Korba Call Girls #9907093804 Contact Number Escorts Service Korba

Where to Next for Petrol & Convenience

1. 1

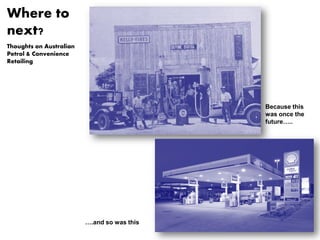

Because this

was once the

future…..

….and so was this

Where to

next?

Thoughts on Australian

Petrol & Convenience

Retailing

2. Market trends internationally indicate an ongoing

decline in performance of traditional Petrol store

performance.

Rising costs of fuel, improving vehicle fuel efficiency,

increased regulatory impact and changing

consumer behaviour has resulted in fuel sales that

are in decline across or at best static across the

developed world. In Australia a contracting fuel

market has for many years been partially offset by

a rationalisation of outlets. This has stabilised and

as a result fuel volumes per outlet look set to now

decline at an increased rate.

By 2030 our population will number as many as 30

million. Despite ongoing increased urban density

the majority of growth will be in the suburbs.

Infrastructure limitations will mean more time spent

commuting.

Our lifestyle is built around the car. By 2025 an

additional 5 million vehicles will be on our roads.

Only the US has a higher vehicle penetration at 820

per thousand versus Australia at 800 by 2018

The Necessity of Change – Risk & Opportunity

More People, More Cars but

Less Time.

Running on Empty – Fuel

Volume Continues to Decline

3. To offset the decline in fuel only performance retailers have for

many years been developing a more diversified offer, placing

greater emphasis on in store categories to supplement falling

income from the forecourt.

Now many of these categories that have formed the core of this

diversification are them selves in decline - tobacco, liquor (in

some markets) along with an decreasing consumption of

impulse snack product – Confectionery, Salty Snacks and high

sugar content beverage. This is partly changing consumer

behaviour (BFY), part regulation (cigarette tax and display

restriction) and part increased competition from alternate

channels seeking to greater exploit consumers increasing desire

for convenience.

Changing consumer preference for product is also apparent as

is the stark rise in offer quality from competing channels -

channel blurring - QSR’s developing full day part and

diversified menus . The continuing rise of Australia's coffee

culture whilst providing great opportunity for growth has also

underpinned the development of a new raft of competitors.

This will precipitate forced change in the Australian

fuel and convenience market. Yet based on the

international experience the Australian market is

proving slow to change and as a result the channel

runs the risk of increasingly losing relevancy to

changing consumer needs and behaviours.

To grow successfully the industry needs to refine its

existing offer and develop new categories to both

capture increased business from those already

shopping with it and from those who’s current and

future needs are not currently being adequately

catered for.

The Necessity of Change –

Risk & Opportunity

4. In Europe & North America

petrol & convenience are

seeing changes…..

5. What Can We Learn from

international experience?

There is no shortage of inspiration but there is a

shortage of time to evolve the Australian Petrol and

Convenience offer.

What follows are a collection of ideas

6. make the

days last

longer

Access is convenience

24 x 7 access will become the operators ticket of admission

This could mean unmanned fuel dispensers or vending machines offering drinks and

snacks.

What it will mean is that when you shut your competitor probably wont.

7. Updated October 22 2012 7

develop sites

that are

advantageous

to doing

business

Developing outlets relevant and specific to the market opportunity.

It could be an unmanned location in the car park of a supermarket,

or a large forecourt capable of catering to increased numbers of

commercial vehicles or RV users.

Sites can satisfy the top up shop or even full shop need of time poor

commuters weary from more time spent in their cars for less

distance travelled.

A place where they pick up their dry cleaning, pay a bill or buy a

lottery ticket. Where meal solutions extend beyond the pie.

A place where filling the tank is not always the reason to visit

8. Updated October 22 2012 8

coalesce things

that are

inconvenient so

as to make them

convenient

The whole purpose of a convenience site

is to make the less convenient alternate

unnecessary

Dry Cleaning ,Postal Pick Up, Click and

Collect, bait, great food……………….

9. the future for petrol is where the cars are

All indications are clear - there is a

future for fuel stations in the

suburbs.

These stations will increasingly

become differentiated by their

complete offer - not limited to the

price of their fuel but rather their

ability to provide consistent and

constant solutions to time poor

travellers.

The “21st century corner store”.

10. Updated October 22 2012 10

not everyone

drives a car

Commercial vehicles are the heavy users of the category. Travelling more kilometres and

consuming more fuel. The drivers are already equally heavy users of store facilities

They are also increasing in number. In 2010 they represented 23% of all vehicles on the road yet

used 41% of all fuel

The segment covers a wide range of vehicles from light commercials under 3.5T GVM to articulated

trucks

Targeting the needs of this segment on the forecourt and in the shop represents a growing

opportunity

11. Updated October 22 2012 11

what is the cost of old

fashioned service?

What is old fashioned

service?

Filling the tank, cleaning the

window, checking the tyres?

Would people care for it?

Would people pay for it?

How high is the bar for

service in convenience in any

case?

What could it look like?

12. Updated October 22 2012 12

let me buy

tomorrow's tank

today

Wouldn’t it be great if I didn’t

have to guess when the cheap

petrol day was?

What if I could lock in

tomorrow’s tank at today's

price?

Research consistently shows that

balances on gift cards or debit

credit cards is more quickly and

more widely distributed than

cash

13. premiumise the

category

Is fuel a commodity for everyone?

Different fuels represent an opportunity to premiumise

the category just as nearly every other FMCG category

has done at some point.

Think toothpaste, think shampoo, think dog food!

Vehicles are close to many people’s hearts and just

about every persons wallet.

14. Updated October 22 2012 14

develop a sales

based mindset

A good owner operator will out perform a good employee operator - if you want to engage your

customers you need to engage your own people first

What would happen if we provided the opportunity to earn a little more and attracted people with

more to offer than the ability to stand on their feet all day.

Pay on performance could have all sorts of positive implications

What types of individuals could be attracted? Does it mean money alone?

15. Updated October 22 2012 15

help me find

the best price

“If you are going to move your prices up and down all

the time the least you can do is help me get the best

price when I need to fill up”.

Increased competitive pricing transparency will happen.

There will be nowhere to hide.

16. Updated October 22 2012 16

develop a meaningful

food offer or find

someone that already

has one

No, this is not a call for more plastic

wrapped sandwiches carrying labels

proclaiming ‘home made’ or ‘fresh cut’

This is about real food - made to order

(MTO).

The prize for developing an offer of

substance is big.

If you can’t achieve find a established offer

and bring them in under roof

17. Do you

even

need

fuel?

A compelling offer.

A place where customers stop by for a multitude of items that

make their time poor lives easier.

The place for great food and coffee 24 x 7 ………and you can buy

fuel.

A business that gets customers thinking that way has arrived.

18. Updated October 22 2012 18

Growing in numbers

and staying mobile

Older Australians are

growing in number and

staying mobile for longer.

By 2026 the number of

Australians over 65 years

of age will have increased

by 100% on the 2006 total

from 2.6M to 5.2M

What will they value?

Drive through windows

and increased levels of

service?

The availability of

assistance on the forecourt

or easier access to parking

or the air hose?

19. Updated October 22 2012 19

The other

50%

The P&C is male dominated.

A large segment of the market never pays a visit.

Why?

In many markets retailers are redesigning the offer and pitching it towards women.

Larger cleaner brighter washrooms - colour schemes and the product offers.

20. How can you call

it convenient if

you cant drive

thru?

QSRs derive anywhere from 50% to

70% of their turnover from their

drive offer.

It is a critical component ;

delivering speed, access and

control to their customers.

Why wouldn’t a convenience offer

provide drive thru service?

You can get a burger at McDonalds

but you can’t get milk, nappies,

chips, chocolate …………… Couple

this to a quality fresh food offer

and who is more convenient now?

21. Blur the lines

You need to look the part.

Do stores need to sadden the soul?

One of these stores is a petrol station. The other

is a fast casual chain charging $10 for a

sandwich.

22. How do we make this

work?

Pay at Pump for fuel is a must.

(This is not necessarily pre

payment)

It will deliver significant

productivity gains and provide

the opportunity for an

improved customer experience

in store.

The question is how to convince

Australian’s that its not simply a

lack of trust.

23. Updated October 22 2012 23

close

the

price

gap

What if the price gap between convenience and grocery closed in one fell

swoop overnight?

The price gap between convenience and grocery will close as chains become

more organised – improve their supply lines and fight back against grocers

moving into smaller formats.