Defer Tax Gaininto New Replacement Property

1031 TAX DEFERRED EXCHANGES

William E Bryant CPA, CVA & Realtor - Copyright 2016

2.

• Trade ofLike-Kind Property for Like-Kind Property

– Real Property Exchanged for other Real Property

• Must be Property Held for Investment in the same Property Class.

– For example, Land can be exchanged for other Land, or exchanged for Rental

Property or Commercial Property, since it’s in the same Class.

– Personal Property for Personal Property

• Antique Car for Antique Car

• Artwork & Collectibles for other Artwork & Collectibles

– What does NOT Qualify?

• Trading Personal Property for Investment Real Property – Mixed Class

• Partnership Interest (considered Personal Property) for Real Property

• Trading your Principal Residence (not considered an Investment Property)

WHAT QUALIFIES FOR A 1031 EXCHANGE

William E Bryant CPA, CVA & Realtor - Copyright 2016

3.

• Tax Consequencesof Traditional Sale vs 1031 Exchange

– Traditional Sale of Property – Typical Transaction (See Chart)

• Must pay Federal and State Income Taxes on the Capital Gain.

– Pay higher Tax Rate on Recapture of Depreciation on those Assets.

– Have less Net Cash Proceeds Available to Reinvest in Replacement Property.

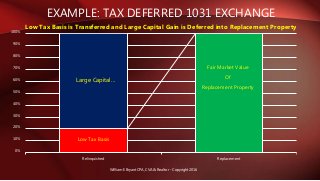

– Tax Deferred 1031 Exchange (See Chart)

• No Taxes paid if you “Trade Up” and if no Cash is received.

• Transfer low tax basis into the Replacement Property.

• Defer Large Capital Gain until Final Sale or Include later in a Final Estate.

TAX BENEFITS OF A 1031 EXCHANGE

William E Bryant CPA, CVA & Realtor - Copyright 2016

4.

Disbursement of CashProceeds on Typical Sale – Assume No Loan Payoff

EXAMPLE: TAX CONSEQUENCES OF TRADITIONAL SALE

William E Bryant CPA, CVA & Realtor - Copyright 2016

5.

Low Tax Basis

FairMarket Value

Of

Replacement Property

Large Capital…

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Relinquished Replacement

EXAMPLE: TAX DEFERRED 1031 EXCHANGE

William E Bryant CPA, CVA & Realtor - Copyright 2016

Low Tax Basis is Transferred and Large Capital Gain is Deferred into Replacement Property

6.

• Identify aQualified Intermediary (“QI”) and Closing Agent

and/or Title Company to handle the Transactions.

• Sell the Relinquished Property via the QI – Now the Clock

starts ticking!

• You have 45 Days to identify a Replacement Property.

• You have a total of 180 Days to Close on the Replacement

Property via the QI.

• Review the following Timeline

WHAT STEPS ARE NEEDED IN A 1031 EXCHANGE

William E Bryant CPA, CVA & Realtor - Copyright 2016

7.

Sell Relinquished

Property

45 Daysto Identify

Replacement Property

180 Days to Close on

Replacement Property

TIMELINE FOR A 1031 EXCHANGE TRANSACTION

William E Bryant CPA, CVA & Realtor - Copyright 2016

8.

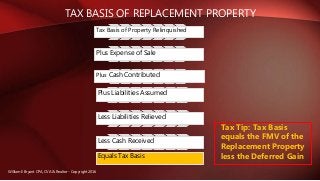

TAX BASIS OFREPLACEMENT PROPERTY

William E Bryant CPA, CVA & Realtor - Copyright 2016

Tax Basis of Property Relinquished

Plus Expense of Sale

Plus Cash Contributed

Plus Liabilities Assumed

Less Liabilities Relieved

Less Cash Received

Equals Tax Basis

Tax Tip: Tax Basis

equals the FMV of the

Replacement Property

less the Deferred Gain

9.

• The Ownershipin the Replacement Property must be identical to

the Ownership in the Relinquished Property.

• There is a 2-Year Investment requirement if a related Party is

involved in the Transaction.

• Consider using Tenants in Common (“TIC”) to separate the

Property ownership from a Partnership, then proceed with the

1031 transaction with your share as TIC owner.

• Reverse Exchanges might be a good strategy in certain Market

and/or Unique Opportunity situations.

• UpREITS and other Post-Transaction Strategies are possible.

OTHER CONSIDERATIONS IN A 1031 EXCHANGE

William E Bryant CPA, CVA & Realtor - Copyright 2016

10.

• For moreinformation about 1031 Tax Deferred Strategies:

– Or to work with a Qualified Intermediary

– Or to assist in the Sale/Purchase of the Real Estate

– Or to Consult with a Tax Advisor about your specific situation

• Please contact Bill Bryant at 612-872-9684 or email at:

• Also please visit: for more info.

THANK YOU

William E Bryant CPA, CVA & Realtor - Copyright 2016