Accounting involves recording, classifying, summarizing, analyzing, and reporting financial transactions to provide insights into an organization's financial health and performance for decision-making and compliance and easy ..

Account

• It isa unit of information

that represents business records.

• There are five types of

accounts: Asset, Liability,

Equity, Revenue and Expense.

3.

Accounting

• It isconcerned with the use of which the

records are put, their analysis and

interpretation.

• It is the process of recording business

activities that make changes to accounts.

• Sales of products, Revenue from services

earned, Buying products and/or services and

so on.

4.

Attributes of Accounting

•It is the art of recording business transactions.

• It is the art of classifying business

transactions.

• The transactions or events of a business must

be recorded in monetary terms.

• It is the art of summarizing financial

transactions.

• The results should be

communicated to users.

5.

Functions

• Systematic recordof business transactions.

• Protecting the property of business.

• Communicating results to users.

• Compliance with legal requirements.

6.

Users of Accounting

Information

•Owners

• Creditors (Suppliers)

• Investors

• Employees

• Government

• Public

• Research Scholars / Agencies

• Managers

Advantages

• Replacement ofMemory

• Evidence in court

• Tax purpose

• Comparative study

• Sale of business

• Assistance to the insolvent

• For various parties

9.

Limitations

• Records onlymonetary transactions

• Effect of price level changes not considered

• No realistic information

• Personal bias of accountant affects the

accounting statements

• Permits alternative treatments (LIFO,

FIFO)

• No real test for managerial

performance

10.

Accounting Terminology

• Business:An organization created with the objective of

making a profit from the sale of goods or services.

Book keeping: The act of systematically recording the

financial transactions affecting a business.

Book Value: The net amount (original value plus or minus

•

•

any adjustments such as depreciation) showed in the

accounts for an asset, liability, or owners' equity item.

Calendar Year: An entity's reporting year, covering 12

months.

•

• Transactions: Exchange of goods or services between

businesses or individuals. Can also be other events having

an economic impact on a business.

11.

Basis of Accounting

.Cashbasis

–Actual cash receipts and

payments are recorded.

–Credit transactions are not recorded.

12.

Basis of Accounting

•Accrual basis

– The income whether received or not but has been

earned or accrued during the period forms

part of the total income of the period.

– The firm has taken benefit of a particular service,

but has not paid within that period, the

expenses will relates to the period in which

the service has been utilized and not to

the period in which payment for it is made.

System of Accounting

SingleEntry System: This system has no

complete record of business transactions

done during a specified period.

• Double Entry System: One account is given

debit while the other account is given credit

with an equal amount.

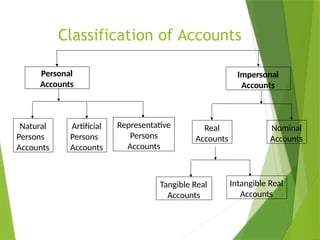

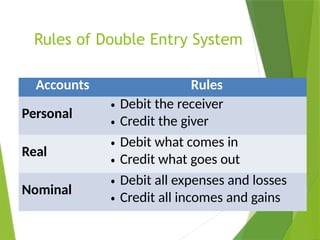

Rules of DoubleEntry System

Accounts Rules

Personal

• Debit the receiver

• Credit the giver

Real

• Debit what comes in

• Credit what goes out

Nominal

• Debit all expenses and losses

• Credit all incomes and gains