Recommended

Recommended

More Related Content

What's hot

What's hot (6)

Applying the SABR model to German power Forwards

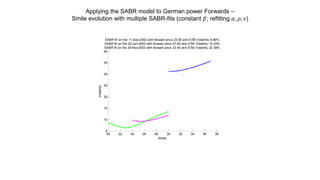

- 1. Applying the SABR model to German power Forwards – Smile evolution with multiple SABR-fits (constant 𝛽; refitting 𝛼, 𝜌, 𝜈) 20 22 24 26 28 30 32 34 36 38 5 10 15 20 25 30 35 40 SABR fit on the 11-Sep-2002 with forward price 23.95 and ATM Volatility 6.66% SABR fit on the 20-Jun-2003 with forward price 27.65 and ATM Volatility 10.03% SABR fit on the 24-Nov-2003 with forward price 33.40 and ATM Volatility 32.39% Strike Volatility