The document summarizes the state of Cyprus's economy six months after its financial crisis and bailout. It finds that while some indicators like the budget deficit and GDP decline were not as bad as expected, the economy is still struggling with high unemployment, capital flight, and debt. There are signs of improvement in exports but the long-term outlook remains uncertain as the full effects of the crisis have yet to be seen. The document promotes the expertise of Sapienta Economics and Strata Insight in analyzing Cyprus's economy and energy policy.

The document proposes using wikis for student lab report writing to allow for collaborative and asynchronous work, reducing paperwork for teachers while still allowing them to track individual contributions through the wiki's history log. Some benefits are fewer reports to grade, timely feedback during the writing process, and developing digital literacy and collaboration skills useful for their academic and professional careers.

The document contains the schedule for an real estate agent for the month of November. It includes times for open houses, training sessions, meetings with clients and other agents, and administrative tasks. Recurring events include open houses on Wednesdays and Saturdays from 10am-1pm, and feedback calls on Wednesdays from 1-3pm. It also lists upcoming training seminars from the company Trend and notes when direct mailings and emails should be sent to clients.

Cw industrial real estate forecast 2013 2016Katie Madanat

California.

The document provides an industrial real estate market forecast for the United States from 2013 to 2016. It discusses the economic outlook, noting uncertainty in the near term but expected stronger growth starting in 2014. It reviews improving industrial market fundamentals with declining vacancy rates. Demand is expected to remain strong for warehouse/distribution space, though new supply may constrain some markets. Rents are projected to grow steadily through 2016, led by coastal markets with constraints. Manufactured exports and reshoring initiatives are positives for manufacturing. Secondary industrial markets are gaining more distribution business through improved infrastructure and supply chain efficiencies.

This document provides industrial real estate market statistics for the United States in Q3 2012, including:

- Overall vacancy rates, with the lowest in SWFL (Naples, FL) at 3.6% and the highest in Fredericksburg, VA at 18.1%.

- Direct net asking rental rates, with the highest in Silicon Valley, CA at $12.92/psf/yr NNN and the lowest in Memphis, TN at $2.54/psf/yr NNN.

- Leasing activity year-to-date, led by Greater Los Angeles at 28.32 million sqft and Chicago, IL at 25.31 million sqft.

- Construction completions

The document summarizes the state of Cyprus's economy six months after its financial crisis and bailout. It finds that while some indicators like the budget deficit and GDP decline were not as bad as expected, the economy is still struggling with high unemployment, capital flight, and debt. There are signs of improvement in exports but the long-term outlook remains uncertain as the full effects of the crisis have yet to be seen. The document promotes the expertise of Sapienta Economics and Strata Insight in analyzing Cyprus's economy and energy policy.

The document proposes using wikis for student lab report writing to allow for collaborative and asynchronous work, reducing paperwork for teachers while still allowing them to track individual contributions through the wiki's history log. Some benefits are fewer reports to grade, timely feedback during the writing process, and developing digital literacy and collaboration skills useful for their academic and professional careers.

The document contains the schedule for an real estate agent for the month of November. It includes times for open houses, training sessions, meetings with clients and other agents, and administrative tasks. Recurring events include open houses on Wednesdays and Saturdays from 10am-1pm, and feedback calls on Wednesdays from 1-3pm. It also lists upcoming training seminars from the company Trend and notes when direct mailings and emails should be sent to clients.

Cw industrial real estate forecast 2013 2016Katie Madanat

California.

The document provides an industrial real estate market forecast for the United States from 2013 to 2016. It discusses the economic outlook, noting uncertainty in the near term but expected stronger growth starting in 2014. It reviews improving industrial market fundamentals with declining vacancy rates. Demand is expected to remain strong for warehouse/distribution space, though new supply may constrain some markets. Rents are projected to grow steadily through 2016, led by coastal markets with constraints. Manufactured exports and reshoring initiatives are positives for manufacturing. Secondary industrial markets are gaining more distribution business through improved infrastructure and supply chain efficiencies.

This document provides industrial real estate market statistics for the United States in Q3 2012, including:

- Overall vacancy rates, with the lowest in SWFL (Naples, FL) at 3.6% and the highest in Fredericksburg, VA at 18.1%.

- Direct net asking rental rates, with the highest in Silicon Valley, CA at $12.92/psf/yr NNN and the lowest in Memphis, TN at $2.54/psf/yr NNN.

- Leasing activity year-to-date, led by Greater Los Angeles at 28.32 million sqft and Chicago, IL at 25.31 million sqft.

- Construction completions

Las Vegas Sun - Startups finding success with boost from Vegas Tech FundKatie Madanat

The Vegas Tech Fund has helped several tech startups find success and put down roots in Las Vegas. One startup the fund invested in was Romotive, which makes small remote-controlled robots called Romos. The $500,000 investment from Vegas Tech Fund helped Romotive grow from a few employees to 18, and partnering with the fund's leaders helped the company plan for growth. Now several other startups have received money from the Vegas Tech Fund and have also significantly grown their employee numbers and revenue thanks to the fund's support and connections to the Las Vegas community. The fund aims to increase tech innovation and the creative workforce in downtown Las Vegas.

A monthly report produced by Stephen P. A. Brown, PhD, of the Center for Business & Economic Research at the University of Nevada, Las Vegas discusses gasoline prices in Nevada and on the West Coast. Gasoline prices increased in 2012 due to tensions with Iran, low U.S. gasoline inventories, and refinery outages in California and Washington. Most indicators now suggest that gasoline prices have peaked and should begin to fall, with prices in Nevada expected to decline to around $3.50/gallon by December. However, prices on the West Coast may fall more slowly due to still low regional gasoline inventories.

This monthly report from the Center for Business & Economic Research at UNLV discusses the state of the US economy in August 2012. It finds that:

1) US GDP growth slowed to 1.3% in Q2 2012, below potential GDP.

2) Personal consumption spending was the largest contributor to GDP growth in the first half of 2012, outpacing overall GDP growth.

3) Business investment spending grew modestly while residential investment strengthened, suggesting moderate overall investment growth.

4) Government spending declines contributed to slowing GDP, though the impacts varied between federal and state/local levels.

Industrial Fact of the Week - US Leasing Activity over 500,000SFKatie Madanat

Leasing activity of large commercial spaces over 500,000 square feet in the U.S. peaked in 2007 at over 20 million square feet but declined during the market slowdown, reaching a low of 11.1 million square feet in 2010. The market began recovering in mid-2010 and leasing activity has increased since 2011, with the largest single lease being Home Depot's 1.6 million square foot build-to-suit deal in Chicago in 2011. So far this year, leasing activity for spaces over 500,000 square feet totals 15.5 million square feet across 20 deals predominantly in the manufacturing, retail, transportation, and wholesale industries

Cushman & Wakefield - North American Industrial Market Beat - Mid-Year 2012Katie Madanat

1) The document provides an economic overview of North America and discusses uncertainty in the US economy from issues in Europe and China.

2) It notes declines in US manufacturing in June 2012 and orders but that manufacturing activity revived in Canada in the first half of 2012.

3) Demand remains expansionary across most Canadian industrial real estate markets but challenging global conditions are translating to more caution in occupancy decisions, with stronger momentum in western Canadian markets like Alberta.

This document summarizes a monthly economic report on the fiscal cliff and its potential impact on the US economy. It finds that allowing all current tax increases and spending cuts to take effect could plunge the US back into recession due to the abrupt change in fiscal policy. However, failing to address the large budget deficit also poses long-term risks to economic growth. The report recommends a gradualist approach that gradually reduces the deficit to a sustainable level over several years to minimize near-term economic risks.

Cushman & Wakefield - Industrial Fact of the Week - July 10 12Katie Madanat

U.S. industrial warehouse demand is driven by housing activity. When housing starts and sales peaked in 2005, warehouse absorption also hit its peak. However, as the housing market declined from 2006 to 2009 due to the recession, warehouse absorption fell for 12 consecutive quarters. When the effects of the recession were felt in 2008, warehouse users reduced their space by 66.5 million square feet. By early 2009, warehouse absorption reached its lowest point during the recession. As the economy recovered in 2010, new housing starts increased which lifted housing sales and subsequently drove increased demand for warehouse space from retailers and suppliers. Over the past eight quarters, warehouse absorption has totaled 119.5 million square feet.

Las Vegas Nevada Fact Sheet Jan-Mar 2012Katie Madanat

The document provides an economic overview of the Las Vegas Valley region for January through March 2012. Some key points:

- Employment declined slightly in Las Vegas but grew in Clark County overall. Leisure and hospitality remained the largest sector.

- Tourism numbers increased year-over-year with over 9.7 million visitors in the first quarter. Gaming revenue was up 4.4% overall.

- The housing market showed signs of recovery with new home construction up and prices stabilizing. Apartment rents increased slightly but vacancies remained high.

- Commercial real estate markets saw some absorption across major sectors though vacancies persisted, especially in office space. New development activity was limited overall.

Cushman & Wakefield - Industrial Fact of the Week - May, 15 2012Katie Madanat

Retail sales continued to climb in the first quarter of 2012, reaching $1.2 trillion. Several retail sectors experienced double-digit annual growth. With increased demand from retailers and third-party logistics providers, industrial space leasing reached its highest level since 2007. The overall industrial vacancy rate declined to 9.0%, its lowest point since 2008, as industrial users absorbed over 99 million square feet of space since 2011. With demand outpacing supply, new speculative development of industrial space is increasing, with approximately 25 million square feet under construction to be completed in 2012.

This monthly report discusses the potential economic impact of higher oil prices in early 2012. It finds that while higher gasoline prices are noticeable, current oil price increases are unlikely to trigger a recession for three main reasons: 1) oil prices have not risen enough compared to the past three years to be recession-inducing, 2) natural gas prices have diverged from oil prices and lowered overall energy costs, and 3) the US economy has become less dependent on energy over time. The report also provides an overview of recent economic conditions in the US and Nevada.

North America Industrial Indicators - In 7 MinutesKatie Madanat

This document provides a 3-minute summary of industrial indicators for North America in April 2012. Key points include: container carriers leaving the Port of Seattle for Tacoma, which should reverse Tacoma's decline; the Port of Long Beach welcoming the largest container ship to call in North America; and Canadian National Railway expanding service to Prince Rupert. Manufacturing investment is rising, with Caterpillar breaking ground on a new $200 million facility in Georgia.

The document is a monthly economic report produced for Commerce Real Estate Solutions that summarizes revised employment data from Nevada, Las Vegas, and Reno-Sparks for 2010-2011. The key findings are:

1) Nevada, Las Vegas, and Reno-Sparks all saw upward revisions to 2010 and 2011 employment numbers, indicating the economies were more firmly in recovery than previously estimated.

2) Nevada gained an additional 12,900 jobs over the two-year period compared to earlier estimates.

3) The revisions show private service-producing sectors contributed significantly to employment growth in 2011 across the state.

Cushman & Wakefield North American Industrial Year End MarketbeatKatie Madanat

1) The North American economy expanded in 2011 despite turmoil in Europe. Industrial production and manufacturing increased while vacancy rates declined.

2) Leasing activity reached 417.1 million square feet in 2011, the highest level since 2007, as occupancy gains absorbed 137 million square feet of vacant space.

3) In Canada, the overall industrial vacancy rate fell to 6.2% in 2011 from 6.7% in 2010 due to absorption averaging 4.4 million square feet per quarter in the second half of the year.

36,778 sq. ft. building; Zoning: SE (Suburban Employment): The (SE) District allows numerous commercial site uses; Passenger elevator; Private and common restrooms; Fully sprinkled; Data center with a grounded floor and a specialized HVAC system; 60 KVA back-up generator; Building/pylon signage; Potential to purchase adjacent parcels; Sale Price: $4,413,360

Anilesh Ahuja Pioneering a Paradigm Shift in Real Estate Success.pptxneilahuja668

Anilesh Ahuja journey is a testament to the power of vision, resilience, and unwavering determination. As a visionary leader, he continues to inspire and empower others to dream big and challenge the status quo. His legacy extends far beyond the realm of real estate, leaving an indelible mark on the industry and the world at large.

Living in an UBER World - June '24 Sales MeetingTom Blefko

June 2024 Lancaster County Sales Meeting for Berkshire Hathaway HomeServices Homesale Realty covering the following topics: 1. VA Suspends Buyer Agent Payment Plan (article), 2. Frequently Used Terms in title, 3. Zillow Showcase Overview, 4. QuickBuy commission promotion, 5. Documenting Cooperative Compensation, 6. NAR's Code of Ethics - Mass Media Solicitations, 7. Is it really cheaper to rent? 8. Do's and Don't's when Terminating the Agreement of Sale, 9. Living in an UBER World

The SVN® organization shares a portion of their new weekly listings via their SVN Live® Weekly Property Broadcast. Visit https://svn.com/svn-live/ if you would like to attend our weekly call, which we open up to the brokerage community.

Why is Revit MEP Outsourcing considered an as good option for construction pr...MarsBIM1

Outsourcing MEP modeling services require effective collaboration and coordination amongst multiple engineering trades. The engineers and the designers often change the details of the MEP projects, but the work of Revit MEP drafting services is having the master plan and model of the complete project. To have proper coordination and installation, there is a need to execute the project effectively. Hence, the work of Revit family creation facilitates the MEP engineers.

Andhra Pradesh, known for its strategic location on the southeastern coast of India, has emerged as a key player in India’s industrial landscape. Over the decades, the state has witnessed significant growth across various sectors,

Listing Turkey - Piyalepasa Istanbul CatalogListing Turkey

We are working around the clock to transform a long-time dream into reality. As a result, Piyalepasa Istanbul will be the largest privately developed urban regeneration project in Turkey.

THE NEIGHBORHOOD WE HAVE BEEN LONGING FOR IS COMING TO LIFE

The good old days of the Piyalepasa neighborhood are being brought back to life with Piyalepasa Istanbul houses, residences, offices, hotels and a pedestrianized shopping avenue.

The wide streets of this 82.000 square meter development conveniently face the main boulevard in a prime Beyoglu location. “Piyalepaşa İstanbul” stands out as the only project designed to offer a neighborhood lifestyle, complete with its grocers, bagel sellers and greengrocer. Piyalepasa Istanbul has all the values to make it an authentic neighborhood, our very own community.

A NEIGHBORHOOD FULL OF LIFE, IN THE HEART OF THE CITY!

“Piyalepaşa İstanbul” is a “mixed-use” concept containing all the elements for a vibrant social life with houses, residences, offices, hotels and high street shopping.

“Piyalepaşa İstanbul” will take the liveliness of Istanbul into its heart. The elegant sparkle of Nisantasi, the young and colorful Besiktas, the variety and multicultural heritage of Istiklal Street will all be contained within the streets of this neighborhood.

“Piyalepaşa İstanbul” bears traces of the most beautiful examples of Turkish architecture from the Seljuks to the Ottomans and from Anatolia to Rumelia. With its graded facades, wide eaves, bay windows, pools, and interior courtyard systems, it offers a new living space without disrupting the city’s silhouette and neighborhood.

“Piyalepaşa İstanbul” is the new attraction of this splendid city.

TO BE AT THE CENTER OF ISTANBUL… THIS IS REAL LUXURY!

With its proximity to D-100 highway, connecting roads and tunnels, “Piyalepaşa İstanbul” is only minutes away from Kabatas, Besiktas, the Golden Horn and Karakoy.

“Piyalepaşa İstanbul” is close to the prestigious new Istanbul Court House, a major hospital, the Perpa trade center and the city’s most lively neighborhoods. With its shuttle service to Okmeydani Metrobus station, Sishane and the Court House subway stations, “Piyalepaşa İstanbul” will provide you with the most convenient transport connections.

https://listingturkey.com/property/piyalepasa-istanbul/

Stark Builders: Where Quality Meets Craftsmanship!shuilykhatunnil

At Stark Builders our vision is to redefine the renovation experience by combining both stunning design and high quality construction skills. We believe that by delivering both these key aspects together we are able to achieve incredible results for our clients and ensure every project reflects their vision and enhances their lifestyle.

Although we are not all related by blood we have created a team of highly professional and hardworking individuals who share the common goal of delivering beautiful and functional renovated spaces. Our tight nit team are able to work together in a way where we pour our passion into each and every project as we have a love for what we do. Building is our life.

Las Vegas Sun - Startups finding success with boost from Vegas Tech FundKatie Madanat

The Vegas Tech Fund has helped several tech startups find success and put down roots in Las Vegas. One startup the fund invested in was Romotive, which makes small remote-controlled robots called Romos. The $500,000 investment from Vegas Tech Fund helped Romotive grow from a few employees to 18, and partnering with the fund's leaders helped the company plan for growth. Now several other startups have received money from the Vegas Tech Fund and have also significantly grown their employee numbers and revenue thanks to the fund's support and connections to the Las Vegas community. The fund aims to increase tech innovation and the creative workforce in downtown Las Vegas.

A monthly report produced by Stephen P. A. Brown, PhD, of the Center for Business & Economic Research at the University of Nevada, Las Vegas discusses gasoline prices in Nevada and on the West Coast. Gasoline prices increased in 2012 due to tensions with Iran, low U.S. gasoline inventories, and refinery outages in California and Washington. Most indicators now suggest that gasoline prices have peaked and should begin to fall, with prices in Nevada expected to decline to around $3.50/gallon by December. However, prices on the West Coast may fall more slowly due to still low regional gasoline inventories.

This monthly report from the Center for Business & Economic Research at UNLV discusses the state of the US economy in August 2012. It finds that:

1) US GDP growth slowed to 1.3% in Q2 2012, below potential GDP.

2) Personal consumption spending was the largest contributor to GDP growth in the first half of 2012, outpacing overall GDP growth.

3) Business investment spending grew modestly while residential investment strengthened, suggesting moderate overall investment growth.

4) Government spending declines contributed to slowing GDP, though the impacts varied between federal and state/local levels.

Industrial Fact of the Week - US Leasing Activity over 500,000SFKatie Madanat

Leasing activity of large commercial spaces over 500,000 square feet in the U.S. peaked in 2007 at over 20 million square feet but declined during the market slowdown, reaching a low of 11.1 million square feet in 2010. The market began recovering in mid-2010 and leasing activity has increased since 2011, with the largest single lease being Home Depot's 1.6 million square foot build-to-suit deal in Chicago in 2011. So far this year, leasing activity for spaces over 500,000 square feet totals 15.5 million square feet across 20 deals predominantly in the manufacturing, retail, transportation, and wholesale industries

Cushman & Wakefield - North American Industrial Market Beat - Mid-Year 2012Katie Madanat

1) The document provides an economic overview of North America and discusses uncertainty in the US economy from issues in Europe and China.

2) It notes declines in US manufacturing in June 2012 and orders but that manufacturing activity revived in Canada in the first half of 2012.

3) Demand remains expansionary across most Canadian industrial real estate markets but challenging global conditions are translating to more caution in occupancy decisions, with stronger momentum in western Canadian markets like Alberta.

This document summarizes a monthly economic report on the fiscal cliff and its potential impact on the US economy. It finds that allowing all current tax increases and spending cuts to take effect could plunge the US back into recession due to the abrupt change in fiscal policy. However, failing to address the large budget deficit also poses long-term risks to economic growth. The report recommends a gradualist approach that gradually reduces the deficit to a sustainable level over several years to minimize near-term economic risks.

Cushman & Wakefield - Industrial Fact of the Week - July 10 12Katie Madanat

U.S. industrial warehouse demand is driven by housing activity. When housing starts and sales peaked in 2005, warehouse absorption also hit its peak. However, as the housing market declined from 2006 to 2009 due to the recession, warehouse absorption fell for 12 consecutive quarters. When the effects of the recession were felt in 2008, warehouse users reduced their space by 66.5 million square feet. By early 2009, warehouse absorption reached its lowest point during the recession. As the economy recovered in 2010, new housing starts increased which lifted housing sales and subsequently drove increased demand for warehouse space from retailers and suppliers. Over the past eight quarters, warehouse absorption has totaled 119.5 million square feet.

Las Vegas Nevada Fact Sheet Jan-Mar 2012Katie Madanat

The document provides an economic overview of the Las Vegas Valley region for January through March 2012. Some key points:

- Employment declined slightly in Las Vegas but grew in Clark County overall. Leisure and hospitality remained the largest sector.

- Tourism numbers increased year-over-year with over 9.7 million visitors in the first quarter. Gaming revenue was up 4.4% overall.

- The housing market showed signs of recovery with new home construction up and prices stabilizing. Apartment rents increased slightly but vacancies remained high.

- Commercial real estate markets saw some absorption across major sectors though vacancies persisted, especially in office space. New development activity was limited overall.

Cushman & Wakefield - Industrial Fact of the Week - May, 15 2012Katie Madanat

Retail sales continued to climb in the first quarter of 2012, reaching $1.2 trillion. Several retail sectors experienced double-digit annual growth. With increased demand from retailers and third-party logistics providers, industrial space leasing reached its highest level since 2007. The overall industrial vacancy rate declined to 9.0%, its lowest point since 2008, as industrial users absorbed over 99 million square feet of space since 2011. With demand outpacing supply, new speculative development of industrial space is increasing, with approximately 25 million square feet under construction to be completed in 2012.

This monthly report discusses the potential economic impact of higher oil prices in early 2012. It finds that while higher gasoline prices are noticeable, current oil price increases are unlikely to trigger a recession for three main reasons: 1) oil prices have not risen enough compared to the past three years to be recession-inducing, 2) natural gas prices have diverged from oil prices and lowered overall energy costs, and 3) the US economy has become less dependent on energy over time. The report also provides an overview of recent economic conditions in the US and Nevada.

North America Industrial Indicators - In 7 MinutesKatie Madanat

This document provides a 3-minute summary of industrial indicators for North America in April 2012. Key points include: container carriers leaving the Port of Seattle for Tacoma, which should reverse Tacoma's decline; the Port of Long Beach welcoming the largest container ship to call in North America; and Canadian National Railway expanding service to Prince Rupert. Manufacturing investment is rising, with Caterpillar breaking ground on a new $200 million facility in Georgia.

The document is a monthly economic report produced for Commerce Real Estate Solutions that summarizes revised employment data from Nevada, Las Vegas, and Reno-Sparks for 2010-2011. The key findings are:

1) Nevada, Las Vegas, and Reno-Sparks all saw upward revisions to 2010 and 2011 employment numbers, indicating the economies were more firmly in recovery than previously estimated.

2) Nevada gained an additional 12,900 jobs over the two-year period compared to earlier estimates.

3) The revisions show private service-producing sectors contributed significantly to employment growth in 2011 across the state.

Cushman & Wakefield North American Industrial Year End MarketbeatKatie Madanat

1) The North American economy expanded in 2011 despite turmoil in Europe. Industrial production and manufacturing increased while vacancy rates declined.

2) Leasing activity reached 417.1 million square feet in 2011, the highest level since 2007, as occupancy gains absorbed 137 million square feet of vacant space.

3) In Canada, the overall industrial vacancy rate fell to 6.2% in 2011 from 6.7% in 2010 due to absorption averaging 4.4 million square feet per quarter in the second half of the year.

36,778 sq. ft. building; Zoning: SE (Suburban Employment): The (SE) District allows numerous commercial site uses; Passenger elevator; Private and common restrooms; Fully sprinkled; Data center with a grounded floor and a specialized HVAC system; 60 KVA back-up generator; Building/pylon signage; Potential to purchase adjacent parcels; Sale Price: $4,413,360

Anilesh Ahuja Pioneering a Paradigm Shift in Real Estate Success.pptxneilahuja668

Anilesh Ahuja journey is a testament to the power of vision, resilience, and unwavering determination. As a visionary leader, he continues to inspire and empower others to dream big and challenge the status quo. His legacy extends far beyond the realm of real estate, leaving an indelible mark on the industry and the world at large.

Living in an UBER World - June '24 Sales MeetingTom Blefko

June 2024 Lancaster County Sales Meeting for Berkshire Hathaway HomeServices Homesale Realty covering the following topics: 1. VA Suspends Buyer Agent Payment Plan (article), 2. Frequently Used Terms in title, 3. Zillow Showcase Overview, 4. QuickBuy commission promotion, 5. Documenting Cooperative Compensation, 6. NAR's Code of Ethics - Mass Media Solicitations, 7. Is it really cheaper to rent? 8. Do's and Don't's when Terminating the Agreement of Sale, 9. Living in an UBER World

The SVN® organization shares a portion of their new weekly listings via their SVN Live® Weekly Property Broadcast. Visit https://svn.com/svn-live/ if you would like to attend our weekly call, which we open up to the brokerage community.

Why is Revit MEP Outsourcing considered an as good option for construction pr...MarsBIM1

Outsourcing MEP modeling services require effective collaboration and coordination amongst multiple engineering trades. The engineers and the designers often change the details of the MEP projects, but the work of Revit MEP drafting services is having the master plan and model of the complete project. To have proper coordination and installation, there is a need to execute the project effectively. Hence, the work of Revit family creation facilitates the MEP engineers.

Andhra Pradesh, known for its strategic location on the southeastern coast of India, has emerged as a key player in India’s industrial landscape. Over the decades, the state has witnessed significant growth across various sectors,

Listing Turkey - Piyalepasa Istanbul CatalogListing Turkey

We are working around the clock to transform a long-time dream into reality. As a result, Piyalepasa Istanbul will be the largest privately developed urban regeneration project in Turkey.

THE NEIGHBORHOOD WE HAVE BEEN LONGING FOR IS COMING TO LIFE

The good old days of the Piyalepasa neighborhood are being brought back to life with Piyalepasa Istanbul houses, residences, offices, hotels and a pedestrianized shopping avenue.

The wide streets of this 82.000 square meter development conveniently face the main boulevard in a prime Beyoglu location. “Piyalepaşa İstanbul” stands out as the only project designed to offer a neighborhood lifestyle, complete with its grocers, bagel sellers and greengrocer. Piyalepasa Istanbul has all the values to make it an authentic neighborhood, our very own community.

A NEIGHBORHOOD FULL OF LIFE, IN THE HEART OF THE CITY!

“Piyalepaşa İstanbul” is a “mixed-use” concept containing all the elements for a vibrant social life with houses, residences, offices, hotels and high street shopping.

“Piyalepaşa İstanbul” will take the liveliness of Istanbul into its heart. The elegant sparkle of Nisantasi, the young and colorful Besiktas, the variety and multicultural heritage of Istiklal Street will all be contained within the streets of this neighborhood.

“Piyalepaşa İstanbul” bears traces of the most beautiful examples of Turkish architecture from the Seljuks to the Ottomans and from Anatolia to Rumelia. With its graded facades, wide eaves, bay windows, pools, and interior courtyard systems, it offers a new living space without disrupting the city’s silhouette and neighborhood.

“Piyalepaşa İstanbul” is the new attraction of this splendid city.

TO BE AT THE CENTER OF ISTANBUL… THIS IS REAL LUXURY!

With its proximity to D-100 highway, connecting roads and tunnels, “Piyalepaşa İstanbul” is only minutes away from Kabatas, Besiktas, the Golden Horn and Karakoy.

“Piyalepaşa İstanbul” is close to the prestigious new Istanbul Court House, a major hospital, the Perpa trade center and the city’s most lively neighborhoods. With its shuttle service to Okmeydani Metrobus station, Sishane and the Court House subway stations, “Piyalepaşa İstanbul” will provide you with the most convenient transport connections.

https://listingturkey.com/property/piyalepasa-istanbul/

Stark Builders: Where Quality Meets Craftsmanship!shuilykhatunnil

At Stark Builders our vision is to redefine the renovation experience by combining both stunning design and high quality construction skills. We believe that by delivering both these key aspects together we are able to achieve incredible results for our clients and ensure every project reflects their vision and enhances their lifestyle.

Although we are not all related by blood we have created a team of highly professional and hardworking individuals who share the common goal of delivering beautiful and functional renovated spaces. Our tight nit team are able to work together in a way where we pour our passion into each and every project as we have a love for what we do. Building is our life.

Signature Global TITANIUM SPR | 3.5 & 4.5BHK High rise Apartments in Gurgaonglobalsignature2022

Signature Global TITANIUM SPR launched a high rise apartments in Gurgaon . In this project Signature Global offers 3.5 & 4.5 BHK high rise Apartment at sector 71 Gurgaon SPR Road. Signature Global Titanium SPR is IGBC Gold certified, a testament to our commitment to sustainability.

Signature Global TITANIUM SPR | 3.5 & 4.5BHK High rise Apartments in Gurgaon

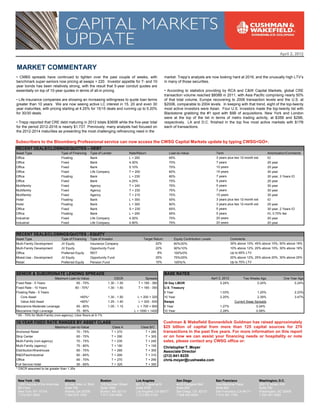

Cushman & Wakefield - Capital Markets Update

1. April 2, 2012

MARKET COMMENTARY

• CMBS spreads have continued to tighten over the past couple of weeks, with market. Trepp’s analysts are now looking hard at 2016, and the unusually high LTV’s

benchmark super-seniors now pricing at swaps + 220. Investor appetite for 7- and 10- in many of those securities.

year bonds has been relatively strong, with the result that 5-year conduit quotes are

essentially on top of 10-year quotes in terms of all-in pricing. • According to statistics providing by RCA and C&W Capital Markets, global CRE

transaction volume reached $808B in 2011, with Asia Pacific comprising nearly 50%

• Life insurance companies are showing an increasing willingness to quote loan terms of that total volume, Europe recovering to 2006 transaction levels and the U.S. at

greater than 10 years. We are now seeing active LC interest in 15, 20 and even 30 $200B, comparable to 2004 levels. In keeping with that trend, eight of the top-twenty

year maturities, with pricing starting at 4.25% for 15/15 deals and running up to 5.20% most active investors were Asian. Four U.S. investors made the top-twenty list with

for 30/30 deals. Blackstone grabbing the #1 spot with $9B of acquisitions. New York and London

were at the top of the list in terms of metro trading activity, at $35B and $29B,

• Trepp reported that CRE debt maturing in 2012 totals $360B while the five-year total respectively. LA and D.C. finished in the top five most active markets with $17B

for the period 2012-2016 is nearly $1.73T. Previously, many analysts had focused on each of transactions.

the 2012-2014 maturities as presenting the most challenging refinancing need in the

Subscribers to the Bloomberg Professional service can now access the CWSG Capital Markets update by typing CWSG<GO>.

2 3 4 5 8 10 18

RECENT DEALS/CLOSINGS/QUOTES – DEBT

Asset Type Type of Financing Type of Lender Rate/Return Loan-to-Value Term Amortization/Comments

Office Floating Bank L + 250 65% 3 years plus two 12-month ext. IO

Office Fixed Bank 4.30% 70% 7 years 25 year

Office Fixed Bank 5.10% 70% 10 years 25 year

Office Fixed Life Company T + 200 60% 15 years 30 year

Office Floating Bank L + 235 60% 7 years 30 year, 3 Years IO

Office Fixed Bank 4.25% 75% 5 years 25 year

Multifamily Fixed Agency T + 240 75% 5 years 30 year

Multifamily Fixed Agency T + 230 75% 7 years 30 year

Multifamily Fixed Agency T + 210 75% 10 years 30 year

Hotel Floating Bank L + 300 55% 3 years plus two 12-month ext. IO

Hotel Floating Bank L + 300 60% 3 years plus two 12-month ext. 25 year

Office Fixed Bank S + 230 65% 5 years 30 year, 2 Years IO

Office Floating Bank L + 250 65% 5 years IO, 0.75% fee

Industrial Fixed Life Company 4.30% 70% 20 years 20 year

Industrial Fixed Life Company 4.90% 75% 20 years 20 year

2 3 4 5 8 10

RECENT DEALS/CLOSINGS/QUOTES - EQUITY

Asset Type Type of Financing Type of Investor Target Return Equity Contribution Levels Comments

Multi-Family Development JV Equity Insurance Company 22% 80%/20% 35% above 10%, 45% above 15%, 50% above 18%

Multi-Family Development JV Equity Opportunity Fund 22% 90%/10% 10% above 12%, 20% above 15%, 30% above 18%

Office Preferred Equity REIT 8% 100%/0% Up to 65% LTV

Mixed-Use - Development JV Equity Opportunity Fund 25% 75%/25% 20% above 12%, 25% above 20%, 30% above 25%

Retail Preferred Equity Pension Fund 10% 100%/% Up to 70% LTV

SENIOR & SUBORDINATE LENDING SPREADS BASE RATES

Maximum Loan-to-Value DSCR Spreads April 2, 2012 Two Weeks Ago One Year Ago

Fixed Rate - 5 Years 65 - 70% 1.30 - 1.50 T + 195 - 380 30 Day LIBOR 0.24% 0.24% 0.24%

Fixed Rate - 10 Years 60 - 70%* 1.30 - 1.50 T + 165 - 350 U.S. Treasury

Floating Rate - 5 Years 5 Year 1.03% 1.20% 2.23%

Core Asset <65%* 1.30 - 1.50 L + 200 + 325 10 Year 2.20% 2.39% 3.47%

Value Add Asset <65%* 1.25 - 1.40 L + 325 - 500 Swaps Current Swap Spreads

Mezzanine Moderate Leverage 65 - 80% 1.05 - 1.15 L + 700 + 900 5 Year 1.27% 0.24%

Mezzanine High Leverage 75 - 90% L + 1000 + 1400 10 Year 2.28% 0.08%

* 65 - 70% for Multi-Family (non-agency); Libor floors at 0-1%

10-YEAR FIXED RATE RANGES BY ASSET CLASS Cushman & Wakefield Sonnenblick Goldman has raised approximately

Maximum Loan-to-Value Class A Class B/C $25 billion of capital from more than 125 capital sources for 270

Anchored Retail 70 - 75% T + 270 T + 280 transactions in the past five years. For more information on this report

Strip Center 65 - 70% T + 290 T + 305 or on how we can assist your financing needs or hospitality or note

Multi-Family (non-agency) 70 - 75% T + 235 T + 240 sales, please contact any CWSG office or:

Multi-Family (agency) 75 - 80% T + 190 T + 195

Christopher T. Moyer

Distribution/Warehouse 65 - 70% T + 285 T + 300 Associate Director

R&D/Flex/Industrial 60 - 65% T + 295 T + 310 (212) 841-9220

Office 65 - 70% T + 270 T + 290 chris.moyer@cushwake.com

Full Service Hotel 55 - 65% T + 325 T + 350

* DSCR assumed to be greater than 1.35x

New York - HQ Atlanta Boston Los Angeles San Diego San Francisco Washington, D.C.

1290 Avenue of the Americas 55 Ivan Allen Jr. Blvd. 125 Summer Street 601 S. Figueroa St. 4435 Eastgate Mall One Maritime Plaza 2001 K Street, NW

8th Floor Suite 700 Suite 1500 Suite 4700 Suite 200 Suite 900 Suite 700

New York, NY 10104 Atlanta, GA 30308 Boston, MA 02110 Los Angeles, CA 90017 San Diego, CA 92121 San Francisco, CA 94111 Washington, DC 20006

T 212 841 9200 T 404 875 1000 T 617 330 6966 T 213 955 5100 T 858 452 6500 T 415 397 1700 T 202 467 0600