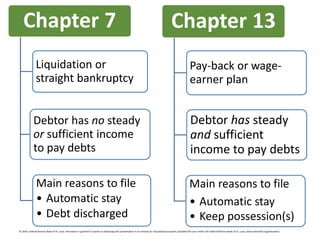

Bankruptcy is a legal process that provides relief for individuals and businesses who cannot repay their debts. It allows debtors to address debt problems through federal law and court proceedings. There are different types of bankruptcy that can provide either a fresh start or fair treatment of debts depending on the situation. The most common types are Chapter 7, which is for liquidation of debts, and Chapter 13, which sets up a repayment plan over time. Both chapters involve credit counseling, filing a petition, assignment of a trustee, and other standardized procedures to discharge debts or set up a repayment schedule.