Downloaded 125 times

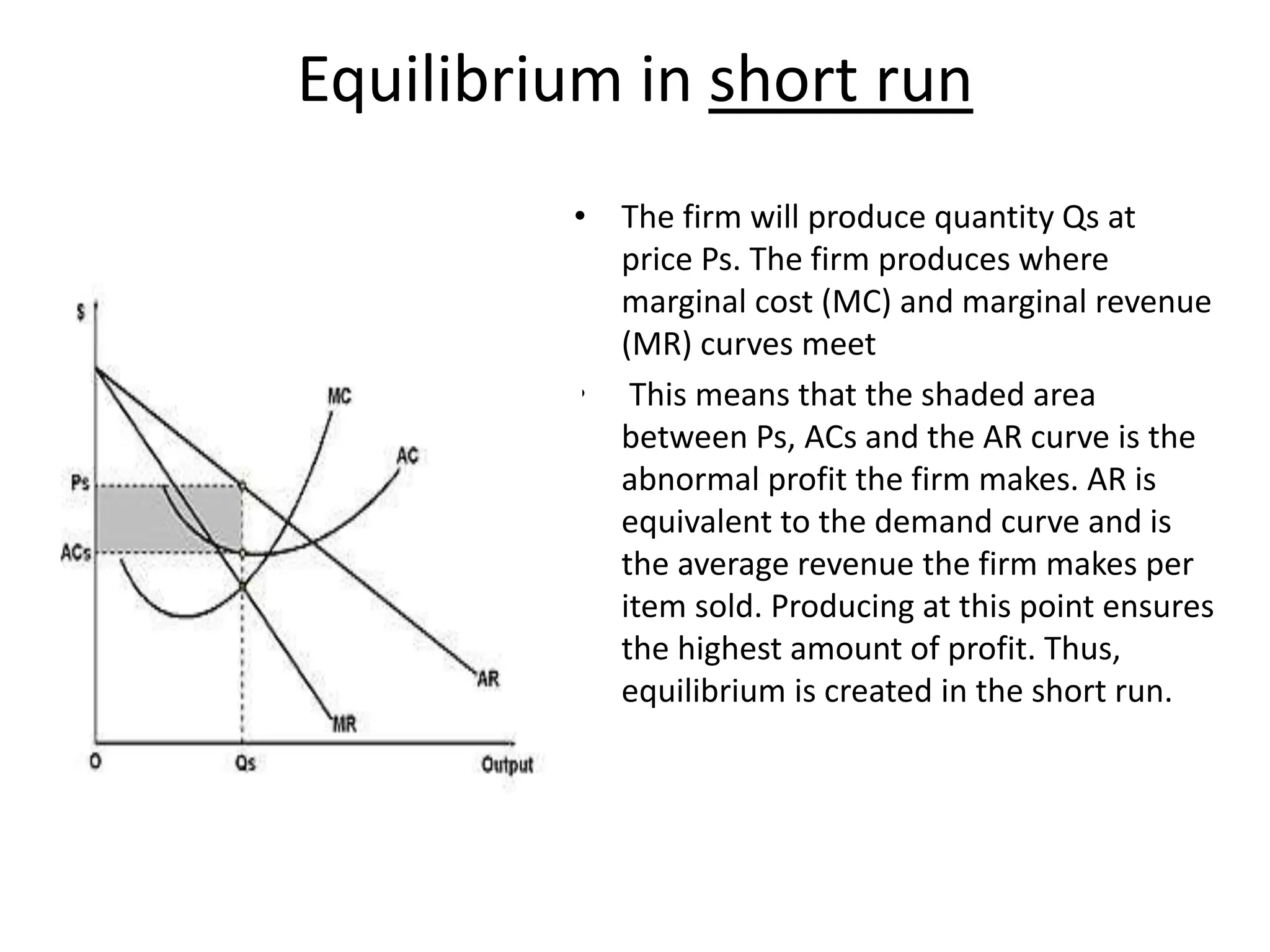

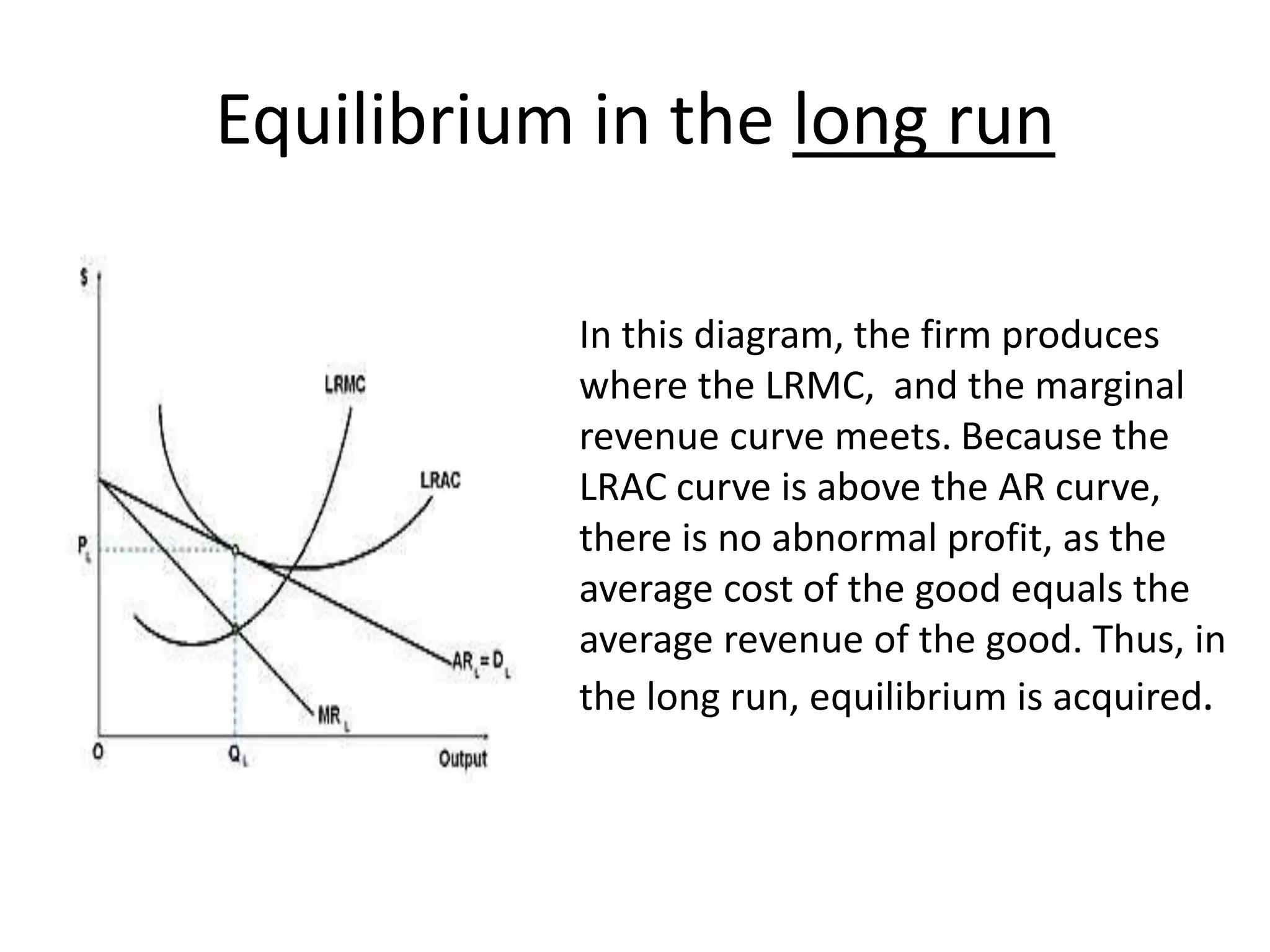

In the short run, a monopolistically competitive firm will produce at the quantity where marginal cost equals marginal revenue to maximize profits. This occurs at a price above average cost, resulting in abnormal profits. In the long run, entry of new firms shifts individual demand curves down and costs curves up, eliminating abnormal profits so firms only earn normal profits where price equals average cost, establishing equilibrium.