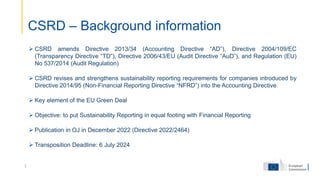

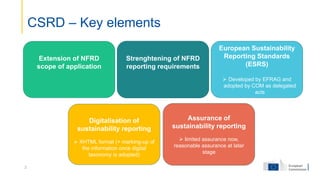

The Corporate Sustainability Reporting Directive (CSRD), effective from July 6, 2024, amends existing EU directives to enhance sustainability reporting for large and listed companies, aiming to align it with financial reporting standards. Key elements include the introduction of European Sustainability Reporting Standards (ESRS), digitalization of reports, and assurance requirements, initially limited before transitioning to reasonable assurance. The directive also expands the scope to include non-EU companies with significant EU operations and requires comprehensive reporting on sustainability impacts and risks.

![What Is Blockchain Technology A Simple Beginner’s Guide [2026]](https://cdn.slidesharecdn.com/ss_thumbnails/whatisblockchaintechnologyasimplebeginnersguide2026-260101112141-cf432b44-thumbnail.jpg?width=640&height=640&fit=bounds)