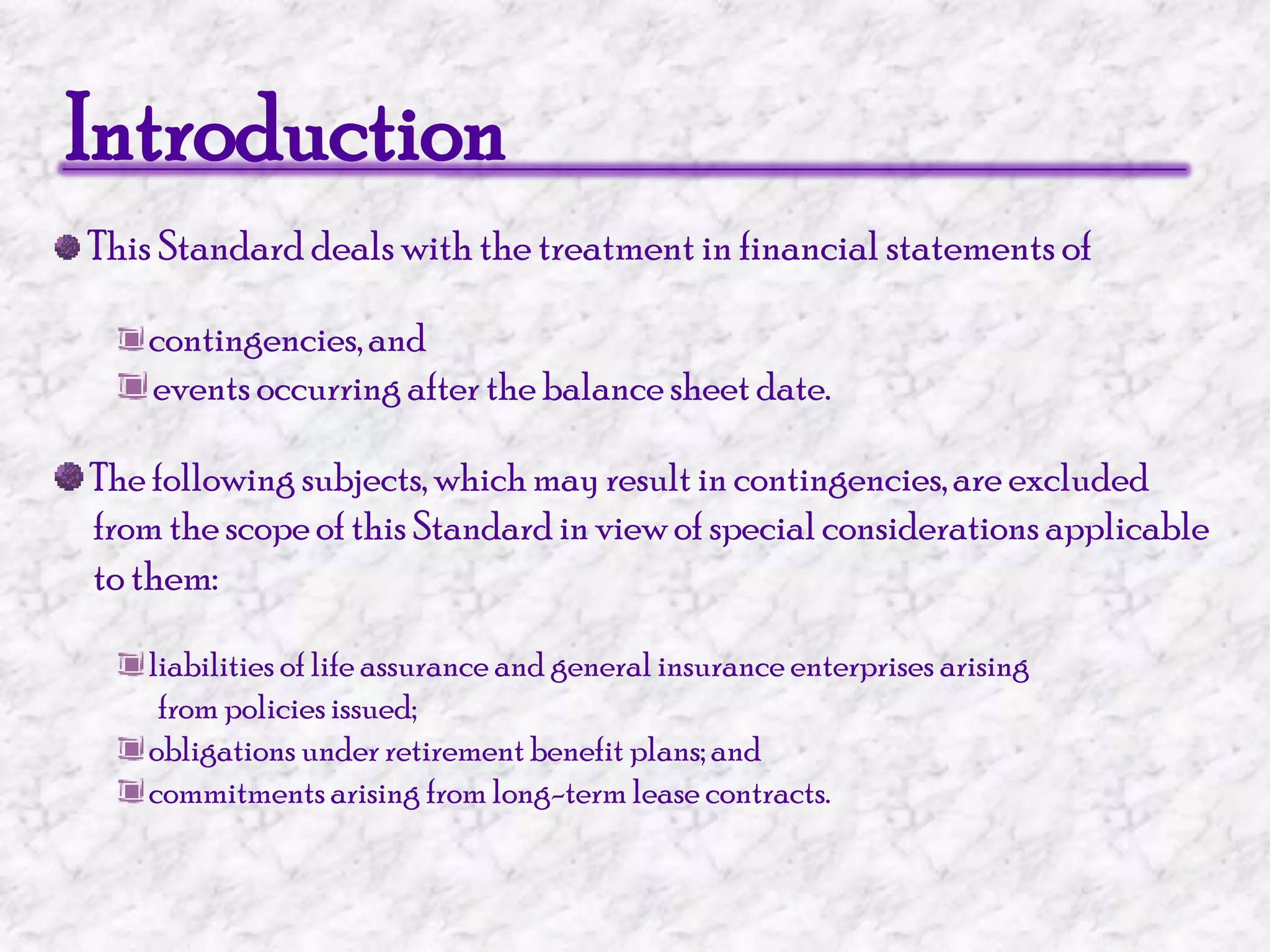

This document summarizes accounting standards for contingencies and events occurring after the balance sheet date. It discusses that contingencies are uncertain future outcomes that may result in gains or losses. Contingent losses should be accounted for if the loss is probable and reasonably estimable. Contingent gains are not recognized. Events after the balance sheet date are adjusted for if they provide evidence of conditions existing at the balance sheet date. Otherwise, significant events are disclosed. The document outlines principles for accounting treatment of contingencies, determining amounts, and disclosure requirements.