Recommended

PPTX

Commercial Banking system in India , Retail banking product.

PPTX

Integration of erp in banking sector

PPT

Econ315 Money and Banking: Learning Unit 19: Banking Industry and Regulation

PDF

Learningunit19 2016-160211163050

PPTX

Origin, history and types of banking system

DOCX

UNIT 1 - BANKING THEORY LAW AND PRACTICE.docx

PPTX

bankingservices-240301094157-96d1e344.pptx

PPTX

Tally.ERP 9 for Windows With Crack Free Download 2025

PDF

Vivaldi Web Browser 6.8.3381.50 Crack Free Download 2025

PDF

Kaspersky Lab Products Remover 1.0.5014.0 Crack Free

PDF

Adobe Substance 3D Designer 14.0.0.8074 Crack Free

PDF

Brave Browser 1.68.134 Crack free download 2025

PDF

GraphPad Prism 10.3.0.507 Crack Free Download

PDF

Kaspersky Lab Products Remover 1.0.5014.0 Crack Free

PDF

IObit Driver Booster Pro Crack Version 2025?

PDF

Minitab Free Download crack (Latest 2025)

PDF

ExplorerPatcher 22621.4317.67.1 Download

PDF

GraphPad Prism 10.4.2.633 Free Download

PDF

Apple Logic Pro X for MacOS Free Download

PDF

Brave Browser 1.68.134 Crack free download 2025

PDF

Brave Browser 1.68.134 Crack free download 2025

PDF

GraphPad Prism 10.3.0.507 Crack Free Download

PDF

Software Ideas Modeler Ultimate Download

PDF

Dehancer Pro 7.2.0 Beta 2 for Adobe Premiere

PPTX

Brave Browser 1.68.134 Crack free download 2025

PPTX

Vivaldi Web Browser 6.8.3381.50 Crack Free Download 2025

PPTX

ExplorerPatcher Crack Free Download 2025

PDF

Adobe Acrobat Pro DC Download Latest 2025

PDF

Using-pension-savings-to-support-home-ownership.pdf

PPTX

REVIEWER-3rd-quarter-exam-mathematics.pptx

More Related Content

PPTX

Commercial Banking system in India , Retail banking product.

PPTX

Integration of erp in banking sector

PPT

Econ315 Money and Banking: Learning Unit 19: Banking Industry and Regulation

PDF

Learningunit19 2016-160211163050

PPTX

Origin, history and types of banking system

DOCX

UNIT 1 - BANKING THEORY LAW AND PRACTICE.docx

PPTX

bankingservices-240301094157-96d1e344.pptx

PPTX

Tally.ERP 9 for Windows With Crack Free Download 2025

Similar to Banking_Fundamentals_Module_1_2_3_US_Fresh.pptx

PDF

Vivaldi Web Browser 6.8.3381.50 Crack Free Download 2025

PDF

Kaspersky Lab Products Remover 1.0.5014.0 Crack Free

PDF

Adobe Substance 3D Designer 14.0.0.8074 Crack Free

PDF

Brave Browser 1.68.134 Crack free download 2025

PDF

GraphPad Prism 10.3.0.507 Crack Free Download

PDF

Kaspersky Lab Products Remover 1.0.5014.0 Crack Free

PDF

IObit Driver Booster Pro Crack Version 2025?

PDF

Minitab Free Download crack (Latest 2025)

PDF

ExplorerPatcher 22621.4317.67.1 Download

PDF

GraphPad Prism 10.4.2.633 Free Download

PDF

Apple Logic Pro X for MacOS Free Download

PDF

Brave Browser 1.68.134 Crack free download 2025

PDF

Brave Browser 1.68.134 Crack free download 2025

PDF

GraphPad Prism 10.3.0.507 Crack Free Download

PDF

Software Ideas Modeler Ultimate Download

PDF

Dehancer Pro 7.2.0 Beta 2 for Adobe Premiere

PPTX

Brave Browser 1.68.134 Crack free download 2025

PPTX

Vivaldi Web Browser 6.8.3381.50 Crack Free Download 2025

PPTX

ExplorerPatcher Crack Free Download 2025

PDF

Adobe Acrobat Pro DC Download Latest 2025

Recently uploaded

PDF

Using-pension-savings-to-support-home-ownership.pdf

PPTX

REVIEWER-3rd-quarter-exam-mathematics.pptx

PDF

How To Buy Verified Cash App Accounts - Secure Your Transactions.pdf

PDF

OIL CHECK 500 Portable - Air Quality Monitoring System

PDF

BendelPuertoRicoCubaGuyanaVenezuelaPetroleumRefineryPetrochemicalPetroAgroInd...

PDF

enterprise software is not dead and here is why

PDF

A Comprehensive Guide to Buy Verified PayPal Accounts in the US.pdf

PDF

Camil Institutional Presentation_Jan26.pdf

PPTX

Finding Product-Market Fit in the Age of AI

PDF

Top 1 0 Websites to Buy Verified Transfer Remitly Accounts ....pdf

PDF

How Unlock Buy Verified Cash App Accounts?

DOCX

How To Buy LinkedIn Accounts – 100% PVA, Aged & Bulk..docx

DOCX

Buy Old Gmail Accounts USA – Instant Delivery Bulk Gmail.docx

PDF

Equinox Gold - January Investor Presentation.pdf

PPTX

Agentic AI vs Genetic AI: Key Differences, Use Cases & Future Trends | Comple...

PDF

Buy Proton Mail Accounts _ Secure Email Accounts In 2026.pdf

PDF

_Top 7 Tips for Buying Verified PayPal Accounts.pdf

DOCX

How to Buy Verified OnlyFans Accounts Work in 2026.docx

PDF

The threat to financial insitutions of quantum computing breaking all encrypt...

PDF

Benefits Quarterly, Vol. 37, Fourth Quarter 2021.pdf

Banking_Fundamentals_Module_1_2_3_US_Fresh.pptx 1. Introduction to Banking & Financial

Services

• Duration: 1 hour

• Objective: Understand the role of banks in the

US financial system

2. What is a Bank?

• A financial intermediary

• Accepts deposits, provides loans

• Facilitates payments and credit

3. Why Banks Matter

• Allocate capital

• Provide safety and liquidity

• Enable economic activity

• Trust-based system

4. Core Banking Functions

• Intermediation (savers to borrowers)

• Liquidity Provision

• Risk Transformation

• Payments & Settlements

5. Types of Banks (US Context)

• Commercial Banks

• Savings and Loan Associations

• Credit Unions

• Investment Banks

• Neo/Online Banks

6. Types of Bank Customers

• Individuals (Retail)

• Small businesses / SMEs

• Corporates & Institutions

• Government and public entities

7. US Banking Structure

• Federal Reserve: Central Bank

• FDIC: Deposit Insurance

• OCC: Regulator for national banks

• CFPB: Consumer Protection

8. 9. How Tech Powers Banking

• Core Banking Systems

• Channel Applications (Mobile/Internet)

• Payment Gateways

• Regulatory Compliance Engines

10. Quiz & Wrap-Up

• What is the role of the FDIC?

• Name two types of banks.

• Who are retail customers?

• What is liquidity transformation?

• What system powers online banking?

11. Lines of Business in Banking

• Duration: 1 hour

• Objective: Understand the key business

segments in banks

12. What is a Line of Business?

• A customer or product-segmented service

area

• Independent P&L responsibilities

13. Retail Banking

• Products: Savings, Checking, Loans, Credit

Cards, Mortgages

• Channels: Branch, Mobile, ATM

• Volume-driven, low value per transaction

14. Corporate / Wholesale Banking

• Customers: SMEs, Large Corporates

• Products: Working Capital, Cash Management,

Trade Finance, Escrow

• High value, relationship-driven

15. Capital Markets / Investment

Banking

• Services: Underwriting, IPOs, Trading

• Revenue from fees and market activity

16. Private Banking & Wealth

• High Net Worth Individuals (HNWIs)

• Personalized financial services, estate planning

17. Treasury & ALM

• Managing liquidity, funding, FX risk

• Interbank borrowing/lending

18. Software Mapping to Lines of

Business

• Retail: Core Banking, LOS, CRM

• Corp: CMS, Trade Finance, Treasury Mgmt

• Markets: Deal Booking, Risk Engines,

Settlements

19. Data & System Segregation

• Customer Segments

• Product Catalogues

• Ledger Structures

20. Recap & Questions

• Match the following:

• Working capital → ?

• Credit card → ?

• IPO → ?

• Why do banks split into lines of business?

21. Retail Banking Deep Dive

• Duration: 1.5 hours

• Objective: Explore retail banking products,

lifecycle, and system behavior

22. Retail Customer Journey

• Onboarding → Account Opening → Product

Usage → Closure

• Touchpoints: Branch, Mobile, Online, Call

Center

23. Savings & Checking Accounts

• Features: Interest-bearing, withdrawals,

minimum balance

• Transaction Types: Deposits, Withdrawals,

Auto-debits, Transfers

24. Retail Loans

• Types: Personal, Auto, Mortgage, Education

• Lifecycle: Origination → Disbursement →

Repayment → Closure

• EMIs, Interest Accrual, Amortization

25. Cards & Payments

• Credit Cards vs Debit Cards

• Authorization, Posting, Settlement

• Rewards, Fees, Interest

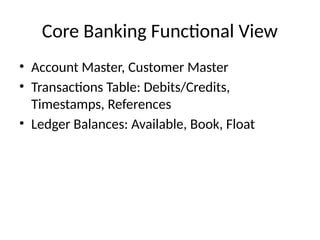

26. 27. 28. Core Banking Functional View

• Account Master, Customer Master

• Transactions Table: Debits/Credits,

Timestamps, References

• Ledger Balances: Available, Book, Float

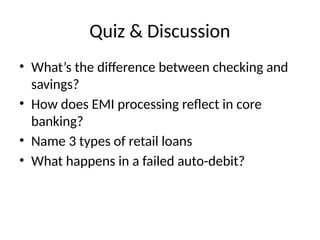

29. 30. Quiz & Discussion

• What’s the difference between checking and

savings?

• How does EMI processing reflect in core

banking?

• Name 3 types of retail loans

• What happens in a failed auto-debit?