Download as PDF, PPTX

![15Bain&Co. - Brazil Consumer Pul ...NYCThis information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent

Reference to have a better understanding on the next slides

“Net percentage spending more” Time reference Future expectations

Q: “How did your spending change in [product/service X]

since the pandemic began?”

Respondents change in spending

(%, change/ total respondents)

% respondents

spending somewhat

or significantly

more than before

% respondents

spending about the

same than before

% respondents

spending somewhat

or significantly less

than before

Net %

spending more

(NSM)

=

% respondents

spending somewhat

or significantly more

than before

% respondents

spending somewhat

or significantly less

than before

-

Net % spending more

(%)

E X A M P L E

The information shown at each

month reflects the

accumulated value from the

beginning of pandemic until

the respective month

Net % spending more expectations

(%)

E X A M P L E

Long

term

Refers to

expected

values

after +12

months

Mid term

Refers to

expected

values

within the

next 12

months

[Month]

Refers to

current

values

recorded

in the last

survey

I L L U S T R A T I V E](https://image.slidesharecdn.com/bainco-200720162426/75/Brazil-s-Consumer-Pulse-Update-15-2048.jpg)

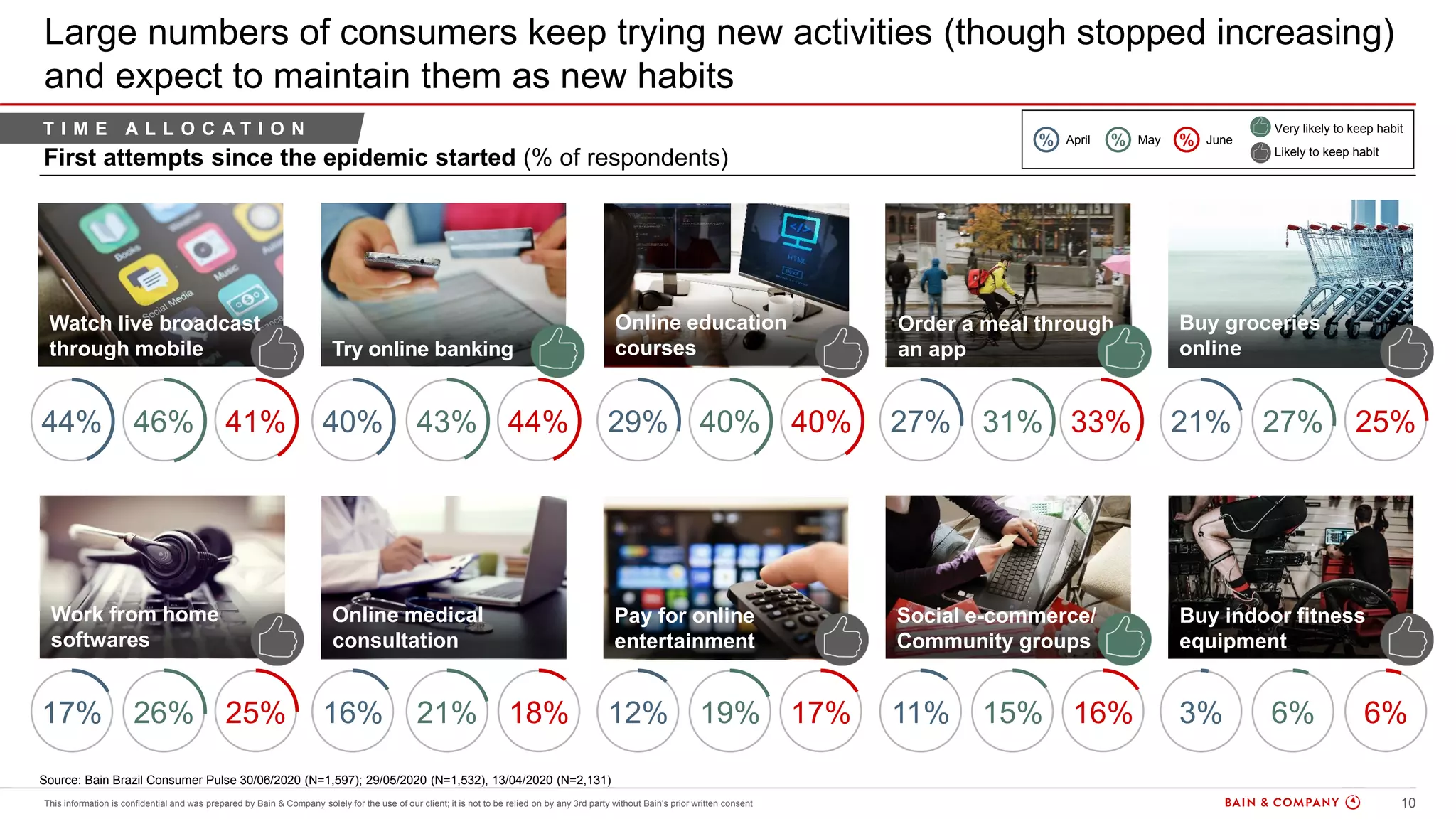

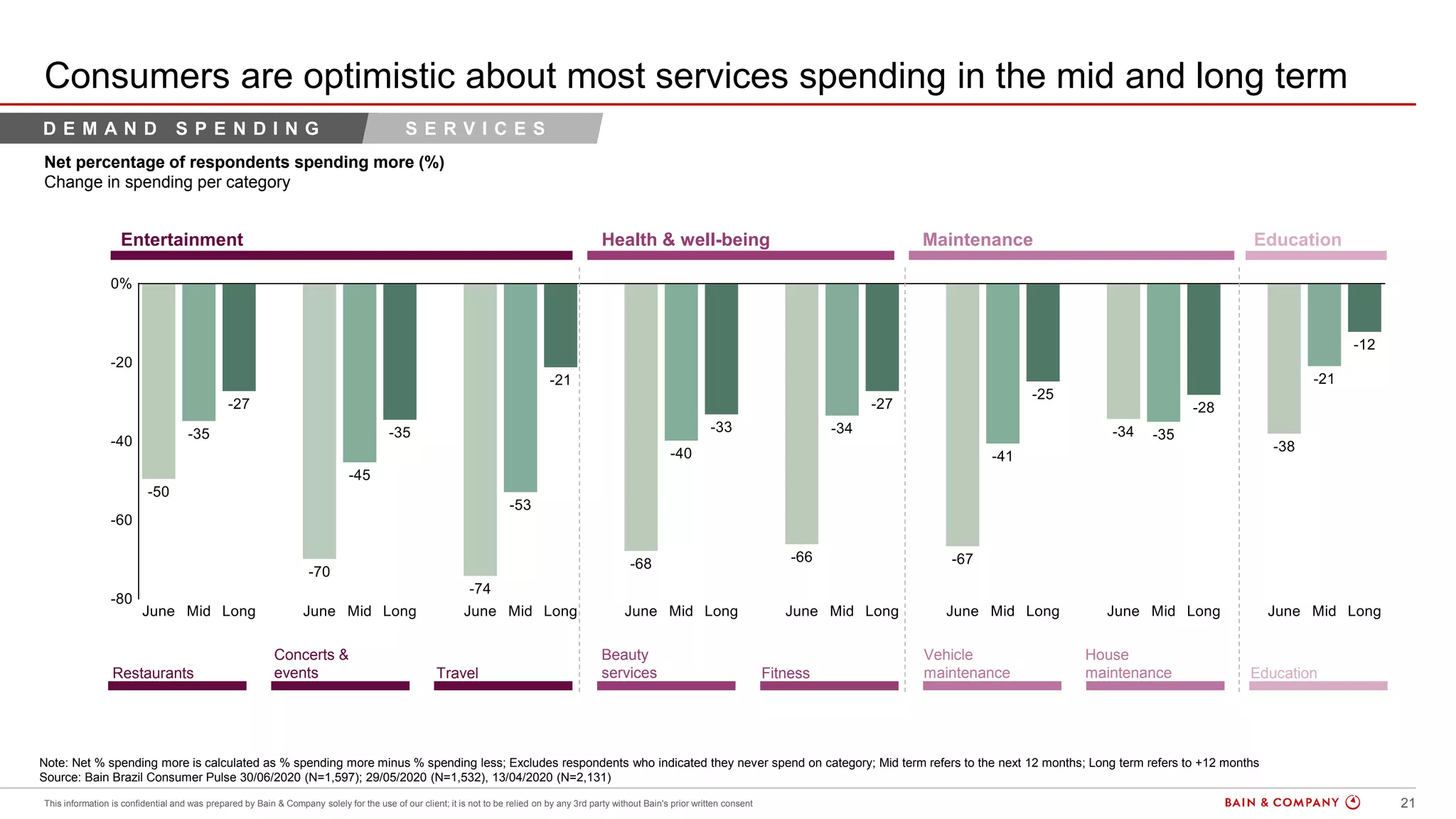

Brazilians have become more pessimistic about the duration of the pandemic, expecting it to last longer. However, expectations about the financial impact are now matching the real impact. Consumers' routines have remained stable since May, with more time spent on digital entertainment and less time working. Demand is falling compared to the start of the pandemic, with spending on essential categories expected to drop 5-25% long-term. Online spending continues to grow while offline spending declines.