1. With the global chemical industry expected to grow to over $5.5 trillion in revenue by the end

of 2020 driven by expansion in international markets,1

managing fraud risk and compliance

exposure is a critical business priority. Law enforcement agencies, including the United States

Department of Justice (DOJ) and the United States Securities and Exchange Commission

(SEC), are increasingly focused on individual misconduct and have heightened the pressure

on companies to mitigate fraud, bribery and corruption. In this context, executives need to be

confident that their businesses comply with rapidly changing laws and regulations wherever

they operate. While many businesses have made progress in tackling these issues, there

remains a persistent level of unethical conduct.

EY’s Global Fraud Survey 2016 represents the views of nearly 3,000 decision makers in 62

countries and territories, and provides compelling insight into perceptions of fraud, bribery

and corruption across the globe. The following summarizes the insights of the 363 survey

respondents from the chemical industry.

EY’s Global Fraud Survey

2016

Chemical industry results

Download our Global Fraud Survey 2016 report: ey.com/globalfraudsurvey2016

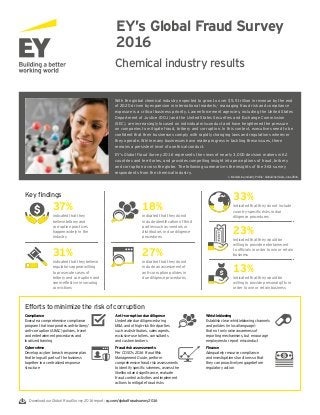

13%

indicated that they would be

willing to provide personal gifts in

order to win or retain business

Key findings

23%

indicated that they would be

willing to provide entertainment

to officials in order to win or retain

business

indicated that they do not include

country-specific risks in due

diligence procedures

33%

37%

indicated that they

believe bribery and

corruption practices

happen widely in the

industry

18%

indicated that they do not

include identification of third

parties such as vendors or

distributors in due diligence

procedures

27%

indicated that they do not

include an assessment of

anti-corruption policies in

due diligence procedures

31%

indicated that they believe

regulators appear willing

to prosecute cases of

bribery and corruption and

seem effective in securing

convictions

Efforts to minimize the risk of corruption

Compliance

Execute a comprehensive compliance

program that incorporates anti-bribery/

anti-corruption (ABAC) policies, travel

and entertainment procedures and

localized training

Cybercrime

Develop a cyber breach response plan

that brings all parts of the business

together in a centralized response

structure

Anti-corruption due diligence

Undertake due diligence during

M&A and of high-risk third parties

such as distributors, sales agents,

exclusive-use tollers, consultants

and custom brokers

Fraud risk assessments

Per COSO’s 2016 Fraud Risk

Management Guide, perform

comprehensive fraud risk assessments

to identify specific schemes, assess the

likelihood and significance, evaluate

fraud control activities and implement

actions to mitigate fraud risks

Whistleblowing

Establish clear whistleblowing channels

and policies (in local language)

that not only raise awareness of

reporting mechanisms, but encourage

employees to report misconduct

Finance

Adequately resource compliance

and investigations functions so that

they can proactively engage before

regulatory action

1. MarketLine, Industry Profile - Global Chemicals, June 2016.