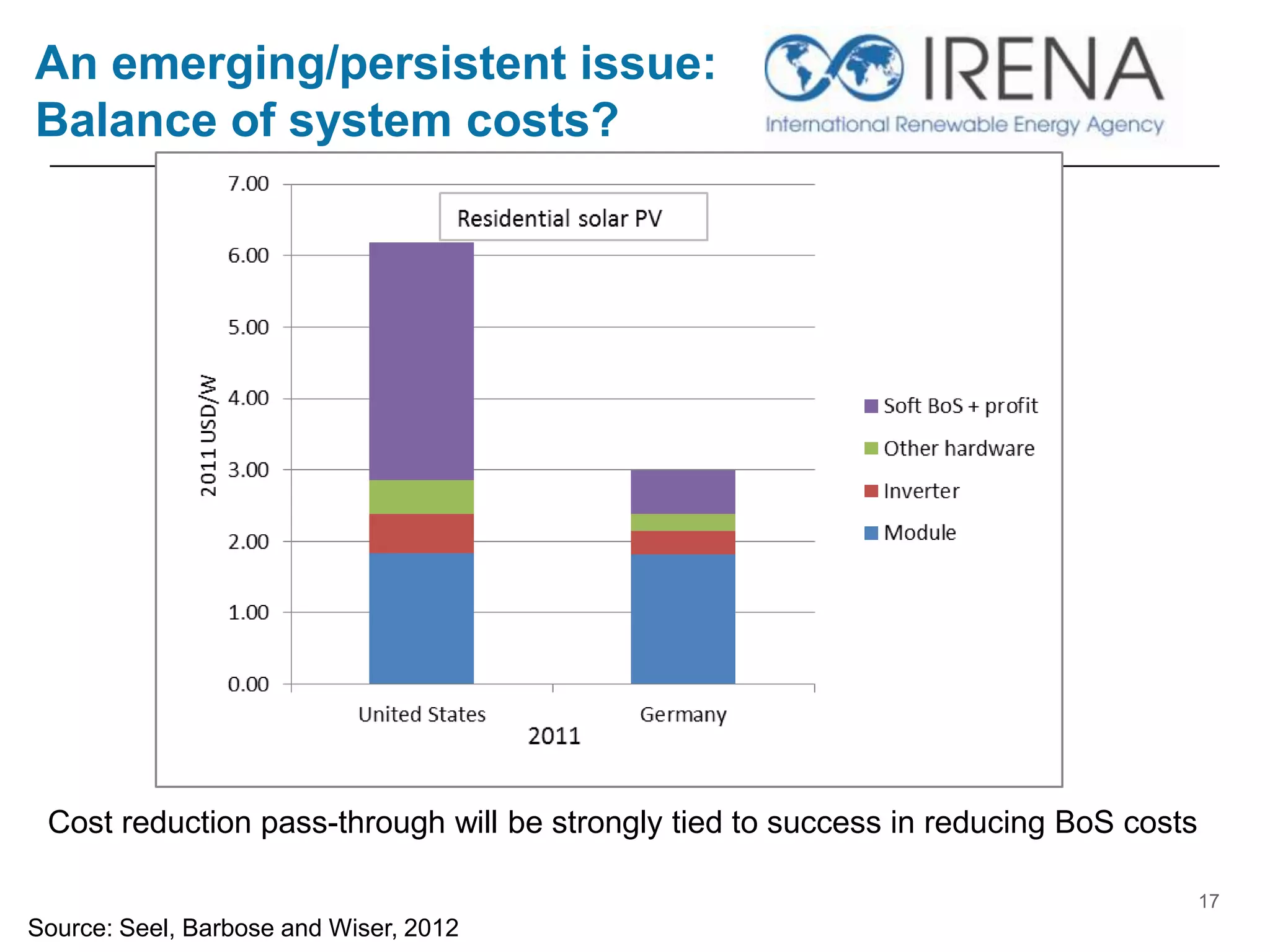

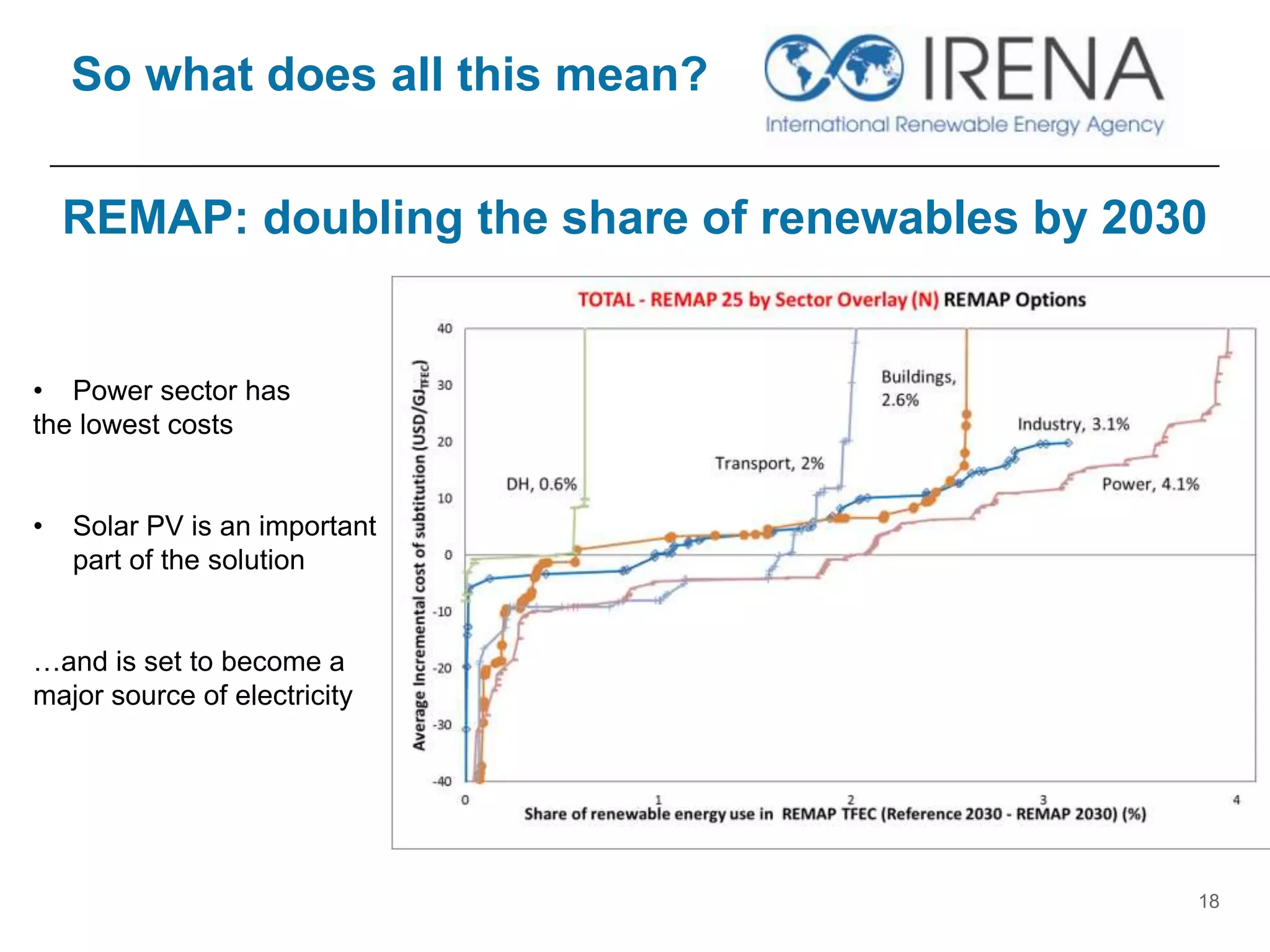

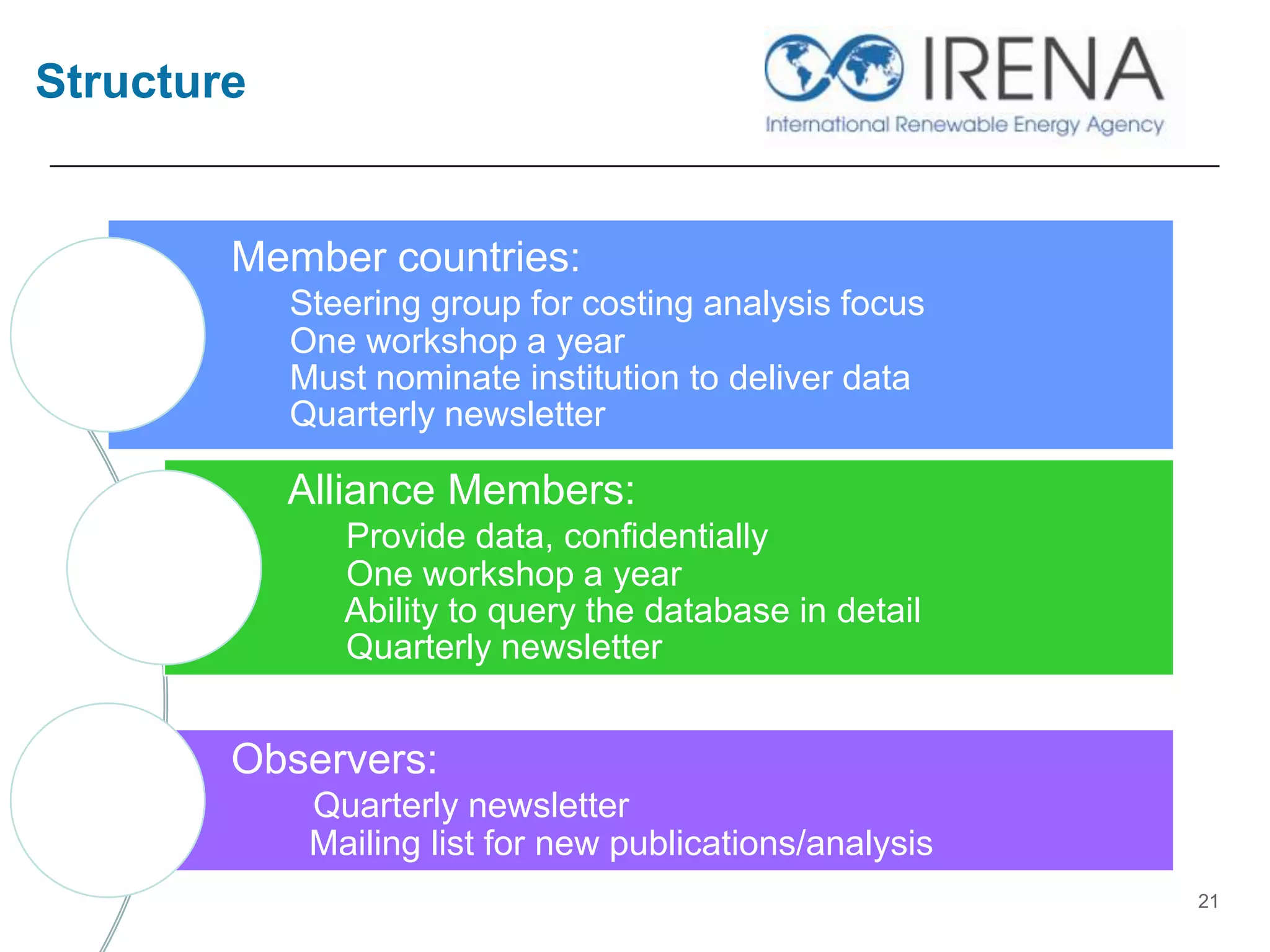

The document discusses IRENA's analysis on power generation costs, emphasizing the increasing competitiveness of renewable energy sources like solar PV and wind. It highlights the necessity for updated data to guide governmental decision-making and ambitious policies, particularly in relation to cost reductions and technological advancements. The document outlines future plans to enhance data sharing through the IRENA Renewable Costing Alliance, aiming to support the growth of renewables by 2030.

![Vibe Coding vs. Spec-Driven Development [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/vibecodingvsspecdrivendevelopment-251209105622-43f455e7-thumbnail.jpg?width=640&height=640&fit=bounds)