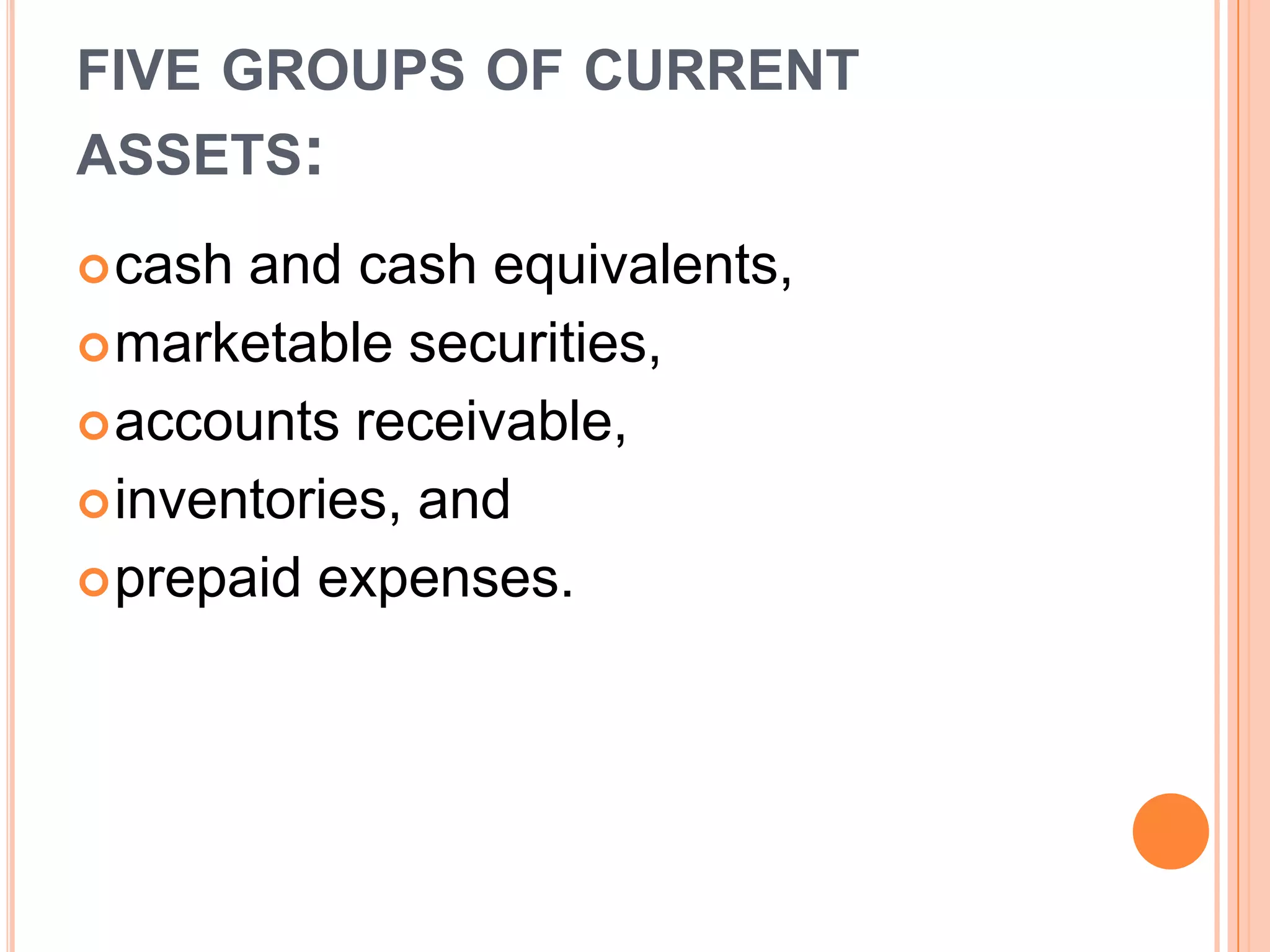

Current assets include cash, marketable securities, accounts receivable, inventories, and prepaid expenses. These are assets that can reasonably be expected to be converted to cash within one year. Accounts receivable represents amounts owed by customers from sales on credit. Companies use different inventory costing methods like FIFO, LIFO, and average costing. Prepaid expenses are assets representing expenses paid in advance to be recognized later.