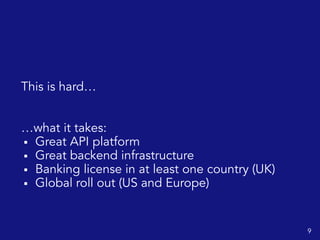

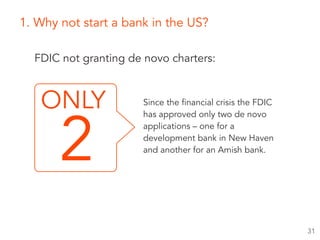

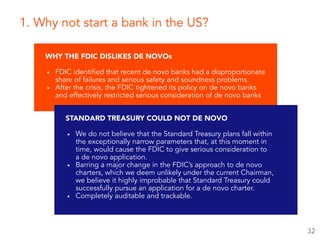

The document outlines plans to launch a wholesale banking platform called Standard Treasury that will provide banking services via API to fintech companies and power the next generation of financial applications. It details the team's experience in banking technology, regulatory work completed in the UK and US, product roadmap, and financial projections showing an $8.99M series A round will fund the application and launch process. Risks are acknowledged but mitigation strategies are proposed to address challenges in obtaining a banking license, timeline, and hiring.