Download to read offline

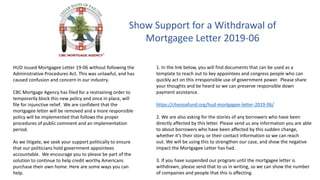

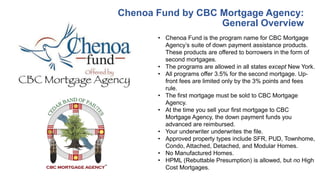

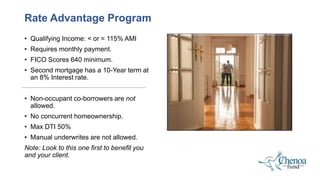

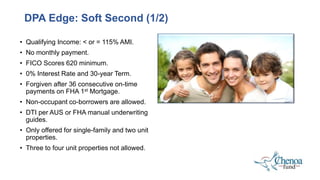

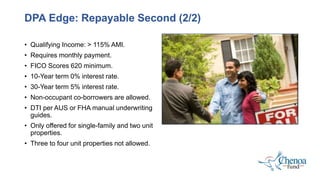

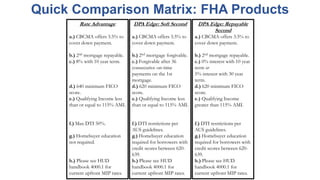

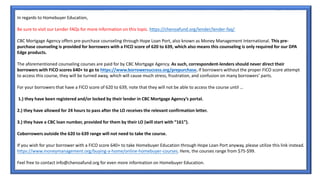

The document outlines the legal challenges against HUD's mortgagee letter 2019-06, which CBC Mortgage Agency argues was issued unlawfully and has caused confusion in the industry. CBC has filed for a restraining order to block the policy and seeks political support to ensure responsible down payment assistance policies are implemented. Additionally, the document provides details on CBC's Chenoa Fund and the various FHA products offered for down payment assistance, as well as important contact information and document requirements for lenders.