Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (20)

Similar to Dl repayment options

Similar to Dl repayment options (20)

Recently uploaded

Recently uploaded (20)

Dl repayment options

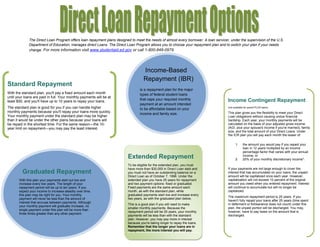

- 1. The Direct Loan Program offers loan repayment plans designed to meet the needs of almost every borrower. A loan servicer, under the supervision of the U.S. Department of Education, manages direct Loans. The Direct Loan Program allows you to choose your repayment plan and to switch your plan if your needs change. For more information visit www.studentaid.ed.gov or call 1-800-848-0979. Income-Based Repayment (IBR) Standard Repayment is a repayment plan for the major With the standard plan, you'll pay a fixed amount each month types of federal student loans until your loans are paid in full. Your monthly payments will be at that caps your required monthly Income Contingent Repayment least $50, and you'll have up to 10 years to repay your loans. payment at an amount intended The standard plan is good for you if you can handle higher to be affordable based on your (not available for parent PLUS loans) monthly payments because you'll repay your loans more quickly. This plan gives you the flexibility to meet your Direct income and family size. Your monthly payment under the standard plan may be higher Loan obligations without causing undue financial than it would be under the other plans because your loans will hardship. Each year, your monthly payments will be be repaid in the shortest time. For the same reason—the 10- calculated on the basis of your adjusted gross income year limit on repayment—you may pay the least interest. (AGI, plus your spouse's income if you're married), family size, and the total amount of your Direct Loans. Under the ICR plan you will pay each month the lesser of: 1. the amount you would pay if you repaid your loan in 12 years multiplied by an income percentage factor that varies with your annual Extended Repayment 2. income, or 20% of your monthly discretionary income*. To be eligible for the extended plan, you must have more than $30,000 in Direct Loan debt and If your payments are not large enough to cover the Graduated Repayment you must not have an outstanding balance on a interest that has accumulated on your loans, the unpaid Direct Loan as of October 7, 1998. Under the amount will be capitalized once each year. However, With this plan your payments start out low and extended plan you have 25 years for repayment capitalization will not exceed 10 percent of the original increase every two years. The length of your and two payment options: fixed or graduated. amount you owed when you entered repayment. Interest repayment period will be up to ten years. If you Fixed payments are the same amount each will continue to accumulate but will no longer be expect your income to increase steadily over time, month, as with the standard plan, while capitalized. this plan may be right for you. Your monthly graduated payments start low and increase every The maximum repayment period is 25 years. If you payment will never be less than the amount of two years, as with the graduated plan below. haven't fully repaid your loans after 25 years (time spent interest that accrues between payments. Although This is a good plan if you will need to make in deferment or forbearance does not count) under this your monthly payment will gradually increase, no smaller monthly payments. Because the plan, the unpaid portion will be discharged. You may, single payment under this plan will be more than repayment period will be 25 years, your monthly however, have to pay taxes on the amount that is three times greater than any other payment. payments will be less than with the standard discharged. plan. However, you may pay more in interest because you're taking longer to repay the loans. Remember that the longer your loans are in repayment, the more interest you will pay.