01 Ebury

02 Potentialimplication of Brexit on Ebury's business model

03 Belgium as the first choice for Brexit plan

Agenda2

+44 (0) 20 3872 6670 | info@ebury.com | ebury.com

3.

Ebury thrives tobe the GTA for SMEs3

Working with

24,000+ businesses

& organisations

13 Countries, 15

Offices. London,

Manchester, Madrid,

Málaga, Lisbon,

Amsterdam, Brussels,

Zurich, Paris,

Dusseldorf, Athens,

Warsaw, Milan, Toronto

and Dubai

Traded $8.2bn in foreign

exchange in the last 12

months

Backed by well-known

and respected technology

investors

Direct “SUPE” SWIFT

member and SWIFT gpi

member.

Over 20,000 transactions

per month. Capability

in over 110 currencies.

Delivered to 214

jurisdictions.

Ebury is one of Europe’s fastest-growing fintech companies,

providing FX liquidity, volatility risk management, international payments

and trade finance to SME’s.

+44 (0) 20 3872 6670 | info@ebury.com | ebury.com

4.

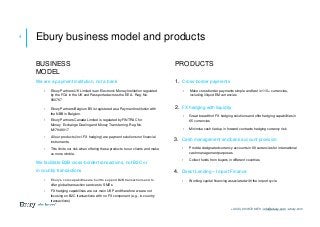

We are apayment institution, not a bank

• Ebury Partners UK Limited is an Electronic Money Institution regulated

by the FCA in the UK and Passported across the EEA. Reg. No.

900797

• Ebury Partners Belgium BV is registered as a Payment Institution with

the NBB in Belgium.

• Ebury Partners Canada Limited is regulated by FINTRAC for

Money Exchange Dealing and Money Transferring. Reg No.

M17949017

• All our products (incl. FX hedging) are payment solutions not financial

instruments.

• This limits our risk when offering these products to our clients and make

us more nimble.

We facilitate B2B cross-border transactions, not B2C or

in-country transactions

• Ebury’s core capabilities are built to support B2B transactions and to

offer global transaction services to SMEs

• FX hedging capabilities are our main USP and therefore we are not

focusing on B2C transactions with no FX component (e.g., in-country

transactions)

1. Cross-border payments

• Make cross-border payments simple and fast in 110+ currencies,

including illiquid EM currencies

2. FX hedging with liquidity

• Great breadth of FX hedging solutions and offer hedging capabilities in

65 currencies

• Minimise cash tied up in forward contracts hedging currency risk

3. Cash management and bank account provision

• Provide designated currency accounts in 68 currencies for international

cash management purposes

• Collect funds from buyers in different countries

4. Direct Lending – Import Finance

• Working capital financing associated with the import cycle

4 Ebury business model and products

PRODUCTSBUSINESS

MODEL

+44 (0) 20 3872 6670 | info@ebury.com | ebury.com

5.

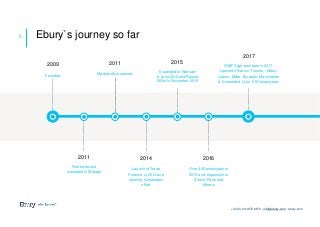

Ebury`s journey sofar5

2014

Launch of Trade

Finance in 2014 and

opening Amsterdam

office

+44 (0) 20 3872 6670 | info@ebury.com | ebury.com

2009

Founded

2011

Madrid office opened

2011

First trade and

expanded to Málaga

2016

Over 400 employees in

2016 and expansion to

Zurich, Paris and

Athens

2015

Expanded to Warsaw

in June 2015 and Raised

$83m in November 2015

2017

SWIFT gpi members in 2017.

Opened offices in Toronto, Dubai,

Lisbon, Milan, Brussels, Manchester

& Dusseldorf. Over 550 employees.

6.

Brexit implications -business model @ risk

1 Regulation

• Risk of potentially losing Ebury’s passporting rights

• Uncertainty of access to the single market resources based on the changing bilateral agreements

between UK and the EU member states

• Potential negative impact on the operational stability through regulatory changes in the UK after EU

separation

2 Risk

• Funding needs due to sharp market move

• Credit worthiness of UK importers

• Credit worthiness of underlying clients

6

7.

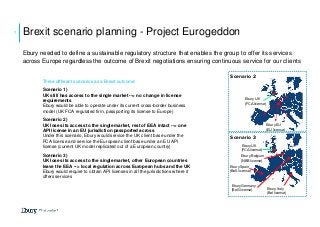

Brexit scenario planning- Project Eurogeddon7

Ebury needed to define a sustainable regulatory structure that enables the group to offer its services

across Europe regardless the outcome of Brexit negotiations ensuring continuous service for our clients

Three different scenarios as a Brexit outcome:

Scenario 1)

UK still has access to the single market --> no change in license

requirements

Ebury would be able to operate under its current cross-border business

model (UK FCA regulated firm, passporting its license to Europe)

Scenario 2)

UK loses its access to the single market, rest of EEA intact --> one

API license in an EU jurisdiction passported across

Under this scenario, Ebury would service the UK client base under the

FCA license and service the European client base under an EU API

license (current UK model replicated out of a European country)

Scenario 3)

UK loses its access to the single market, other European countries

leave the EEA --> local regulation across European hubs and the UK

Ebury would require to obtain API licenses in all the jurisdictions where it

offers services

Ebury UK

(FCA license)

Ebury EU

(EU license)

Ebury UK

(FCA license)

Ebury Belgium

(NBB license)

Ebury Spain

(BoS license)

Ebury Germany

(BoG license) Ebury Italy

(BoI license)

Scenario 2

Scenario 3

8.

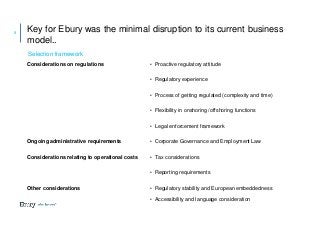

Key for Eburywas the minimal disruption to its current business

model..

Selection framework

Considerations on regulations • Proactive regulatory attitude

• Regulatory experience

• Process of getting regulated (complexity and time)

• Flexibility in onshoring /offshoring functions

• Legal enforcement framework

Ongoing administrative requirements • Corporate Governance and Employment Law

Considerations relating to operational costs • Tax considerations

• Reporting requirements

Other considerations • Regulatory stability and European embeddedness

• Accessibility and language consideration

8

9.

Belgium and Irelandwere short listed

Country assessment1:

Proactive regulation

Regulatory experience

Process of getting regulated (complexity and time)

Flexibility in onshoring /offshoring functions

Legal enforcement framework

Corporate Governance and Employment Law

Tax considerations and reporting requirements

10

1 Ebury`s own analysis

10.

11

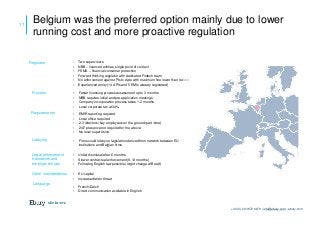

Belgium was thepreferred option mainly due to lower

running cost and more proactive regulation

+44 (0) 20 3872 6670 | info@ebury.com | ebury.com

Regulator

Process

Requirements

Lobbying

Legal enforcement

framework and

employment law

Other considerations

Language

• Two supervisors

• NBB – licenced entities, single point of contact

• FSMA – financial consumer protection

• Forward thinking regulator with dedicated Fintech team

• No enforcement against PIs to date with maximum fine lower than Ireland

• Experienced entity (14 APIs and 5 EMIs already registered)

• Faster licensing process assessment up to 3 months

• NBB requires initial and pre-application meetings

• Company incorporation process takes 1-2 months

• Local corporate tax at 34%

• EMIR reporting required

• Local office required

• 2-3 directors/ key employees on the ground (part-time)

• 24/7 presence not required for the above

• No local supervision

• Firms could lobby on legislation derived from network between EU

institutions and Belgian firms

• Unfair dismissal after 6 months

• Slower contractual enforcement (6-12 months)

• Following English law possible (might change w/Brexit)

• EU capital

• Increased terror threat

• French/Dutch

• Direct communication available in English