More Related Content

More from mjcunny

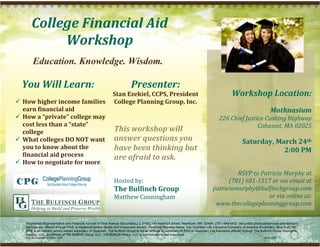

College Financial Aid

- 1. College Financial Aid Workshop Education. Knowledge. Wisdom. You Will Learn: Presenter: Stan Ezekiel, CCPS, President Workshop Location: How higher income families College Planning Group, Inc. earn financial aid Mathnasium How a “private” college may 226 Chief Justice Cushing Highway cost less than a “state” Cohasset, MA 02025 college This workshop will What colleges DO NOT want answer questions you Saturday, March 24th you to know about the have been thinking but 2:00 PM financial aid process are afraid to ask. How to negotiate for more RSVP to Patricia Murphy at Hosted by: (781) 6811517 or via email at The Bulfinch Group patriciamurphy@bulfinchgroup.com Matthew Cunningham or via online at: www.thecollegeplanninggroup.com Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS) 140 Kendrick Street, Needham, MA 02494, (781) 449-4402. Securities products/services and advisory services are offered through PAS, a registered broker-dealer and investment advisor. Financial Representative, The Guardian Life Insurance Company of America (Guardian), New York, NY. PAS is an indirect, wholly owned subsidiary of Guardian. The Bulfinch Group is not an affiliate or subsidiary of PAS or Guardian. Life insurance offered through The Bulfinch Group Insurance Agency, LLC, an affiliate of The Bulfinch Group, LLC. The Bulfinch Group, LLC is not licensed to sell insurance. PAS is a member of FINRA, SIPC 2012-1257 .