This document provides an introduction to key accounting concepts:

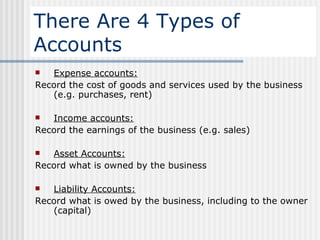

1. It defines accounting as recording financial information about resources owned (assets), owed (liabilities), and equity. It outlines the different types of accountants and their qualifications.

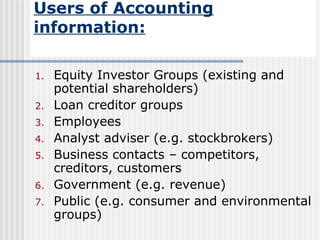

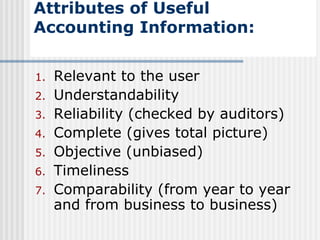

2. Accounting information is used by various stakeholders like investors, creditors, employees, and government agencies. Useful attributes of accounting data include relevance, understandability, reliability, completeness, objectivity, timeliness, and comparability.

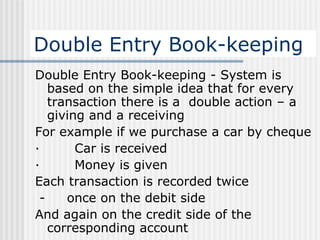

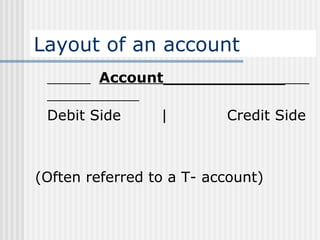

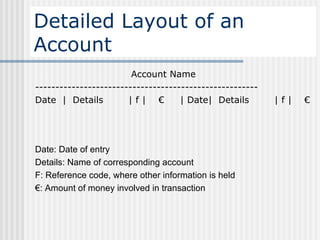

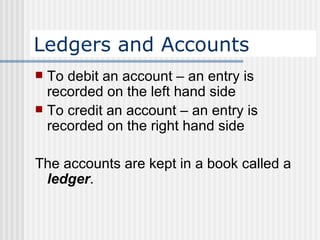

3. The document introduces double-entry bookkeeping where every transaction has two equal entries - a debit and a credit. It outlines the layout of T-accounts to record transactions.