Call Girls in Karkardooma Delhi +91 84487779280}Woman Seeking Man in Delhi NCR

Houston Retail Market Report 4Q 2010

1. Q4 2010 | RETAIL MARKET

HOUSTON RETAIL MARKET

RESEARCH & FORECAST REPORT

Houston Welcomes New Tenants to the Market

Houston’s retail market continued to improve through the fourth quarter of 2010 with positive net

absorption and lower vacancy rates. For the past six quarters, Houston’s retail market has posted

positive net absorption. Retail vacancy rates for all product types stood at 8.1%, down from 9.9% at this

time last year. Developers have curtailed development, delivering less than 350,000 SF of new retail

CITYWIDE MARKET INDICATORS space in the fourth quarter – compared to over 850,000 SF in the fourth quarter last year – and kept the

4Q-09 4Q-10 construction pipeline nearly empty with less than 120,000 SF in retail projects under construction

compared to 240,000 SF one year ago. Overall, the local market is performing well under less than

QUARTERLY NET ABSORPTION

optimal economic conditions, namely sluggish job growth and low consumer spending levels.

1,042,664 SF 593,490 SF

Macro factors driving the absorption of retail space ultimately tie back to the job count. According to the

YEAR-END NET ABSORPTION

Texas Labor Market Review, total nonagricultural employment in Texas rose by 19,100 jobs in

2,776,796 SF 2,829,420 SF November, gaining jobs in eight out of the last eleven months. At the local level, Houston’s MSA had the

QUOTED RENTAL RATE NNN largest monthly job increase, with 10,900 jobs added in November. Dallas followed with 5,200 jobs

added. Houston also led in the monthly growth of retail and government jobs, adding 7,400 and 2,300

$15.45/SF $14.85/SF

jobs, respectively.

RETAIL VACANCY

9.9% 8.1%

Houston’s above-average population growth is expected to reach 9.5 million by 2035, led by strong

growth in suburban Fort Bend and Montgomery counties. Houston’s diverse population spanning all

QUARTERLY DELIVERIES

economic brackets continues to be a strong draw for retailers. Several companies that have recently

861,316 SF 22,500 SF expanded into the Houston retail market include Carl’s Jr, Jimmy Changas and Saucyritos. Carl's Jr

plans to open 40 new locations in the Houston area. Existing retailers such as Target and Whole Foods

YEAR-END DELIVERIES

plan to expand their presence in the market by opening new locations or remodeling current locations to

3,342,514 SF 343,627 SF include new concepts. Houston’s strong long-term outlook is expected to continue attracting retailers

UNDER CONSTRUCTION seeking to expand market share in one of the fastest growing metropolitan areas in the U.S.

230,949 SF 119,034 SF

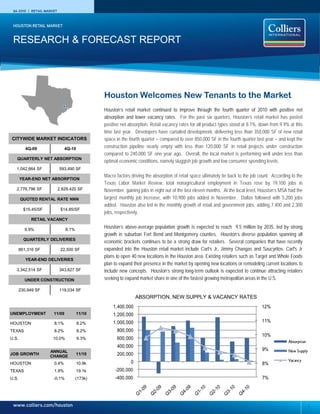

ABSORPTION, NEW SUPPLY & VACANCY RATES

1,400,000 12%

UNEMPLOYMENT 11/09 11/10 1,200,000

HOUSTON 8.1% 8.2% 1,000,000 11%

TEXAS 8.2% 8.2% 800,000

10%

U.S. 10.0% 9.3% 600,000

Absorption

400,000

ANNUAL 9% New Supply

JOB GROWTH

CHANGE

11/10 200,000

0 Vacancy

HOUSTON 0.4% 10.9k 8%

TEXAS 1.9% 19.1k -200,000

U.S. -0.1% (173k) -400,000 7%

www.colliers.com/houston 1

2. RESEARCH & FORECAST REPORT | Q4 2010 | HOUSTON RETAIL MARKET

YTD 2010 TOP RETAIL LEASES

Vacancy & Availability By property type, grocery-anchored

Houston’s retail vacancy rate fell to neighborhood centers led the market in

8.1% in the fourth quarter, down from the fourth quarter with 467,000 SF in

9.9% at this time last year. By product positive net absorption, followed by strip

type on a year-over-year basis, centers with 55,000 SF. Power centers,

community centers posted the largest malls, and community centers followed,

decrease of 370 basis points (bps) to posting positive net absorption of

9.3% vacancy, followed by strip and 50,000 SF, 41,000 SF, and 33,000 SF,

lifestyle centers which fell by 350 and respectively. Single-tenant space had

300 basis points to 10.2% and 5.3%, the only loss reporting (61,364) SF of

Fiesta Mart respectively. In contrast, outlet centers negative net absorption.

Willowchase Shopping Center

and theme/entertainment centers

Oct-10 92,818 SF

year-over-year vacancy rates rose by Rental Rates

690 and 120 bps, respectively.

Kohl’s Although the citywide average quoted

Atascocita Commons Houston’s retail vacancy has remained rental rate of $14.85 per SF NNN

July-10 88,827 SF relatively stable over the past six decreased 0.5% from $14.93 in the

consecutive quarters, with only one previous quarter, and 4.0% from $15.45

Joe V’s Smart Shop quarter, 3Q 2009, dipping below the in the fourth quarter of 2009, about half

San Jacinto Plaza 90% occupancy mark. Following the of the property types posted increases

Oct-10 65,784 SF nearly 100,000 jobs lost in 2009, in rental rates.

Houston is expected to end 2010 with

Malls posted an increase of 32.1% to

Joe V’s Smart Shop positive job growth, with retail and

$18.49 per SF NNN (from $14.00).

12035 Antoine Drive Retail government jobs leading the way in the

Outlet centers and lifestyle centers also

Mar-10 54,690 SF fourth quarter.

posted increases of 40.9% and 35.8%.

Limited new supply will also help the

Academy Sports and Outdoors market stabilize over the coming twelve

In contrast, on a year-over-year basis,

1360 Lake Woodlands Dr community centers’ average quoted

months. Year-end retail deliveries

Octg-10 51,463 SF rental rates fell 20.9% to $14.12 per SF

totaled only 344,000 SF, compared to

NNN (from $17.07 per SF), while

The Room Store the 3.3M SF of retail space added in

theme/entertainment centers’ rental

7666-7736 W FM 1960 2009. Four retail projects in the

rates decreased by 19.0% to $40.84 per

Oct-10 51,147 SF construction pipeline at the end of the

SF NNN (from $48.61 per SF).

fourth quarter totaled a combined

Academy Sports & Outdoors 119,000 SF, compared to 231,000 SF of

Pecan Park Plaza new retail space under construction in

Mar-10 50,300 SF fourth quarter of 2009, with developers

not likely to begin any significant

Second Baptist Church projects until economic conditions

12008 Shadow Creek Parkway

improve.

Aug-10 50,000 SF

Absorption & Demand

Office Depot For the sixth straight quarter, retail net

Cypress Pointe absorption was positive, adding 593,490

Mar-10 48,000 SF SF of positive net absorption to the

year-end total of 2.8M SF. On a

Best Savings Supermarket year-over-year basis, absorption

Lion Square declined from the 946,330 SF recorded

Nov-10 42,205 SF in fourth quarter of 2009.

2

3. RESEARCH & FORECAST REPORT | Q4 2010 | HOUSTON RETAIL MARKET

Sales Activity Leasing Activity

Investment sales for Houston’s retail Houston’s retail leasing activity reached

properties remain sluggish, with the 1.4 million SF in the fourth quarter,

limited availability of credit hampering compared to 1.5 million SF in the fourth

activity. There were 45 transactions in quarter of 2009. Overall, transactions

the fourth quarter with a total dollar under 20,000 SF comprised the largest

Atascocita Center volume of $34M, averaging $116 per group of retail leases, with the market

3820-3826 Atascocita Rd SF with an average 8.7% recording only eight leases over 50,000

Northeast/Lake Houston Submarket capitalization rate. SF in 2010. Several new retailers

RBA: 97,240 SF entered the market including Carl’s Jr,

Among the more significant retail sales

Built: 2003 Jimmy Changas and Saucyritos. Carl's Jr

were the following transactions:

Buyer: Westwood Financial Corp. plans to open 40 new locations in the

Westwood Financial Corp. acquired

Seller: Regency Centers Corp. Houston area. Target announced plans

Sale Date: October 2010 the 97,200 SF Atascocita Commons

to remodel eight area stores to expand

Sales Price: $9.8M located at 3820-3826 Atascocita Rd.

their P-Fresh grocery concept.

The property sold for $9.8M or $101

per SF. Significant retail leases signed through

the fourth quarter included: Fiesta Mart

Jamal Realty, LLC purchased a 12,900

in Willowchase Shopping Center

SF CVS Pharmacy located at 14115 E

renewed their 92,818 SF lease; Kohl’s

Sam Houston Parkway N from Lasco

88,827 SF lease in Atascocita Commons

Development for $4.8M or $372 per

(Kingwood); HEB’s newest retail concept

SF.

Joe V’s Smart Shop’s 54,690 SF lease at

Grace Business Investments 12035 Antoine Drive (Willowbrook) and

CVS purchased the 43,562 SF Shops at the 65,800 SF lease in San Jacinto

14115 E Sam Houston Pky N Almeda and Conn’s Appliance Center Plaza; Academy Sports and Outdoors’

Near Northeast Submarket building located at 10900 Gulf Freeway 50,300 SF lease at Pecan Park Plaza

RBA: 12,900 SF from SET Asset Properties LLC for (League City); Second Baptist Church’s

Built: 2007 $5.0M or $115 per SF. 50,000 SF lease at 12008 Shadow Creek

Buyer: Jamal Realty, LLC

Pky. (Far South); and Office Depot’s

Seller: Lasco Development

Sale Date: November 2010 48,000 SF lease at Cypress Pointe

Sales Price: $4.8M (Cypress).

For additional retail lease transactions signed

year-to-date, please see the select list on page two.

HOUSTON RETAIL MARKET SUMMARY

Direct Sublet Total

Direct Vacant Vacancy Sublet Vacancy Total Vacant Vacancy 4th Qtr Net Year-End Net Weighted Avg.

Rentable Area SF Rate Vacant SF Rate SF Rate Absorption Absorption Rental Rate NNN

Strip Centers 30,386,090 3,060,682 10.1% 24,754 0.1% 3,085,436 10.2% 55,341 764,710 $15.82

Neighborhood Centers 75,889,933 8,037,831 10.6% 124,707 0.2% 8,162,538 10.8% 466,934 1,274,548 $13.61

Community Centers 38,298,197 3,503,711 9.1% 42,452 0.1% 3,546,163 9.3% 32,531 392,215 $14.12

Power Centers 16,581,902 756,459 4.6% 66,944 0.4% 823,403 5.0% 49,592 436,110 $19.03

Lifestyle Centers 2,426,476 128,907 5.3% - 0.0% 128,907 5.3% 2,500 109,876 $31.52

Outlet Centers 1,228,700 102,117 8.3% - 0.0% 102,117 8.3% 5,100 9,530 $13.01

Theme/Entertainment 1,934,868 244,787 12.7% - 0.0% 244,787 12.7% 1,600 (92,988) $40.84

Single-Tenant 45,787,847 1,596,071 3.5% 34,554 0.1% 1,630,625 3.6% (61,364) (127,559) $11.53

Malls 31,020,048 1,882,937 6.1% 58,539 0.2% 1,941,476 6.3% 41,256 62,978 $18.49

Greater Houston Retail 243,554,061 19,313,502 7.9% 351,950 0.1% 19,665,452 8.1% 593,490 2,829,420 $14.85

3

4. RESEARCH & FORECAST REPORT | Q4 2010 | HOUSTON RETAIL MARKET

Retail Development Pipeline

HOUSTON RETAIL PROJECTS UNDER CONSTRUCTION

Estimated

Map # Submarket Property Name Address RBA % Leased Developer Delivery

1 Inner Loop 1523 Airline Bldg 1623 Airline Dr 12,000 50 ReMax CityView Jan-11

2 Fairfield The Shops at Cypress Crossing27126 Hwy 290 17,006 100 Texas Land & Lease Jan-11

3-6 Cypress Fairway Point, Bldgs. A-E 15103 Mason Rd 80,000 0 Fairfield Village Community Mar-11

7 Montgomery County Life Check Pharmacy 1490 Researh Forest 10,028 100 AMREIT Apr-11

Total retail under construction 119,034

7

3

5

5 2

6

1

SELECT HOUSTON 2010 RETAIL DELIVERIES

Year

Submarket Property Name Address RBA % Leased Developer Built

Willowbrook Joe V's Smart Shop 12035 Antoine Dr 66,690 82.0% NewQuest (for HEB) May-10

Memorial East CityCentre, Bldg 13 12808 Queensbury Ln 47,584 61.3% Midway Companies Jan-10

Baytown Chase Plaza Center 7599 Garth Rd 30,000 0.0% Ed Rutledge Associates Feb-10

Tomball Ross (Tomball Marketplace) 14223 FM 2920 Rd 27,689 100.0% Weingarten Realty Mar-10

Inner Loop River Oaks West Ave Building C 2800 Kirby Dr 24,130 100.0% Gables Residential May-10

Sugar Land/Fort Bend Mody Plaza 1611 Hwy 6 10,280 54.5% Mihir Mody Sep-10

Washington Boulevard 3939 Washington Retail 3939 Washington Ave 22,800 59.9% Apex Group Mar-10

West Westheimer Lakes Plaza Phase II 26440 FM 1093 22,500 55.6% Parkhill Investments Nov-10

Kingwood Kings Harbor Waterfront Village, Bldgs. 8 & 9 1660 W Lake Houston Pky 22,200 81.7% Midway Companies Mar-10

Hobby Cullen Commons II 12805 Cullen Blvd 20,000 50.0% Cullen Commons Apr-10

Northline Carmel Plaza 6906 Airline Dr 16,000 62.5% Chaleh Corporation Mar-10

4

5. RESEARCH & FORECAST REPORT | Q4 2010 | HOUSTON RETAIL MARKET

480 Offices Worldwide

EUROPE AND

NORTH AMERICA MIDDLE EAST

HAWAII ASIA PACIFIC

AFRICA

SOUTH

AMERICA

AUSTRALIA

61 Countries on 6 Continents

191 AMERICAS

135 USA

39 CANADA

17 LATIN AMERICA

26 ASIA

95 EUROPE/MIDDLE EAST/AFRICA COLLIERS INTERNATIONAL

1300 Post Oak Blvd, 2nd Floor

168 AUSTRALIA/NEW ZEALAND

Houston, Texas 77056

$1.9 BILLION IN GLOBAL REVENUE Main: 713.222.2111

Fax: 713.830.2118

1.4 BILLION SQUARE FEET UNDER www.colliers.com

MANAGEMENT

15,000 PROFESSIONALS

5