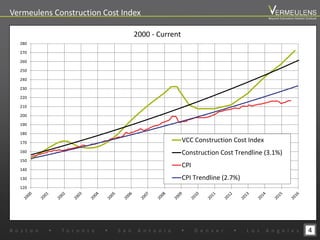

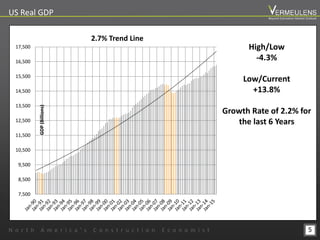

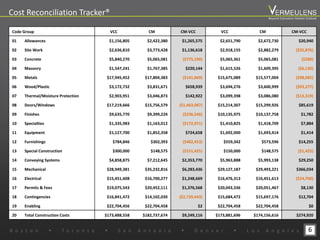

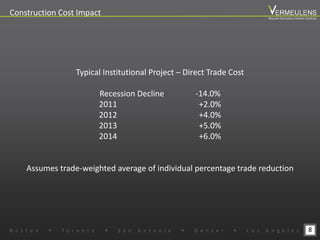

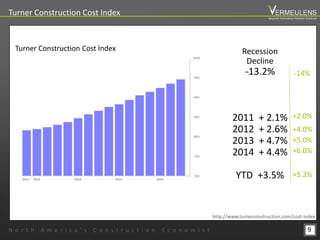

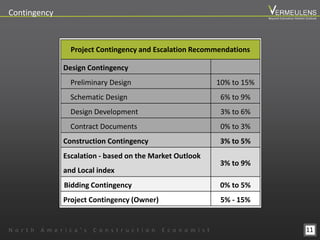

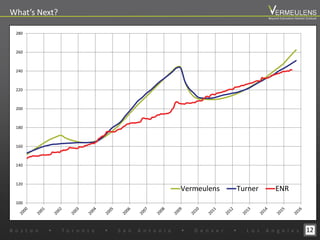

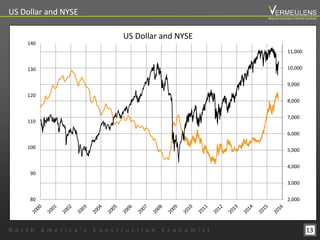

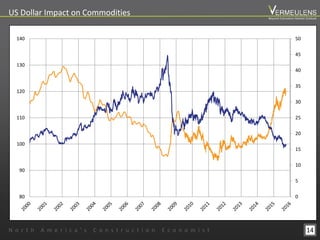

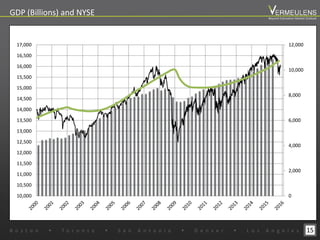

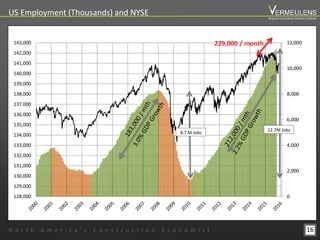

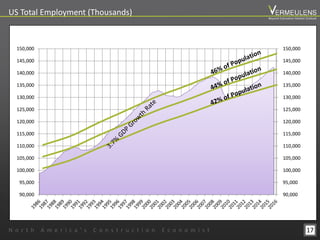

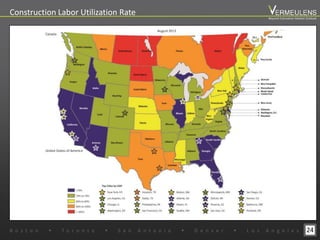

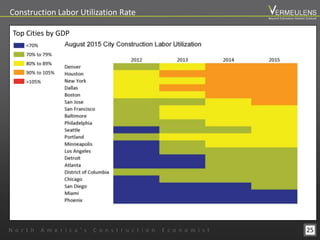

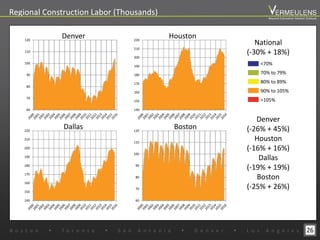

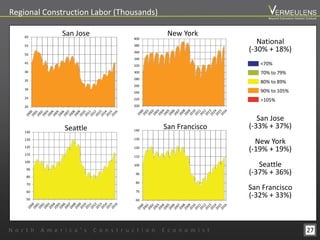

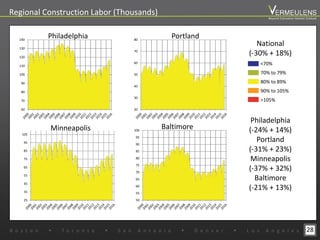

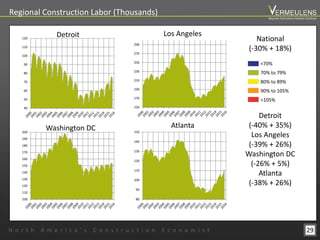

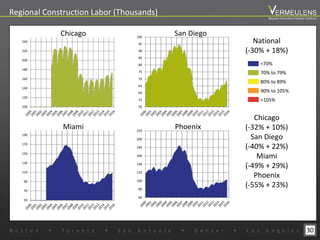

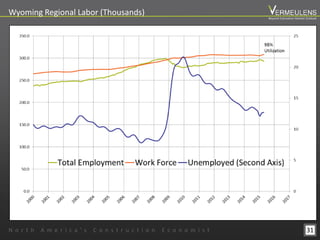

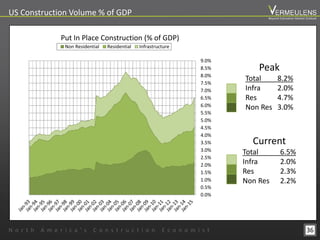

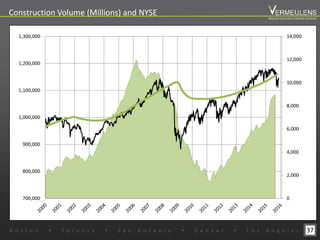

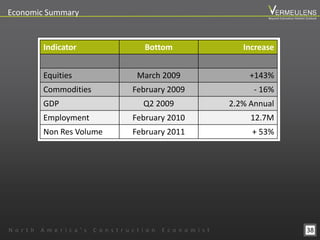

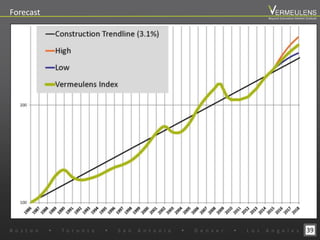

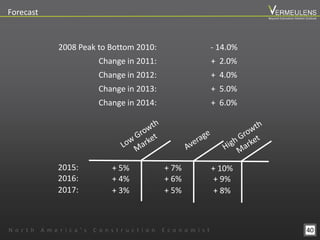

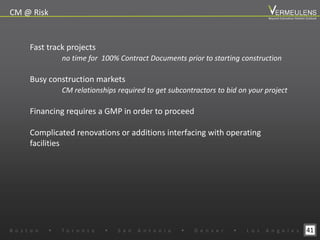

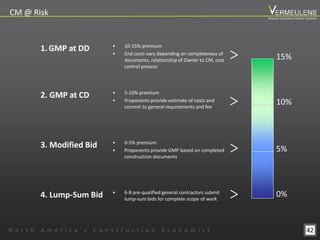

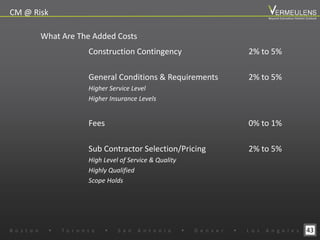

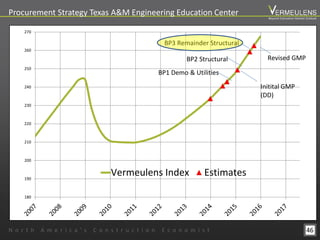

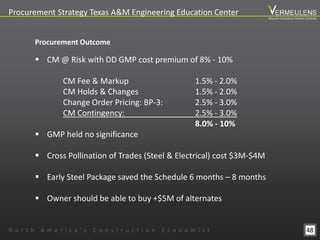

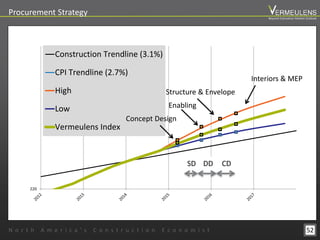

The document presents a comprehensive analysis of the construction cost forecasting and market trends in North America since 1972, highlighting key metrics, economic impacts, and procurement strategies. It includes various data points such as construction cost indices, GDP trends, and recommendations for project contingencies and escalation strategies. The insights aim to assist industry professionals in understanding current market conditions and making informed procurement decisions.

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)