Fullerton Securities recommends : Bharati Airtel Ltd - BUY

•

0 likes•69 views

Catch the latest Equity research reports from Fullerton Securities at http://www.fullertonsecurities.co.in/equity/markets/research_reports.aspx

Recommended

More Related Content

What's hot

What's hot (19)

Similar to Fullerton Securities recommends : Bharati Airtel Ltd - BUY

Similar to Fullerton Securities recommends : Bharati Airtel Ltd - BUY (20)

More from Fullerton Securities

More from Fullerton Securities (20)

Recently uploaded

Recently uploaded (20)

Fullerton Securities recommends : Bharati Airtel Ltd - BUY

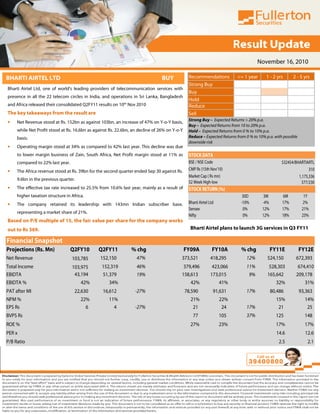

- 1. BHARTI AIRTEL LTD BUY Bharti Airtel Ltd, one of world’s leading providers of telecommunication services with presence in all the 22 telecom circles in India, and operations in Sri Lanka, Bangladesh and Africa released their consolidated Q2FY11 results on 10 The key takeaways from the result are • Net Revenue stood at Rs. 152bn as against 103bn, an increase of 47% on Y while Net Profit stood at Rs. 16.6bn as against Rs. 22.6bn, an decline of 26% on Y basis. • Operating margin stood at 34% as compared to 42% last year. This decline was due to lower margin business of Zain, South Africa, Net Profit marg compared to 22% last year. • The Africa revenue stood at Rs. 39bn for the second quarter ended Sep 30 against Rs. 9.6bn in the previous quarter. • The effective tax rate increased to 25.5% from 10.6% last year, mainly as a result of higher taxation structure in Africa. • The company retained its leadership with 143mn representing a market share of 21%. Based on P/E multiple of 15, the fair value per share for t out to Rs 369. Financial Snapshot Projections (Rs. Mn) Q2FY10 Q2FY11 Net Revenue 103,785 152,150 Total Income 103,975 152,319 EBIDTA 43,194 51,379 EBIDTA % 42% 34% PAT after MI 22,630 16,612 NPM % 22% 11% EPS Rs 6 4 BVPS Rs ROE % PER x P/B Ratio BHARTI AIRTEL LTD BUY of telecommunication services with ircles in India, and operations in Sri Lanka, Bangladesh consolidated Q2FY11 results on 10th Nov 2010 Rs. 152bn as against 103bn, an increase of 47% on Y-o-Y basis, Net Profit stood at Rs. 16.6bn as against Rs. 22.6bn, an decline of 26% on Y-o-Y Operating margin stood at 34% as compared to 42% last year. This decline was due Net Profit margin stood at 11% as The Africa revenue stood at Rs. 39bn for the second quarter ended Sep 30 against Rs. .6% last year, mainly as a result of The company retained its leadership with 143mn Indian subscriber base, , the fair value per share for the company works Bharti Airtel plans to launch 3G services in Q3 FY11 Recommendations <= 1 year Strong Buy Buy Hold Reduce Sell Strong Buy – Expected Returns > 20% p.a. Buy – Expected Returns from 10 to 20% p.a. Hold – Expected Returns from 0 % to 10% p.a. Reduce – Expected Returns from 0 % to 10% p.a. with possible downside risk Sell – Returns < 0 % BSE / NSE Code CMP Rs (15th Nov’10) Market Cap ( Rs mn) 52 Week High-low Bharti Airtel Ltd Sensex Nifty STOCK RETURN (%) STOCK DATA % chg FY09A FY10A 47% 373,521 418,295 46% 379,496 423,066 19% 158,613 173,015 42% 41% -27% 78,590 91,631 21% 22% -27% 21 24 77 105 27% 23% November 16, 2010 Bharti Airtel plans to launch 3G services in Q3 FY11 <= 1 year 1 - 2 yrs 2 - 5 yrs Expected Returns > 20% p.a. Expected Returns from 10 to 20% p.a. Expected Returns from 0 % to 10% p.a. Expected Returns from 0 % to 10% p.a. with possible 30D 3M 6M 1Y -10% -4% 17% 2% 0% 12% 17% 21% 0% 12% 18% 23% 532454/BHARTIARTL 310 1,175,336 377/230 % chg FY11E FY12E 12% 524,150 672,393 11% 528,303 674,410 9% 165,642 209,178 32% 31% 17% 80,486 93,363 15% 14% 17% 21 25 37% 125 148 17% 17% 14.6 12.6 2.5 2.1

- 2. OTHER HIGHLIGHTS The Q2FY11 was the first full quarter reflecting the African operations; the first quarter incorporated only 23 days of the Africa operations effective from June 8, 2010. The revenues from mobile services represented 83.4% of the total revenues, while non-voice revenue contributed to approximately 14.2 and Net Profit margins stood lower at 34% and 11% respectively from 42% and 22% in last year operating expenses and higher access & interconnection charges in African business in India declined by 20% to Rs. 202 a month while the Minutes of usage increased just 1% to 454. ARPU in Africa fell 1% from the previous quarter to $7.40. For Q2 FY11, Bharti Airtel Even as the Mobile Number Portability is expected to be a reality soon, high quality should help the company maintain its market share. Bharti Airtel plans to launch 3G services in India i will enable it to augment its revenues by offering various data services. It provides a great potential as current broadband subscriber base is just around 10.8mn. Also, the company is in the process of implementing its low cost model in thei African operations. Bharti Airtel has already signed IT and customer service outsourcing deals and is having negotiations with other operators for network sharing agreements. These initiatives will Bharti Airtel to increase their subscriber base by offering competitive tariffs Based on a P/E multiple of 15, the fair value per share for t We recommend a ‘BUY’ rating on the stock. Financial Analysis and Projections Particulars (Rs Mn) Net Revenue Other Income Total Income Operating Expenditure Depreciation EBIT EBIT Margin (%) Interest Profit Before Tax Less: Tax PAT after MI PAT Margin (%) ROE (%) EPS (Rs) BVPS (Rs) Valuation Ratios (x) P/E P/B the African operations; the first quarter incorporated only 23 days of the evenues from mobile services represented 83.4% of the total revenues, voice revenue contributed to approximately 14.2% of the total revenues for the quarter. The Operating profit at 34% and 11% respectively from 42% and 22% in last year mainly due to high and higher access & interconnection charges in African business. The average revenue per user (ARPU) Minutes of usage increased just 1% to 454. ARPU in Africa fell 1% from the previous quarter to $7.40. For Q2 FY11, Bharti Airtel’s churn rate was 5.9% as against 5.8% in Q1 FY11. is expected to be a reality soon, high brand recall, network coverage and service maintain its market share. Bharti Airtel plans to launch 3G services in India in Q3 FY11. This revenues by offering various data services. It provides a great potential as current broadband the company is in the process of implementing its low cost model in thei African operations. Bharti Airtel has already signed IT and customer service outsourcing deals and is having negotiations . These initiatives will improve the margins going ahead and enable to increase their subscriber base by offering competitive tariffs. , the fair value per share for the company works out to Rs 369. Financial Analysis and Projections Particulars (Rs Mn) FY08A FY09A FY10A Net Revenue 270,122 373,521 418,295 Other Income 3,600 5,975 4,771 Total Income 273,723 379,496 423,066 Operating Expenditure 156,422 220,883 250,051 Depreciation 38,102 49,639 65,544 79,198 108,974 107,471 EBIT Margin (%) 29% 29% 26% Interest 6,083 23,064 1,483 Profit Before Tax 73,115 85,910 108,954 Less: Tax 8,161 5,468 15,339 PAT after MI 63,954 78,590 91,631 PAT Margin (%) 24% 21% 22% ROE (%) 29% 27% 23% EPS (Rs) 17 21 24 BVPS (Rs) 57 77 105 Valuation Ratios (x) November 16, 2010 the African operations; the first quarter incorporated only 23 days of the evenues from mobile services represented 83.4% of the total revenues, Operating profit high er (ARPU) Minutes of usage increased just 1% to 454. ARPU in Africa fell 1% brand recall, network coverage and service Q3 FY11. This revenues by offering various data services. It provides a great potential as current broadband the company is in the process of implementing its low cost model in their African operations. Bharti Airtel has already signed IT and customer service outsourcing deals and is having negotiations improve the margins going ahead and enable Overall customer base of the company in 19 countries stands at 194.8mn Indian market share stood at 21% African operation provides significant growth penetration with penetration rate of 40% FY11E FY12E 524,150 672,393 4,153 2,017 528,303 674,410 362,662 465,232 61,488 68,752 104,153 140,427 20% 21% 12,142 33,695 92,011 106,731 10,063 11,673 80,486 93,363 15% 14% 17% 17% 21 25 125 148 FY11E FY12E 14.6 12.6 2.5 2.1