Downloaded 45 times

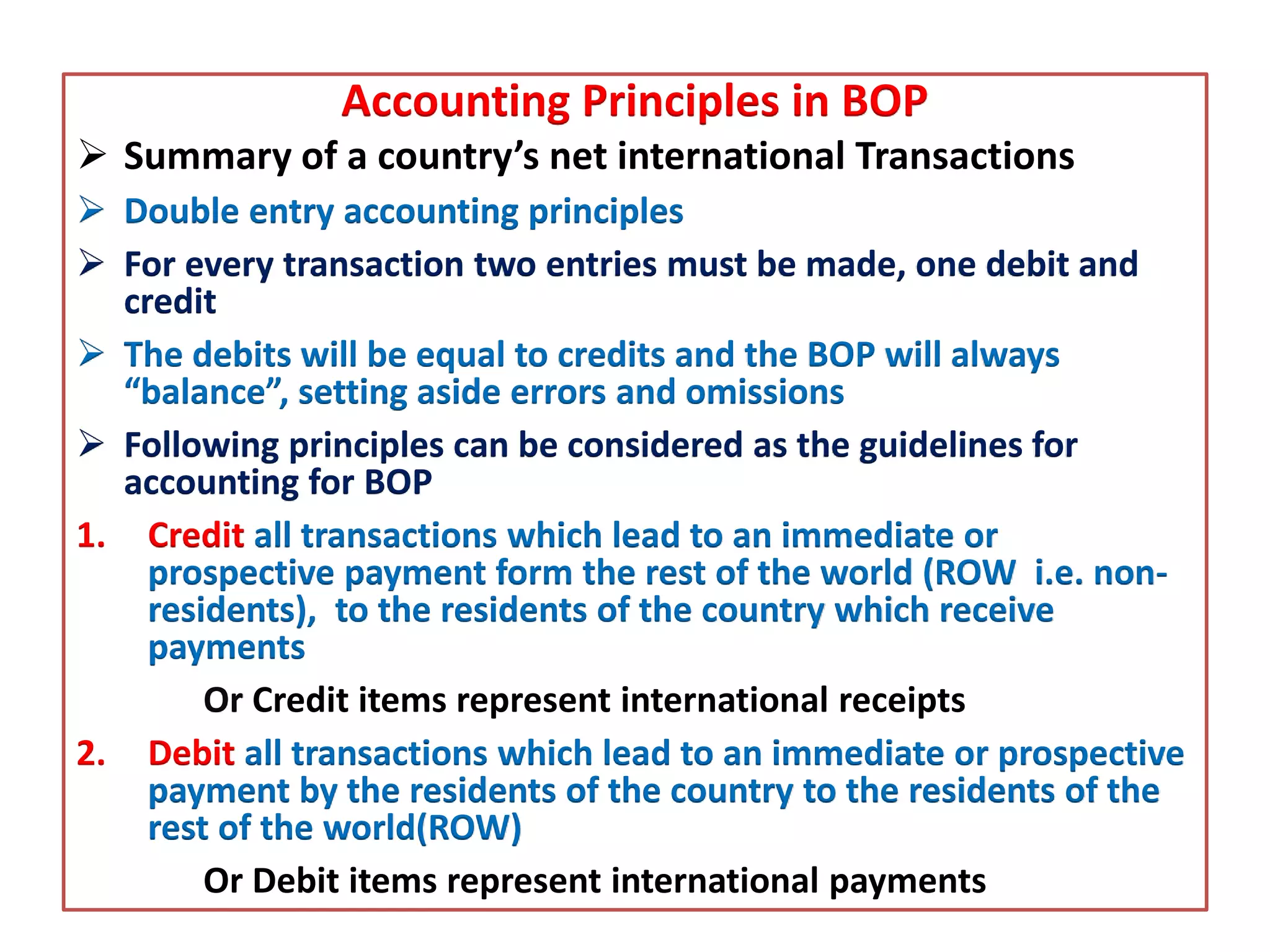

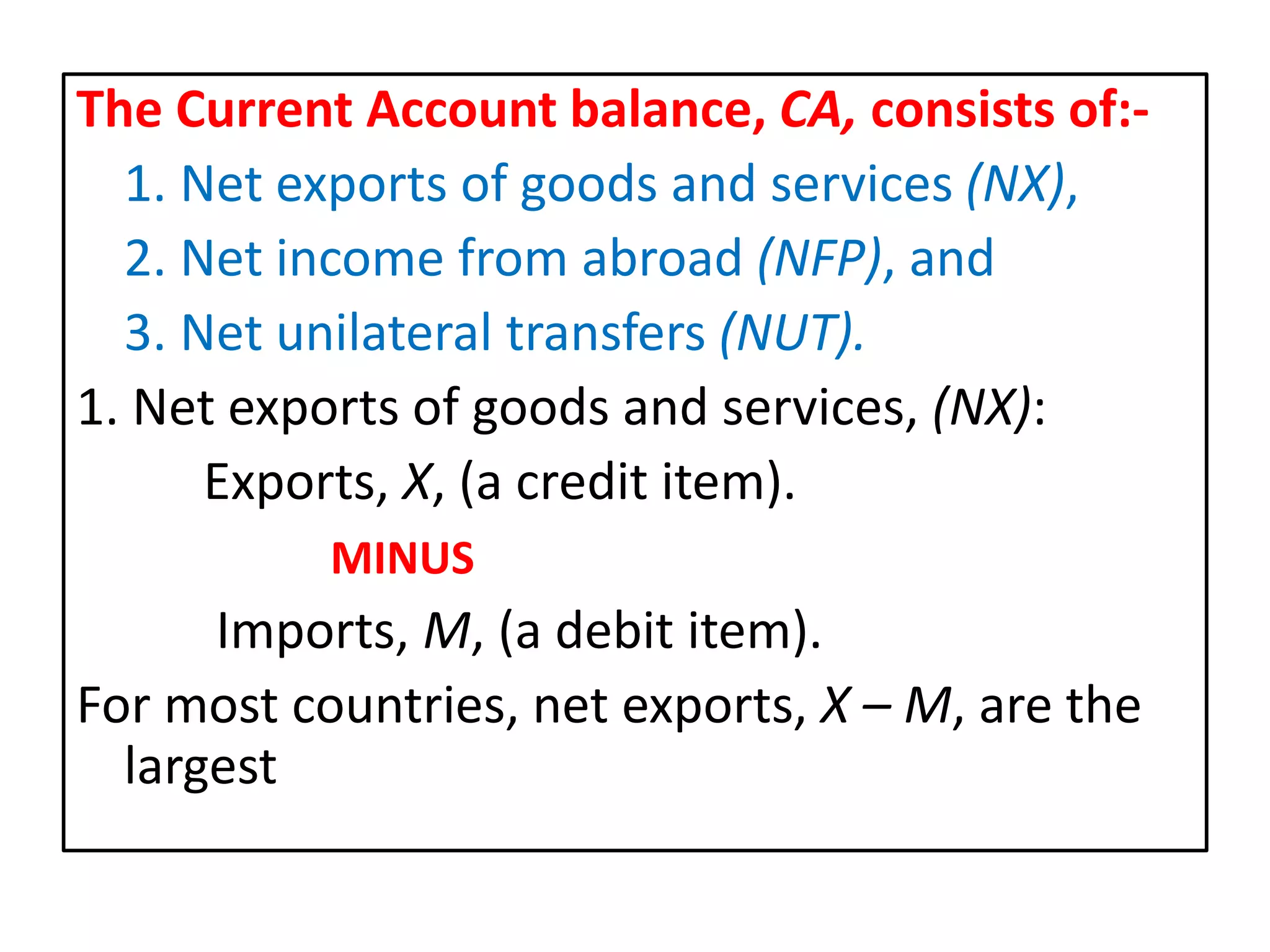

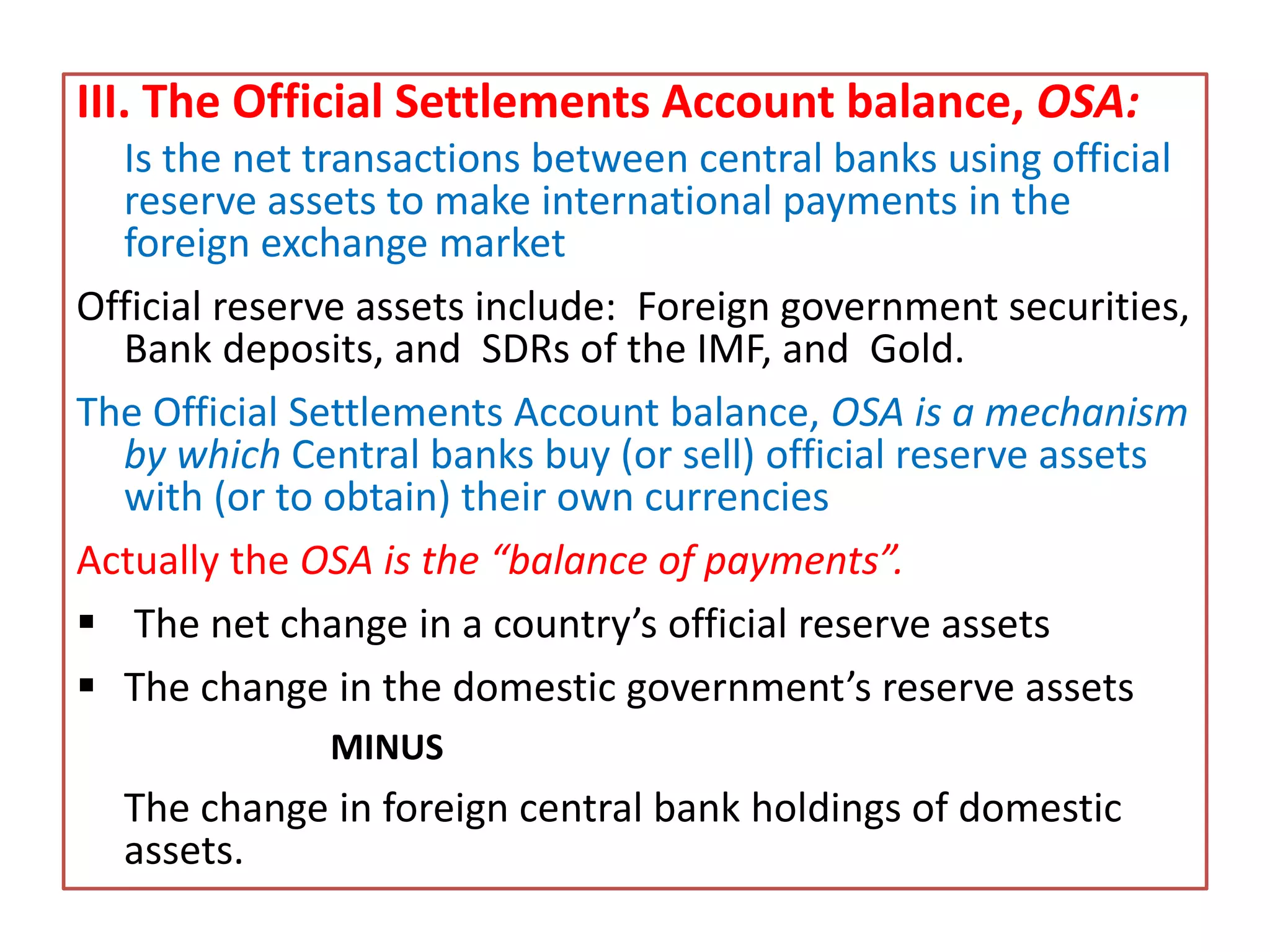

This document discusses accounting principles for balance of payments (BOP) accounting. It outlines that BOP accounting follows double-entry bookkeeping, with debits equal to credits. Transactions are recorded based on whether they represent payments from or receipts to a country. Exports are credited on the current account and debited on the capital account. Imports are debited on the current account and credited on the capital account. The BOP consists of the current account balance, capital and financial account balance, and official settlements account balance. Valuation and timing of recording transactions can pose challenges to uniform BOP accounting practices.

![Balance of payments[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/balanceofpayments1-230405055631-4f2f56b6-thumbnail.jpg?width=640&height=640&fit=bounds)