April 2017

•

1 like•202 views

Newsletter of our firm Raju and Prasad Chartered Accountants

Recommended

Recommended

More Related Content

What's hot

What's hot (9)

Similar to April 2017

Similar to April 2017 (20)

Recently uploaded

Recently uploaded (20)

April 2017

- 1. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Contact us: Email : hyderabad@rajuandprasad.com Website: www.rajuandprasad.com April 2017 Volume 4, Issue 2 FOCAL POINT Newsletter from Raju and Prasad Chartered Accountants

- 2. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Page 3Raju and Prasad Chartered Accountants Page 1 Dear Reader, Our editorial comments for this month are on the ‘Why or why not Aadhar be linked with IT Returns’. This month we have covered the Leather Industry in our Industry Review. We have also included an article on the amendments to the Income Tax applicable from 1st April, 2017 written by Sri. Avinash T Jain, FCA Please give your views and also send this newsletter to your friends. Regards For Raju& Prasad Chartered Accountants M Siva Ram Prasad Partner

- 3. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Page 3Raju and Prasad Chartered Accountants Page 2 Book Release We are glad to inform you that Articles from our newsletter of first two years were compiled into a book ‘My Views and Reviews` and was released by Sri. V.K Saraswat, Member NITI Aayog on 11th of March, 2017. The meeting was presided over by Sri. P.S Rama Mohan Rao, former governer of Tamil Nadu. The book was introduced by Dr. N Bhaskar Rao chairman Center for Media Studies (New Delhi).

- 4. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Page 3Raju and Prasad Chartered Accountants Page 3 Contents Book Release..................................................................................................................................................2 Contents.............................................................................................................................................................3 Editorial...............................................................................................................................................................4 Aadhar, why and when mandatory?............................................................................................................. 4 Why and Why not Income tax return be linked with Aadhar................................................................................................ 5 Industry Review...........................................................................................................................................6 Leather Industry ...................................................................................................................................................... 6 History................................................................................................................................................................................................................................ 6 Leather processing................................................................................................................................................................................................... 7 Process Flowchart ..................................................................................................................................................................................................... 8 Government Initiatives......................................................................................................................................................................................... 9 Present Policies .........................................................................................................................................................................................................10 Research and Development............................................................................................................................................................................11 Challenges.....................................................................................................................................................................................................................11 INCOME TAX AMENDMENTS APPLICABLE W.E.F 01.04.2017.......................................................13 Changes in Income Tax Return Form for FY 2016-17 relevant to AY 2017-18:.................................................13 Policy Watch................................................................................................................................................. 16 SEBI...............................................................................................................................................................................16 Revision of limits of investments by FPIs in Government Securities ...........................................................................16 Company Law ..........................................................................................................................................................16 Powers of Registrar of Companies to strike off the names of companies under section 248(1) of the Companies Act, 2013...........................................................................................................................................................................................16 Amendment in Schedule III ...........................................................................................................................................................................16 Indirect Taxes..........................................................................................................................................................17 Service tax on service rendered by a person located in a non-taxable territory to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India............................................................................................................................17 Verdicts............................................................................................................................................................ 18 Direct Taxation .......................................................................................................................................................18 Profit on sale of Shares that are converted into investment from stock-in-trade and sold at a later stage shall be exempted u/s 10(38) .......................................................................................................................................................18 ►►► PHOTOGRAPH OF THE MONTH ..................................................................................... 19

- 5. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Page 3Raju and Prasad Chartered Accountants Page 4 Editorial Aadhar, why and when mandatory? he Finance Bill introduced in the parliament is amended in the last leg of the Parliament Session and was passed on 30th March, 2017. The bill was amended to make Aadhar compulsory for filing Income Tax Returns filed on or after 1st July, 2017. The Income Tax Returns filed before 1st July, 2017 need not mention Aadhar Number. The Aadhar Act, 2016 was enacted with the title Aadhar (Targeted Delivery of Financial and other Subsidies, benefits and services) Act, 2016. Without going into the nitty-gritties of whether it is money bill or not, the name suggests that the Act is meant for overseeing or monitoring the various subsidies, financial benefits and public distribution system. Essentially it is to make sure that there is no misuse of various government schemes which are meant for targeted population. It is an open secret that every state government weeded out fake ration cards. T

- 6. Page 5Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> In all its good sense while allotting the number government does not seek information on caste, creed or religion. Especially the income particulars are not collected which is the key parameter to understand the distribution of benefits and if the purpose of the scheme is to give benefit on income basis. Perhaps it is the late thinking to link IT Returns with Aadhar. Why and Why not Income tax return be linked with Aadhar The question is whether Aadhar card is voluntary or mandatory. It was always mentioned that Aadhar is voluntary, Apex Court also confirmed the same. While every IT assesse is allotted a PAN, Aadhar is an additional option to oversee certain financial misdeeds. The Finance Act 2017 also makes PAN invalid if Aadhar particulars are not mentioned. Aadhar being mandatory was triggered when it was made compulsory for Mid-Day Meal Scheme and for pensioners, government may exercise caution in such situations. It is voluntary for individuals who seek benefits but government has always a right to make it compulsory for certain purposes. If the government wants to link Aadhar with IT returns it is only to have better surveillance over financial transactions. Whether any legal recourse is required to make it mandatory should be examined. The next fear is whether the information is kept secret. The UIDAI specifically mentions that the information available with the authorities will not be disclosed to anybody except in special circumstances under National Security. There is no great information available since the application does not seek any sensitive information. There is no need for unnecessary apprehension about secrecy. Under the RTI Act there is no obligation to give any information by any authority, any personal information which has no relevance to any public activity or interest. Under section 8(1) J of the RTI Act demographic and biometric data of a person cannot be disclosed except to the respective person. Above all what we should bother about is whether Cyber Security is enough for the information available with the authorities and various agencies working under the act? -M Siva Ram Prasad

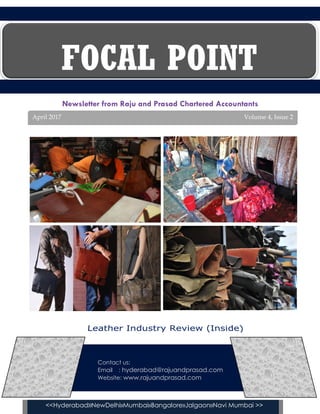

- 7. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Raju and Prasad Chartered AccountantsRaju and Prasad Chartered Accountants Page 6 Industry Review Leather Industry History here is no real evidence of the use of leather in ancient times, but it is known to be used by Indians. The references to use were mentioned in certain scriptures. Lord Shiva used a drum called `Damarukam’ which had leather surface, various tribals are known for drum beating, Indian sages using animal skins for sitting are all known sources that hides and skins were in use. Marco Polo in 1290 AD mentioned about the presence of leather industry in India and its trade with other countries. The basic footwear was made of leather in villages and the activities remained as an artisan oriented work in certain areas. The processing of the basic skin was made out of vegetable based juices or smoking process through certain leaves and barks of plants like oak, chestnut, tanoak, hemlock, mangroves, accacia etc. Chemical T

- 8. Page 7Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> processing was known only from 18th / 19th century. Leather processing Raw hides and skins are first cured to avoid decay by different methods like salting, chilling, freezing etc. The cured material is soaked in water for number of days in case of vegetable processing and for a lesser time in case of chemical processing. The soaked hides are further processed by liming, for removal of hair and painting for removal of wool. After liming, deliming is done to remove alkaline chemicals and make leather softer. Further process is called bating in which enzyme treatment is given to make it soft and stretchable by removing chemicals remaining after deliming. After this, the hides are passed through acid salt pickle liquor to make it ready for tanning. Tanning is a process to make the hide into leather by stabilising the collagen structure. The word tanning is derived from `tannara’, Latin word for oak bark. The process can be done either through plant bark and leaves or chrome salts and sulphuric acid. The chromium salts are neutralised in neutralisation process with sodium bicarbonate, sodium, calcium formate, etc. Then the semi-finished leather is retanned through retanning agents in case of chrome tanning for getting uniform thickness. After tanning, splitting is done through machine split where the leather is split into two layers, one with grain surface and the other without grain surface. The lower layer can be further made into Suede Leather. The split leather is then dyed to get the required colour. The hides and skins are taken from various animals like cows, calves, buffaloes, sheep, and goat. Special skins are also taken from other animals like rabbits, deers, alligators and snakes. The various finishes that are known as nappa, suede, nubuck, arethe, sumin finishes. The

- 9. Page 8Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> other finishes include fully pigmented finish, antique finish, wiper finish, grain finish etc.The industry is originated mainly due to meat industry and helped the growth of fashion industry. The industry can be classified into trade in hides and skins and then into leather goods. Leather goods can further be classified into footwear including shoe uppers and soles, leather goods like handbags, travel bags, leather garments, saddlery and harness, upholstery furniture etc. A major consumer of leather footwear is Indian Army. Process Flowchart Hides and Skins Curing Soaking liming Deliming Bating Pickling Depickling Vegetable Tanning Splitting Retanning Dyeing Finished Leather Trading Goods Manufacturing Mineral Tanning Neutralisation

- 10. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Raju and Prasad Chartered AccountantsRaju and Prasad Chartered Accountants Page 9 Government Initiatives An artisan oriented activity has grown into a cottage industry and remained for a long time in that stage. The excise regulations on turnover and restrictions on usage of power up to 2 horse power, motors and employees not to exceed 50, made the industry growth stunted. This sector largely remained as a trade in hides and skins. Trend in Production of hides and Skins (In million Pieces) S.No. Category 2000 2004 2008 2012 1 Bovine Hides and Skins 38 38.6 41.6 43.1 2 Sheepskins and Lambskins 29.8 31.2 36.2 37 3 Goatskins and Kidskins 71.3 74 83.7 88.9 Total 139.1 143.8 161.5 169 Source: FAO The industry is in small and medium scale sectors; large scale units are few in the country. The first industrial policy resolution which was adopted after independence in 1948 also emphasised the need for protection of the industry. The industry was reserved for small scale units for a long time. Government initiatives for export promotion started from 1970, export policy resolution and encouragement was given for exports of value added products instead of trading hides and skins. In 1973 the industry is dereserved and imports of capital goods and consumables were allowed and the duty structure is liberalised. Indian Leather development programme (ILDP) was initiated in ninth five year plan and is being implemented to modernise the technologies and production facilities with expanded capacities. The programme also helps the rural artisans to upgrade their skills. The programme also has a sub-plan, Integrated Development of Leather Sector (IDLS) to promote parks, clusters design facilities, Intech Mart Scheme etc. Tannery Modernisation scheme is another scheme initiated under ILDP to improve the tanneries in the year 2000.

- 11. Page 10Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Leather technology mission is initiated to create awareness about the latest technologies available for the industry. Present Policies Presently central excise is not levied on certain foot wear and there is concessional duty on certain foot wear manufactured including shoe uppers. Capital goods can be imported without duties under EPCG with export obligations. 3% Interest equalisation scheme is available for 5 years from 1st April, 2015. Skill Development and Skill upgradation programmes are available from National Skill Development Corporation and Pradhan Manthri Kaushal Vikas Yojana (PMKY) 100% FDI is allowed in the sector under automatic route. Market access initiative scheme and market development assistance schemes of Department of Commerce are available to support marketing. Fact Sheet The leather industry of India has a prominent place in the world’s leather industry which is evident from the following: India is the second largest producer of footwear in the world. India produces 2.5 billion Sq. Feet of leather which is 13% of the world production. Leather industry is the eighth major foreign exchange earner for the country. India’s cattle population is 20% of world’s cattle (cows and buffalos) and 11% of world’s goat and sheep population. The industry employs nearly 2.5 million people.

- 12. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Raju and Prasad Chartered AccountantsRaju and Prasad Chartered Accountants Page 11 Indian Export of leather and leather products during the last 5 years (Value in Million USD) Product 2011-12 2012-13 2013-14 2014-15 2015-16 Finished Leather 1024.69 1093.73 1284.57 1329.05 1046.44 Footwear 2079.14 2066.91 2557.66 2945.58 2737.85 Leather Garments 572.45 563.54 596.15 604.25 554.29 Leather Goods 1089.71 1180.82 1353.91 1453.26 1369.00 Saddlery& Harness 107.54 110.41 145.54 162.70 146.38 Total 4873.53 5015.41 5937.97 6494.84 5853.96 % Growth 22.80% 2.91% 18.39% 9.37% -9.86% Source: DGCI&S Research and Development Research and development in leather sector was started by Central Leather Research Institute (CLRI) set up as early as in 1948. This is the world’s biggest research laboratories in this sector and has developed number of new technologies like waterless chrome tanning which will use titanium tanning. This will help reducing the effluents. The other environmental friendly technologies developed by the institute are less salt curing system, sludge free liming process, total lime and sulphide free deliming of hides and skins. In addition the CLRI conducts many skill development courses and training programmes. Other institutions involved in development of leather and leather goods include Central Footwear Training Institute (CFTI), National Institute of Fashion Technology (NIFT), Foot wear Design and Development Institute (FDDI) and Council for Leather Exports (CLE). Challenges The industry which has a role in socio- economic development of the country suffers from certain challenges. Environmental pollution is a major threat from the industry to the society and is not encouraged in a big way. The competition from synthetic substitutes is a major challenge and awareness about

- 13. Page 12Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> the health hazards for such products on humans is not propagated. The price factor between synthetic product and natural leather makes a normal customer to go for synthetic product. Raw material collection and processing poses a challenge since the raw material source is scattered and quality of material is not consistent because of the quality of the aminals and animal husbandry practices prevailing. Industry which is mostly in small scale sector faces the problems of funding, marketing and technology upgradation and modernization. The cluster approach to have common facilities will solve many problems including effluent treatment. Recent laws banning the cow slaughter may impact the raw material supply. Using modern technologies to reduce the water usage, sludge free limig etc, will solve the environmental isssues. As per the UNIDO study the industry has a promosing future both in domestic market and export market. -Team at Raju and Prasad

- 14. Page 13Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> INCOME TAX AMENDMENTS APPLICABLE W.E.F 01.04.2017 Changes in Income Tax Return Form for FY 2016-17 relevant to AY 2017-18: 1. As per the forms notified by the Income Tax Department, the assesse is required to disclose cash deposit over Rs.2,00,000/-, deposited during demonetization period (i.e. 08.11.2016 to 31.12.2016) 2. The government has introduced a new schedule requiring individuals and HUF to declare the value of Assets and Liabilities if their total income exceeds Rs. 50 Lakhs. Now taxpayers are also required to disclose address of immovable property and description of movable properties under new ITR forms. Further, a new field has been introduced for the disclosure of ‘Interest held in the assets of a firm or AOP as a partner or member’. Such members or partners are also required to disclose name, address, PAN of the firm or AOP.

- 15. Page 14Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Kindly make note of the following changes in IT law that come into effect from 1-4-2017 - (1) Limit for payment of expenses by cash (both, capital and revenue expenditure) reduced from Rs.20,000/- to Rs.10,000/- per day in aggregate per person. Capital expenses paid in cash beyond the said limit will not be taken into account for depreciation purposes. However, the cash payment limit for lorry fright etc. remains the same at Rs.35,000/-. (2) No person shall receive an amount of 2 lakh rupees or more, by cash (Sec. 269ST)- (a) in aggregate from a person in a day; or (b) in respect of a single transaction; or (c) in respect of transactions relating to one event or occasion. The penalty for violation of above is to be a sum equal to the amount of such receipt. Examples for above - i) If one sells goods worth Rs. 2,00,000/- through two different bills of Rs.100000 each to one person and accepts cash in single day at different times then section 269ST(a) will get violated. ii) If one sells goods worth Rs. 2,00,000/- through single bill to another person and receives cash of Rs.1,00,000/- on day 1 and another Rs.1,00,000/- on day 2 then section 269ST(b) will get violated, since it pertains to single transaction. iii) If one accepts cash of Rs.180000 for sales and Rs.20000 for freight charges, then section 269ST(c) will get violated even if cash is accepted on different dates, since they pertain to a single sales event. iv) If one sells his car for Rs.2,00,000/- and receives the amount in cash, then penalty levied on him will be Rs.2,00,000/-. (2A) In view of the newly introduced above said penal provisions relating to cash sales, the existing provisions (in vogue from 1.6.2016) relating to collection of TCS @ 1% on cash sales exceeding Rs.2 lakhs (Rs.5 lakhs, in the case of jewellery) are deleted. Consequently, there is no need to collect TCS on cash sales exceeding Rs.2 lakhs. Straight away it will attract equal amount penalty now. (3) For below Rs.2 crores turnover cases - A. For Non Cash Sales (through Digital, Online, cheque, Bank etc.) : Net Profit will be taken as 6% of Turnover/Gross Receipt. B. For Cash Sales : Net Profit will be taken as 8% of Turnover/Gross Receipt. (4) Tax Exemption limit is Rs.2,50,000/- (same as earlier) - 1. After that, upto Rs.5 lakh, Tax Rate is 5% (earlier it was 10%). Tax rebate of maximum Rs.2500 will be allowed, for total income upto Rs.3.50 lakhs. 2. Individuals having total income exceeding Rs.50 lakhs but below Rs.1 crore, are to pay surcharge @ 10% of the tax. Those having total income

- 16. Page 15Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> exceeding Rs. 1 crore shall continue to pay surcharge @ 15%. (5) Payment of Rent - Rs.50,000 per month by any Individual or HUF (not subject to Tax Audit requirements) - deduct TDS @ 5%. (6) Capital Gain in respect of Land & Buildings- – Periodicity for long term Capital Gain is reduced from 3 years to 2 years. – Base year shifted from 01.04.1981 to 01.04.2001 for all assets including Immovable property. (7) Corporate tax rate for the account year 2017-18 for companies with annual turnover upto Rs. 50 crores (in the account year 2015-2016) is reduced to 25%. No change in firm tax rate of 30%. (8) Donations made exceeding Rs.2000 will be not be eligible for deduction under section 80G, unless these are made using modes other than cash. Consequently, trusts accepting 80G donations may advise their donors to give donations exceeding Rs.2000 vide cheque / RTGS / digital modes. (9) Sale of unquoted shares to be taxed at (deemed) fair value. (10) In absence of PAN of the buyer of specified goods, the rate of TCS will be twice of the extent rate or 5%, whichever is higher. (11) From financial year 2017-18, if Return is not filed within due date, late fee of Rs.5,000/- for delay up to 31st December, and Rs. 10,000/- thereafter. (12) Every person who is eligible to obtain AADHAR number, should quote such number, on or after 1 July 2017, in the Return of income. Furthermore, every person who has been allotted PAN as on 1st July 2017 must intimate the AADHAR number to the Tax Authority, failing which, PAN allotted to such person shall be deemed to be invalid. Kindly note that linking of AADHAR with PAN is not possible, unless name as per AADHAR and PAN match perfectly. Hence, please take steps to rectify your name as per AADHAR to match as per PAN. (13) Every person has to link AADHAR number with all 1their bank accounts on or before 30.04.2017. In case of failure, the banks may block bank accounts. (More clarification is awaited on the same) (14) Where Sec.12AA registered trusts modify their objects clause, they need to apply within 30 days to CIT for approval of the modified clauses. - Avinash T Jain, FCA

- 17. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Raju and Prasad Chartered AccountantsRaju and Prasad Chartered Accountants Page 16 Policy Watch SEBI Revision of limits of investments by FPIs in Government Securities SEBI vide circular no. IMD/FPIC/CIR/P/2017/30 date 3rd April, 2017 has revised the limit of investment by Foreign Portfolio investors in Government Securities for the quarter April to June 2017 as follows: Type of Instrument Upper cap as on 31/03/2017 (INR Cr) Revised upper cap with effect from 03/04/2017 (INR Cr) Government Debt 1,52,000 1,84,901 Government Debt-Long Term 68,000 46,099 State Development Loans 21,000 27,000 Total 2,41,000 2,58,000 http://www.sebi.gov.in/cms/sebi_data/attac hdocs/1491222641815.pdf Company Law Powers of Registrar of Companies to strike off the names of companies under section 248(1) of the Companies Act, 2013 Ministry of Corporate Affairs vide notification dated 12th April, 2017 has empowered the registrar of companies to remove/ strike off the names of companies, whose names are listed on the Ministry’s website and have not commenced their business within one year of their incorporation or have not been carrying on any business or operation for a period of two years immediately preceding and have not made any application within such period for obtaining the status of dormant company under section 455 of the Companies Act,2013. https://www.taxmann.com/filecontent.aspx? Page=CIRNO&id=104010000000050613&isxml =Y&search=&tophead=true&tophead=true Amendment in Schedule III

- 18. Page 17Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Ministry of Corporate Affairs vide notification no. GSR 308(E) [F.NO.17/62/2015-CL-V-(VOL.I)] dated 30th March, 2017 has made an amendment in Schedule III, in Division I and Division II of the Companies Act, 2013 which specifies that every company shall disclose the details of Specified Bank Notes (SBN) held and transacted during the period 08/11/2016 to 30/12/2016 as provided in the table below. SBNs Other denomination notes Total Closing cash in hand as on 8-11-2016 (+) Permitted receipts (-) Permitted payments (-) Amount deposited in Banks Closing cash in hand as on 30-12-2016 https://www.taxmann.com/filecontent.aspx?Page=CIRNO&id=104010000000050533&isxml=Y&sear ch=&tophead=true&tophead=true Indirect Taxes Service tax on service rendered by a person located in a non-taxable territory to a person located in non- taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India. CBDT vide notification no. 13/2017-Service Tax has made an insertion of sub-rule (7C) under rule 6 of the Service Tax Rules, 1994 which gives an option to a person located in a non- taxable territory rendering service to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India to pay an amount calculated at 1.4% of the sum of Cost, Insurance and Freight value of such imported goods. http://www.cbec.gov.in/resources//htdocs- servicetax/st-notifications/st-notifications- 2017/st13-updated-2017.pdf trortation ofulated at 1.4% of the sum of cost,

- 19. <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> Raju and Prasad Chartered AccountantsRaju and Prasad Chartered Accountants Page 18 Verdicts Direct Taxation Profit on sale of Shares that are converted into investment from stock-in-trade and sold at a later stage shall be exempted u/s 10(38) -vide decision of high Court of Calcutta, in the case of Deeplok Financial Services Ltd V. Commissioner of Income-tax-II, Kolkata The honorable High Court of Calcutta vide Deeplok Financial Services Ltd V. Commissioner of Income-tax-II, Kolkata held that where the assesse converted the stock-in- trade of shares into investment and sells them at a later stage, profit arising from such sale of shares shall be deemed to be capital gains and not business incomes. If such shares are held with the assesse as long term capital assets, the profit arising from sale of such shares shall be exempt from tax u/s 10(38). https://www.taxmann.com/filecontent.aspx? Page=CASELAWS&id=101010000000174646&is xml=Y&search=&tophead=true&tophead=true Capital gains shall not be levied on sale of agricultural land though agricultural operations are not carried on regularly on such land -vide decision of High Court of Bombay, in the case of Shankar Dalal v. Commissioner of Income Tax, Goa. The honorable High Court of Bombay vide Shankar Dalal v. Commissioner of Income Tax, Goa held that where the assesse sold a piece of land on which he had planted various fruit bearing trees (on an irregular basis) and used the produce for personal consumption and moreover had not filed an application for conversion of land for non-agricultural purpose, in such case the land still remains as an agricultural land agricultural operations were not carried on that land regularly and the agricultural produce is being used for personal consumption. https://www.taxmann.com/filecontent.aspx?Pa ge=CASELAWS&id=101010000000174518&isxml= Y&search=&tophead=true&tophead=true Disclamer Information in this Newsletter, charts, articles, or any other statements regarding market or any other financial information, is obtained from the sources, which we feel reliable. We do not warrant or guarantee the timeliness or accuracy of the information.The reader shall not take any decision based on the facts or figures of the newsletter without professional advice.

- 20. Page 19Raju and Prasad Chartered Accountants <<Hyderabad»NewDelhi»Mumbai»Bangalore»Jalgaon»Navi Mumbai >> ►►► PHOTOGRAPH OF THE MONTH Flock of Sand Pipers in low tide of Arabian Sea - Clicked by M Siva Ram Prasad Please visit http://www.rajuandprasad.com/newsletter.phpfor earlier issues