Downloaded 91 times

![there is no tax liability. Therefore, the essential condition for a tax demand is

the service of demand notice. The due date is prescribed in section 220(1) of

the I.T Act, 1961 and can be shortened by the AO if he is of the opinion that

granting of 30 days time is detrimental to the interests of revenue. However, as

per the proviso to section 220(1), such action should be taken only after

obtaining approval of the Joint/Addl Commissioner of Income Tax. However, this

power needs to be exercised with caution. As stated by the Andhra Pradesh

High Court in the case of Subbshree Trading Enterprises Pvt Ltd Vs ACIT [111

STC 144], the decision to shorten the due date cannot be taken in an

overzealous and hasty manner.

6. ASSESSEE IN DEFAULT:

If an assessee does not make the payment of the demanded tax within the due

date, he shall be deemed as an “assessee deemed in default” u/s 220(4) of the

I.T Act, 1961. The other situations in which an assessee shall be treated as an

assessee in default/deemed to be in default are when there is default in;

i. deduction or deposit of TDS (u/s 201(1))

ii. advance tax payment (u/s 218)

iii. payment of self-assessment tax (u/s 140A(3)) and

iv. payment of installments granted (u/s 220(5))

A third party to whom notice u/s 226(3) (garnishee notice) is issued shall also

be treated as an “assessee deemed to be in default” u/s 226(3)(x), in case of

non-compliance of the notice. To avoid the tag of being in default, an assessee

can file an application before the AO under section 220(3) before the expiry of

the due date, seeking installments or extension of time for payment of the

demand. In such a case, the AO has discretion to grant installments or

extension of time subject to conditions as he may think fit to impose in the

circumstances of the case. But, eithergrant of installments or extension of time

does not entitle the assessee to for non-levy of interest. An assessee in default,

is akin to a debtor of the Government of India and will be visited with pecuniary

and non-pecuniary consequences.

7. LEVY OF INTEREST U/S 220(2):

Levy of interest is an automatic consequence that falls on any assessee in

default. The rate of interest underwent through lot of changes since the

inception of the Act and the present rate of interest stands at 1% per month or

part of the month. Interest charged u/s 220(2) is compensatory in nature and

the levy is automatic. There is no need to give opportunity to the assessee

before levy of interest u/s 220(2). No appeal lies against levy of interest1.

i. MANNER OF COMPUTATION AND ADJUSTMENT OF INTEREST:

Rule 119A of the I.T Rules prescribed the method for computation of interest

u/s 220(2). Till 31-03-1989, interest was calculated on annual basis. In such a

case, part of the month shall be ignored. From 01-04-1989, interest is

calculated on monthly basis. In such a case, part of the month shall be treated

as full month. If a period spans from a date prior to 01-04-1989 to a date after,

then interest for the part prior to 01-04-1989 shall be calculated on annual

basis and on monthly basis for the post 01-04-1989 period. Tax (including

penalty or any other sum) on which interest is computed shall be rounded off to

the nearest hundred and any fraction of hundred shall be ignored while

rounding off. As per instruction no. 1936 dated 21-03-1996, whenever an

amount is collected towards pending demand, credit shall first be1 An interested

reader can read the judgment of Madras High Court in the case of Suresh Gokuldas [229 ITR

721]. given to the tax and then to the interest. In other words, the amount shall](https://image.slidesharecdn.com/collectionandrecovery-sai-bose-121115222208-phpapp02/75/Collection-and-recovery-sai-bose-4-2048.jpg)

![first be adjusted towards tax and only when the tax demand is fully met,

adjustment towards interest is to be made.

ii. COMPUTATION OF INTEREST ON VARIATION OF DEMAND:

It is not uncommon to see that in most of the cases, demand which is initially

created undergoes changes. This can happen due to reduction or enhancement

in appeal, set aside, cancellation, revision, rectification or reassessment.

Circular no. 334 deals with some of the situations. Following are some of the

examples:

a. If there is reduction of demand in appeal, interest is payable on the final

demand from the due date mentioned in original demand notice served on the

assessee i.e interest is payable from the due date immediately arising out of the

assessment order (may be referred as original due date)

b. If there is enhancement in demand (either in appeal or in revision or upon

rectification), new demand notice shall be issued only for the new demand and

interest on the new demand shall be paid from the new due date. However,

interest on demand which is already pending shall be from the original

due date

c. If the assessment is set aside in one appeal but restored back in further

appeal, interest shall be paid from the original due date

d. In case of reassessment also, interest is leviable on the old demand from the

original due date2

e. Care should be taken while giving effect to appellate orders in light of the

judgment of Supreme Court in the case of Killick Nixon Ltd Vs CIT [258 ITR

627]3

2

Nb Mir Barkat Ali Khan Vs ITO [172 ITR 13] (AP)

3

In this case, CIT(A) granted relief on certain issues and set aside the matter on certain issues.

The AO, while passing the modification order, computed the revised income after considering

relief granted by the CIT(A) but on the set aside issues kept the matter pending for verification.

Meanwhile, the assessee utilized the KVSS scheme to settle his case on the basis of the

modification order. Thereafter, the AO issues a notice for verification of the issues set aside by

the CIT(A). Assessee replied that no further verification can be made as his case is covered

under KVSS. On appeal, the Apex Court held that once the AO has passed the modification order,

all the issues are treated as considered by him and therefore, it cannot be stated that there is

scope for issue of further notice for verification. In light of this order, it is better to pass a single

modification order considering all the issues decided in appeal.

iii. WAIVER/REDUCTION OF INTEREST U/S 220(2A):

Interest levied or to be levied u/s 22)(2) can be waived off or reduced by the

CCIT/CIT, upon application by the assessee, whenthe CCIT/CIT is satisfied that;

1. genuine hard ship would be caused to the assessee and

2. non-payment of tax was due to circumstances beyond the control of the

assessee and

3. the assessee has cooperated in the enquiries for assessment and recovery

The CCIT/CIT can waive/reduce the interest only when the above three

conditions are cumulatively fulfilled.

iv. ADDITIONAL READING MATERIAL ON VARIATION OF INTEREST:

In case full tax is paid by the assessee upon demand but refund was issued due

to order of CIT(A), there is no need for the assessee to pay interest on original

demand even after ITAT restores the order of AO as per the judgment of Kerala

High Court in the case of A V Thomas & Co [160 ITR 818]. In a case where

assessment is fully set aside, the demand goes into abeyance. In equal breadth,

the assessee is also not entitled for any refund before fresh assessment is

made. Nothing is due to revenue nor to the assessee till fresh assessment is

made as held by the Apex Court in the case of CIT Vs Chittor Electric Supply](https://image.slidesharecdn.com/collectionandrecovery-sai-bose-121115222208-phpapp02/75/Collection-and-recovery-sai-bose-5-2048.jpg)

![Corporation [212 ITR 404].

v. ADDITIONAL READING MATERIAL ON WAIVER/REDUCTION OF INTEREST:

Courts cannot interfere with the discretionary power of the CCIT/CIT u/s

220(2A) as held by the Kerala High Court in the case of GTN Textiles Ltd Vs CIT

[217 ITR 653].

Similarly, once the application of the assessee is rejected, second application by

the assessee is not maintainable. Settlement Commission does not have

unrestricted powers to waive the interest paid/payable u/s 220(2) as held by

the Apex Court in the case of CIT Vs Damani Brothers [259 ITR 475]. But,

Settlement Commission can consider the circumstances mentioned in section

220(2A) in the manner in which CCIT/CIT considers them.

8. POWER TO TREAT AN ASSESSEE AS NOT IN DEFAULT U/S

220(6):

When an assessee preferred appeal before the CIT(A) u/s 246 or 246A, he can

file a petition seeking stay of demand before the AO. The Act bestows

discretion4 on the AO to consider such cases for treating the assessee as not in

default till the time appeal is disposed off but subject to imposition of conditions

that are fit. As propounded by the Kerala High Court in the case of Pradeep

Ratanshi Vs ACIT & another [221 ITR 502], this discretion lies only with the AO.

It goes without saying that whenever a petition seeking stay is filed,

opportunity of hearing is a must before disposal of the petition. Apart from the

AO, the CIT(A) also enjoys the power to grant to stay which is implicit in his

jurisdiction as heldby the Apex Court in the case of ITO Vs M K Mohammad

Kunhi [71

ITR 815].

i. GUIDE LINES ISSUED BY CBDT THROUGH INSTRUCTION NO. 1914:

CBDT has issued comprehensive guidelines on the power to treat an assessee

not to be in default (termed as stay in common parlance) through Instruction

no. 1914. Circular nos. 530 and 589 also cover the issue of stay. The following

are the guidelines thatemerge from the instruction as well as the circulars:

Any demand should be recovered as soon as it is due

Primary responsibility of collection of demand lies with the AO and when

TRC is drawn with the TRO

Mere issue of show cause notice to the assessee does not amount to efforts

made by the AO for collection

Mere filing of appeal does not entitle the assessee for automatic stay of

collection of demand

Stay can be considered in cases where the AO adopted an interpretation of

law which is different that pronounced by various High Courts or the

jurisdictional High Court when the judgment is not accepted.

Stay can also be considered with respect to additions where the assessee

already won the case for earlier years.

Only demand related to the disputed additions needs to be considered for

stay.

4

Supreme Court in a land mark judgment in the case of S G Jaisinghani Vs Unionof India [65 ITR

34] held that discretion should be within defined limits and to beguided by law. Discretion should

be predictable and based on known principles oflaw. It should not be vague, arbitrary or fanciful.

It should be governed by rule oflaw and not humour. The Apex Court also held that whenever

discretion wasabsolute, man has suffered.

Assessee has to cooperate for early finalization of appeal

In case of reversal of judgment relied upon by the assessee, stay stands

vacated.](https://image.slidesharecdn.com/collectionandrecovery-sai-bose-121115222208-phpapp02/75/Collection-and-recovery-sai-bose-6-2048.jpg)

![Present financial capacity of the assessee is also one of the considerations

for grant of stay

Any petition for stay should be disposed off within two weeks of filing by

passing a speaking order

Ordinarily, the power to grant stay should be exercised only by the AO or

his immediate superior. Higher authorities should intervene only in exceptional

circumstances.

While granting stay, AO can impose suitable conditions like grant of

installments, insistence for lump sum payment or seek security

AO may reserve the right to review the order after a reasonable period of

time

AO also has the right to adjust refunds, if any

Liberal installments up to 18 months can be granted in suitable cases

The expression “stay of demand” should not be used in the order on the

petition for stay. Instead, the words “not treated as assessee in default for the

time being” as mentioned in section 220(6) shall be used.

ii. ADDITIONAL MATERIAL ON GRANT OF STAY:

In the case of Hindusthan Rubber Works Ltd Vs ITO [81 ITR 397], the Kolkata High Court

held that grant of stay for limited period is not proper. Similarly, in the case of Gajanan

Agencies Vs ITO [210 ITR 865], the Kerala High Court held that section 220(6) does not

contemplate installments. It is felt by the author that these cases have little relevance in

light of Instruction no. 1914, which clearly permits grant of stay for limited period and also

grant of scheme of installments. As per section 220(7), when an assessee has been

assessed on income arising from a foreign country, whose regulations do not permit

transfer of money, the AO shall not treat the assessee as a defaulter in respect of tax

related to such income till the time restrictions on the transfer of money are lifted except in

cases where the money was utilized or could have been utilized for meeting expenditure in

that country.

9. STAY OF DEMAND DURING SECOND APPEAL BEFORE ITAT:

The Act does not bestow any powers to the Income Tax authorities to grant stay of

collection of demand after the first appeal is disposed off and second appeal is filed by the

assessee before ITAT. The statutory power in such cases is vested with ITAT. As per first

proviso to section 254(2A), in cases where stay of collection of demand is granted by ITAT,

the appeal shall be decided within 180 days of the order granting stay. If not, as per

second proviso to the same section, the order granting stay shall stand automatically

vacated. However, in practical situation, even in cases where appeal is pending before

ITAT, assessees file petitions for stay before IT authorities and the same are considered by

them. This is because of the reason that before considering any stay petition, normally

ITAT demands the assessee to state whether his petition for stay of demand is rejected by

IT authorities or not. Another reason is that there is possibility of collection of at least part

of the demand by way of grant of installments etc by I.T authorities themselves so that

litigation on this issue is avoided and precious time is saved by both the sides. However,

the practice is purely administrative in nature and guided by conventions rather any specific

procedure laid down for this purpose.

10. PENALTY U/S 221:

Penalty is not a mode of recovery. In case of an assessee deemed to be in

default, penalty u/s 221 can be levied for nonpayment of taxes within due date.

This power is specific to AO only. This penalty can also be levied from time to

time but the total amount of the penalty cannot exceed the total amount of tax

demanded. Levy of penalty is discretionary where as levy of interest u/s 220(2)

is automatic. If the assessment goes in appeal, penalty u/s 221 also goes.

Penalty u/s 221 can be levied in case of TDS default as well as default in](https://image.slidesharecdn.com/collectionandrecovery-sai-bose-121115222208-phpapp02/75/Collection-and-recovery-sai-bose-7-2048.jpg)

![If a defaulter dies during recovery proceedings, the proceedings will be

continued against the legal representatives of the deceased. In case, the

assessee dies before drawl of TRC, TRC has to be drawn against the legal

representatives of the deceased.

Appeal from the original order of the TRO lies with the CCIT/CIT and shall

be filed within 30 days of the date of the order. If the appellate authority

directs, the recovery proceedings can be stayed pending disposal of the appeal.

Review of the order can also be done by the CCIT/CIT after giving notice to

all interested parties to correct mistakes if any.

12. OTHER MODES OF RECOVERY PRESCRIBED U/S 226:

Apart from the modes of recovery prescribed in section 222, department can also employ

other modes, which are prescribed in sections 226 to 228A and 232. In this section the

modes prescribed u/s 226 are described. It is worthwhile to mention here that as provided

in section 226(1), recourse to section 226 can be taken by the AO only when TRC is not

drawn. Once, TRC is drawn, only TRO can take action u/s 226.

i. ATTACHMENT OF SALARY U/S 226(2):

If the assessee has any income chargeable under the head “salaries”, the

AO/TRO can send a notice of attachment to the payer of the salary and require

him to deposit the salary towards tax arrears of the assessee subject to the

exemptions from attachment laid down in section 60 of CPC.

ii. GARNISHEE PROCEEDINGS U/S 226(3):

Section 226(3) is widely used by AOs and TROs in the Department. Under this

section, AO/TRO can attach any sum due or likely to be due from a third party

to the assessee and require the third party to deposit the sum towards tax

arrears of the assessee. Such proceedings are described as garnishee

proceedings in common parlance and details are described below:

Garnishee notice can be issued from time to time by the AO/TRO to a third

party to realize arrears pending against an assessee

Single notice can be issued for arrears of various years or separate notices

can be issued

A copy of the notice shall be marked to the assessee for information

The notice can be issued to realize amounts which are already due or that

or likely to be due. This does not mean that amounts from unascertained future

obligations, which are non-existent at present, can be attached.

AO/TRO can revoke or amend the notice, if necessary

If any garnishee declares that no such sum is due to the assessee from him,

the declaration has to be made in the form of a statement on oath

AO/TRO shall issue a receipt to the garnishee for the amounts received from

him

The liability of the garnishee is personal in nature and in case of non-

compliance to the notice, the garnishee will be deemed to be an assessee in

default

Garnishee like a Bank or Post Office or Insurance Company cannot insist for

production of pass book or deposit receipt or policy or any other document for

the purpose of entry or endorsement or for any other purpose before making

the payment even if such procedure is prescribed before payment of money in

the normal course of business

Fixed deposits can be realized even before maturity as held by the

Karnataka High Court in the case of Vysya Bank Ltd, Global Trust Bank Ltd Vs

JCIT [241 ITR 178].

iii. APPLICATION BEFORE COURT U/S 226(4):](https://image.slidesharecdn.com/collectionandrecovery-sai-bose-121115222208-phpapp02/75/Collection-and-recovery-sai-bose-11-2048.jpg)

![In cases where money belonging to a defaulter-assessee is lying in the custody

of a Court, the AO/TRO can apply to the Court of Law seeking release of the

money towards tax arrears and the court can release the same. In this regard,

it is worth while to mention here that the Court has no power to look into the

extent of the liability but has the power to determine that how much amount

can be released as held by the Supreme Court in the case of Harshad Shantilal

Mehta Vs Custodian [231 ITR 871].

iv. ATTACHMENT AND SALE OF MOVABLE PROPERTY U/S 226(5):

This sub-section enables the AO/TRO to recover arrears by distraint and sale of

movable property as per the procedure laid down in Schedule III of the I.T Act,

1961 when empowered by the CCIT/CIT through a general or special order.

Schedule III of the I.T Act states that the procedure for attachment and sale is

in the same manner as the procedure laid down in Schedule II of the I.T Act.

13. SOME OTHER MODES OF RECOVERY:

TRO can also put forward his claim before BIFR/DRT. TRO can also forward his

claim to liquidator of a company, wherever applicable. In the case of BIFR and

liquidator of a company, they on their won will give notice to the I.T

Department seeking details of claims pending. In case of a liquidator, if he fails

to seek the claims and settles the property without accounting for the claims of

the Department, he shall be held personally liable. DIT(Recovery) is the nodal

agency in case of applications pending before BIFR. In case of Private Ltd

companies, arrears can be realized from the personal assets of the Directors by

seeking recourse to section 179 of the I.T Act, 1961. In case of a firm, arrears

can be realized from the personal assets of the partners. Representative

assessees or agents are also liable to pay the arrears of the persons whom they

represent in the assessment proceedings. As per the provisions of section 227,

recovery can be effected through State Government whenever collection from a

particular area is assigned to the State Government. Tax in such case is to be

collected by the State Government in like manner employed for collection of

municipal tax. Tax arrears can also be realized from the foreign assets of the

assessee, if any, through agreements with foreign countries as provided in

section 228A of the I.T Act. However, the matter has to be referred to CBDT for

recovery. Similarly, upon receipt of reference from other countries by CBDT, tax

arrears of defaulters of a foreign country have to recovered and remitted to the

tax authorities of that country. Lastly, as per the saving clause in section 232,

tax arrears can also be realized through institution of civil suit.

14. PROSECUTION U/S 276:

Whenever any person fraudulently removes, conceals, transfers or delivers to

any other person; any property or interest therein; intending thereby to prevent

execution of recovery proceedings under Schedule II of the I.T Act, 1961, such

person shall be punishable with rigorous imprisonment up to 2 years and also

shall also be liable to fine.

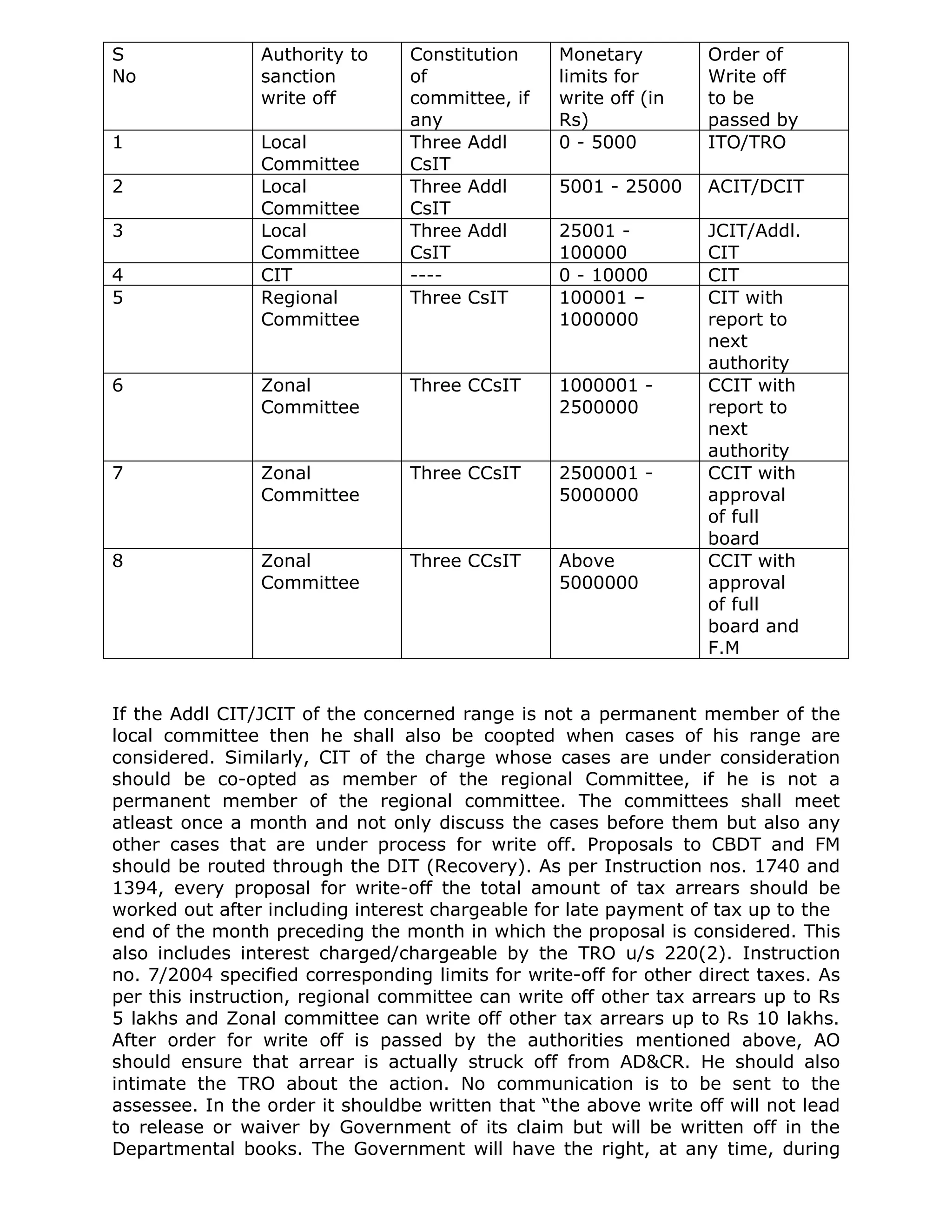

15. WRITE OFF/SCALING DOWN OF ARREARS:

Write off/scaling down is a mechanism to reduce the arrears in the books of the

Department, wherever there is no chance for recovery. This is purely an internal

affair of the Department and the assessee is not involved at all. In fact, there is

no need to inform the assessee that the amounts are written off or scaled down.

The procedure is also only administrative in nature and there is no statutory

write off or scaling down. Chapter 13 of the Manual of Office Procedure 2003

contains detailed procedure on write off/ scaling down. Instruction nos. 7/2004,

14/2003, 16/2003 and 1740/1986 lay down the revised monetary limits and

powers of various departmental committees constituted for write off. There are](https://image.slidesharecdn.com/collectionandrecovery-sai-bose-121115222208-phpapp02/75/Collection-and-recovery-sai-bose-12-2048.jpg)

This document provides a summary of provisions related to tax collection and recovery in India. It discusses key sections of the Income Tax Act that deal with collection and recovery (sections 220-232). It outlines the legislative history of changes to various sections over time. It then discusses the concepts of an "assessee in default" and levy of interest on defaulted payments. Specific topics covered include when tax is payable, deeming a taxpayer in default, computation of interest on defaulted payments, and how interest is adjusted in cases where the tax demand amount changes over time such as due to appeals.