MARKET OUTLOOK

USreal GDP growth slowed to 1.9% on an annualised basis in 4Q2016 from 3.5%

in the previous quarter. For the year 2016, the real GDP growth was recorded at

1.6%, the lowest since 2011. Despite the unexciting number recorded, US econo-

my in general is in a stronger state. Private consumption grew at annual rate of

2.5% from October to December, thanks to third consecutive quarters of strong

growth in durable goods orders. Higher spending on durable goods (averaged at

10.8%) indicates recovery in consumer sentiments, and this was further mirrored

on the increase in job creation and pick up in the business investment. Nonfarm

payrolls grew by 227,000 in January compared to 157,000 in December 2016.

China’s official manufacturing PMI edged down to 51.3 in January mainly due to

seasonal New Year and Chinese New Year holidays. It managed to stays in expan-

sionary zone (above 50.0) for the past six months, which suggests prospects of

continuous improvement in manufacturing activities. Domestic and external de-

mand remained resilient with import and new export order rising to 50.7 and 50.3

respectively.

Japan’s manufacturing PMI grew to 52.7 in January, signalling a stronger improve-

ment in operating conditions. Production rose for the sixth consecutive months, at

similar rate of expansion experienced in December’s 12-month high. This is mainly

attributable to new product launches and increase in new export orders. New ex-

port orders rose the quickest rate in one year, as firms attributed the increase in the

new work inflows to improved advertising and demand from both domestic and

international customers.

All ASEAN bourses recorded gains for the month of with the exception of Jakarta

Composite Index (JCI) which inched down marginally by 0.1%. Leading the gainers

at 5.8% was Straits Times Index (STI), followed by Philippines Composite Index

(PCOMP) at 5.7%, Stock Exchange of Thailand (SET) at 2.2% and FTSE Bursa

Malaysia KLCI (FBMKLCI) at 1.8%.

We believe that President Trump would try to honour his promises during his elec-

tion campaign. Thus, trade policy will be one of the two most important economic

issues (the other is infrastructure spending) that we are cautious of. We believe

that US withdrawing from TPP and renegotiating of NAFTA is widely expected but

the absence of immediate actions to impose tariff suggests that Trump administra-

tion may want to negotiate under more favourable term or conditions of US. We

speculate that Trump may introduce new trade barriers rather than making the

move to raise the tariff first. Under such circumstances, the global market may take

another turn of turmoil and confusion until a more clarification can be made from

US’s trade policy implementation. We also think that profit taking activity due to tax

policy is not realizing soon. As such, we increased our exposure to Malaysia mar-

ket as the market is more resilient and election story still in play for the year 2017.

Historically, Malaysia market would experienced a run up ahead of election.

EQUITY

FBMKLCI extended its gain in January, starting 2017

with 1.8% gain. Looking at the trading participants,

foreigners returned as net buyer, albeit tepid at

RM419mil whilst the retailers taking the opportunities

to offload their position, effectively sold RM330mil

worth of shares. Local institutions turned net seller

for the month, sold RM89mil worth of shares after

buying RM922mil worth of shares in December.

Malaysian sectors started the year with all landed in

the positive territory. Taking the lead with 10.3% is

the technology sector, followed by construction which

experienced 3.8% gain. Technology sector reported

robust gain in tandem with investors optimism in

anticipation of iPhone 10-years anniversary this year.

On another note, the export sectors (i.e Electric &

Electronic) also benefited from weakened ringgit in

4Q2016 ( plunged 8.4% q-o-q). Construction sector

saw a modest gain in the beginning of the year at-

tributable to investors optimism for more mega pro-

jects contract rollouts in 2017. Some of the expected

rollouts include the remaining packages for Mass

Rapid Transit Line 2 (MRT 2) in 1H2017, Light Rail

Transit Line 3 (LRT 3) in 1Q2017 and potentially the

East Cost Rail Link towards end –2017.

BONDS

On bond side, all yields on the Malaysian Govern-

ment Securities (MGS) continue to decline in the

January. 3-year, 5-year, 7-year and 10-year MGS

reduced by 26bps, 11bps, 20bps and 8bps to close

at 3.26%, 3.59%, 3.93% and 4.14% respectively. The

main concern on the government debt is the maturity

-driven outflow as there is a total of RM67bn of MGS/

GII due to mature in 2017.

COMMODITIES

llocatorMONTHLY INVESTMENT ALLOCATOR

ISSUE

FEB 2017

Nymex WTI crude oil retreated 1.7% in January after

a robust 8.7% gain in December, to close at $52.8/

barrel from $53.7/barrel. Crude palm oil price contin-

ued its uptrend momentum in January, gained 0.4%

to close at RM3,230.0/MT from RM3,218.0/MT in the

previous month on the back of ongoing tight invento-

ries. Gold rebounded in January, to register gain of

4.9%, from $1,151.7 in December to $1,208.6 in

January as uncertainty over Trump’s policies execu-

tion continues to puzzle investors post his inaugura-

tion.

2.

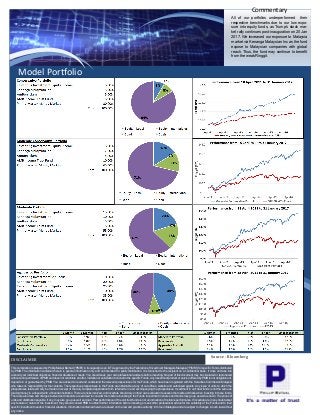

Commentary

Model Portfolio

This compilationis prepared by Phillip Mutual Berhad (“PMB”) in its capacity as an IUTA approved by the Federation of Investment Managers Malaysia (“FIMM”) for specific Funds distributed

by PMB. The information contained herein is general information only and not intended for public distribution. It is furnished to the recipient on a confidential basis. It does not take into

account your individual objectives, financial situations or needs. You should seek your own professional advisers before investing. No part of this document may be circulated or reproduced

without prior permission of PMB and does not constitute an offer, invitation or solicitation to invest in the specific Funds. Any investment product or service offered by PMB is not obligations of,

deposits in or guaranteed by PMB. You are advised to read and understand the relevant prospectuses for the Funds, which have been registered with the Securities Commission Malaysia

who takes no responsibility for the contents. The respective prospectuses to the Funds are obtainable at any of our offices, website and authorised agents. Any issue of units to which the

prospectuses relate will only be made on receipt of the duly completed application form referred to in and accompanying the prospectuses. Investment in unit trust funds is not the same as

placing money in a deposit with a financial institution. There are risks involved, and investors should rely on their own evaluation to assess the merits and risks when investing in these funds.

There are also fees and charges involved and investors are advised to consider them before investing in the Funds. Investment in shares and bonds may go up as well as down. The prices of

units and distribution payable, if any, may also go up as well as down. Past performance of the unit trust funds is not an indication of its future performance. If investors are in any doubt about

any feature or nature of the investment, they should consult PMB to obtain further information before investing or seek other professional advice for the suitability of the Funds and to their

specific investment needs or financial situations. Information contained herein are based on the law and practise currently in force in Malaysia and are subject to changes in such law without

any notice.

DISCLAIMER

Source : Bloomberg

All of our portfolios underperformed their

respective benchmarks due to our low expo-

sure into equity funds, as Trump’s stock mar-

ket rally continues post-inauguration on 20 Jan

2017. We increased our exposure to Malaysia

market via Kenanga Malaysian Inc as the fund

expose to Malaysian companies with global

reach. Thus, the fund may continue to benefit

from the weak Ringgit.