1. Year 2015 2016E 2017E

P/E 39.58 37.38 30.54

PEG 9.40 1.90 1.50

P/Sales 0.99 1.27 1.16

P/FCF 46.09 28.29 16.61

P/Book 1.93 2.60 2.56

December 11, 2016

T-MOBILE US INC - (TMUS)

“Yeah, I Could Hear You the Entire Time”

OUSEMGEQUITYRESEARCH 1

Investment Thesis

T-Mobile US, Inc., offers voice, messaging, and data services in the postpaid,

prepaid, and wholesale markets for customers and businesses in the United

States, Puerto Rico, and the U.S. Virgin Islands.

Thesis Highlights

Growing LTE Demand in a Growing Data Market

Overall mobile subscriptions are expected to increase from 7.3 billion in 2015 to over

9 billion by 2021, 4.3 billion of which are expected to be LTE based subscriptions.

This is the effects of a shift to more advanced technologies in developed markets

such as Western Europe and North America.

Branded Segments Outperform With Help From Initiatives

TMUS provides wireless communication services to three primary categories of

customers: branded postpaid, branded prepaid, and wholesale. Due largely in part to

its aggressive pricing model and the success of MetroPCS, T-Mobile is the only

wireless company with positive net growth in both postpaid and prepaid. For Q3 the

postpaid segment of TMUS saw 890,000 net adds versus –185,000 for T, 86,000 for

VZ and 173,000 for sprint. Likewise, its prepaid segment saw growth of 8 percent in

both revenue and customer base YOY in 2015.

Network Investment and Expansion

TMUS has been investing significantly over the years to enhance its network and

provide faster high-bandwidth mobile communications services. During FY2014 and

FY2015, the company’s capital expenditures for property and equipment related to

network modernization and expansion were $4.5 billion and $4.3 billion respectively.

And for 2016, that number is expected be in the $4.5 billion to $4.8 billion range.

TMUS is also focused on expanding network coverage through an aggressive

spectrum acquisition strategy with multiple acquisitions in 2014, 2015, and 2016.

Thesis Risks

Net Neutrality

Net neutrality has become an increasingly common buzzword during the last decade,

as digital privacy and service quality issues move into public view. Pricing plans and

data speed have been the main concern for firms in this industry, as changes in

federal regulation could drastically affect the viability of current revenue streams, in

addition to creating new challenges for existing business models. Management has

outlined these new regulations as a significant risk that has yet to fully play out.

Combined with recent rulings from the FCC in February and June, many of these

worst cases scenario risks have been confirmed.

Stock Rating: Buy

Price Target

Current Price

$66.05 (16.4%)

$56.74

Relevant Information

ROE 8.03%

EV/EBITDA 7.55

Current Ratio 1.67

Short Interest 5.96%

Dividend Yield 0.00%

Debt Rating BB

Next Earnings Date 02/22/2017

Analysts Mozika Maloba

Head Analyst

Peter Rousseau

Junior Analyst

Brad Morrissey

Junior Analyst

Collin Patterson

Analyst

Nick Gilkey

Analyst

Company Information

Sector Communications

Industry Telecom

Market Cap $46.75B

Sales $35.31B

Beta 0.78

Price-Based Multiples

$30

$35

$40

$45

$50

$55

$60

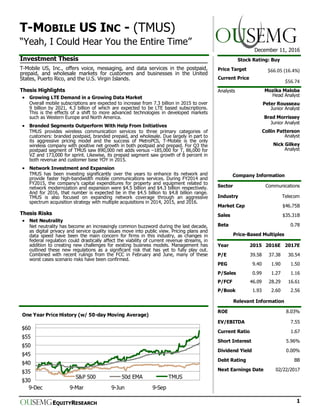

9-Dec 9-Mar 9-Jun 9-Sep

One Year Price History (w/ 50-day Moving Average)

S&P 500 50d EMA TMUS

2. OUSEMGEQUITYRESEARCH 2

DECEMBER 11, 2016 | T-MOBILE US INC. (TMUS)

Thesis Point 1:

▪ Opportunity For LTE

Market Capitalization

Growing LTE Demand in a Growing Data Market

Opportunity For LTE Market Capitalization

TMUS has a large opportunity to capitalize on the growing demand for LTE/4G

Technology. Overall mobile subscriptions are expected to increase from 7.3 billion in

2015 to over 9 billion in 2021. Of the total mobile subscriptions, LTE based

subscriptions are estimated to be over 4.3 billion by 2021. The shift is mainly due to

substantial migration to more advanced technologies including WCDMA/HSPA and LTE

in developed markets such as Western Europe and North America. Specifically in

North America, overall mobile subscriptions look to sustain a LSD CAGR through 2021.

Substantial growth, however, will be seen in Data Traffic and Total Mobile Traffic,

stemming from an increase use of the smartphone for streaming and Internet

browsing.

As the consumer trends are examined, they tend to favor TMUS. For example, only 23

percent of U.S. consumers have an unlimited data plan; yet the monthly mobile phone

data allowance plans held by domestic customers are shifting to higher GB plans as

data traffic increases. In addition, in an Ericsson analysis, “network measurements on

LTE networks showed significant opportunities for improvement in cell-edge

performance in the U.S.”, essentially meaning that LTE has displayed speeds that are

still below expectations with regards to collaboration services and HD video viewing.

Deloitte supports the Mobile Traffic growth thesis, noting that 72 percent of 18-24

year olds use their mobile phones while watching TV/a film (as well as 74 percent of

25-34 year olds), while in the older demographics that percentage drops down to

30-40.

U.S. and Canada Mobile Projections

2015 2021 CAGR 2015-

Mobile Subscriptions (million) 390 450 2%

Smartphone Subscriptions (million) 280 370 5%

Data Traffic per active smartphone (GB/

month) 3.8 22 35%

Total Mobile Traffic (EB/month) 1.3 8.5 35%

3. OUSEMGEQUITYRESEARCH 3

DECEMBER 11, 2016 | T-MOBILE US INC. (TMUS)

Branded Segments Outperform With Help From Initiatives

Branded Segments Impressive Performance

T-Mobile’s branded operating segments have significantly outperformed competitors

over roughly the last three years. The postpaid segment which accounts for 51

percent of revenue saw a 13.8 percent increase in revenue in FY15 while the growing

prepaid segment accounting for 24 percent of revenue increased revenue by ~8

percent.

Management announced on September 20th QTD postpaid net phone adds of 753k

with estimates around 814k for the quarter. This compares to leading competitors S,

VZ and T registering roughly 173k, 86k and -185k respectively. Since the second

quarter of 2013 when TMUS began adding postpaid phone subscriptions, they have

captured 90 percent of growth in the industry. Managements release of QTD

performance for prepaid in September net phone adds was 650k with a full quarter

estimate of 715k.

The main focus for the prepaid segment has been on the Metro PCS brand.

Management continues to leverage the recognizable and higher quality prepaid brand

to significantly grow prepaid customer base. Metro PCS achieved 167 percent growth

over the last year in its third full year of operation under TMUS following the

acquisition completion in 2013. Additionally, Metro PCS added more than 476k

customers in 2Q16 due in large to its impressive geographic expansion. TMUS has

been the only wireless company with positive net subscriber growth in both prepaid

and postpaid segments for twelve consecutive quarters. Moving forward under the Un

-carrier initiative, management looks to explore joint distribution between the two

segments to continue to optimize both brands.

Un-carrier Initiative

Launched in 2013, Un-carrier has been TMUS’s radical initiative to drive simplification

and transparency for customers through various promotions and plan benefits. JUMP!

is an offering that allows customers to pay an additional $10-$30 a month that allows

them to upgrade their handset every six months with insurance and extended

warranty. One of the most influential initiatives introduced was Binge On. This

offering made video streaming 3x more efficient for customers while allowing them to

stream programs such as HBO, Hulu, Netflix, and WatchESPN for free. Over 99

percent of customers kept Binge On activated with their plans when introduced and

has significantly increased customer video consumption. The success of Binge On led

to the development and implementation of T-Mobile ONE, TMUS’s sole postpaid plan

offering moving forward. Launched in September, this plan provides unlimited talk,

text, 4G LTE, and video and music streaming at a more affordable price. For one line

this plan is $70, to add a second line it is $50, and for all lines beyond that it is $20.

T-Mobile ONE has created significant differentiation from competitors and provided a

strong runway for outperformance over the investment horizon. TMUS’s network

capacity allows them to be the only major carrier capable of implementing this

unlimited strategy for all customers while increasing quality globally, benefiting the

network, and increasing ARPU. Due to the 480p resolution video streaming limit,

TMUS has cut existing data consumption by 50 percent and directed customers away

from HD streaming. As this strategy is fully rolled out, TMUS will see significant upside

as results continue to distance themselves from overcrowded network providers such

as Verizon and AT&T.

Thesis Point 2:

▪ Continued outperformance

in net adds

▪ Un-Carrier initiative

4. OUSEMGEQUITYRESEARCH 4

DECEMBER 11, 2016 | T-MOBILE US INC. (TMUS)

Network Investment and Expansion

Expansive Network in the U.S.

T-Mobile has had the fastest 4G LTE Network for the past two and a half years, and

on August 4, 2016, Nielsen Mobile Insights released results from a survey placing

TMUS at the top for customer sentiment. TMUS uses mid-band spectrum licenses

such as Advanced Wireless Services and Personal Communications Services, and low-

band spectrum licenses which utilizes its 700 MHz A-Block spectrum. On its 700 MHz

A-Block Spectrum, TMUS is able to deploy its Extended Range LTE which is able to

reach twice the distance and work four times faster in buildings on average than its

regular LTE signal. This upgraded LTE service currently covers 190 million people in

over 300 market areas. TMUS’s LTE service as a whole has had a YOY growth of 40

million customers from 2014 to 2015, bringing its coverage to 305 million people, and

its nationwide network covers 91 percent of people in the U.S.

The Growing Process of the TMUS LTE Network

TMUS has also been investing significantly over the past couple of years into

enhancing its network to provide higher-bandwidth mobile communications services.

These past investments have been made primarily to support the growth of LTE and

have therefore focused on the use of a strategy focused on modernizing its network

and 4G evolutions. In 2014, TMUS acquired multiple spectrum licenses in 19 markets

from Verizon Wireless for 700 MHz A-Block Advanced Wireless Service (AWS) and

Personal Communications Services (PCS), costing it $2.4 billion. Along with this, TMUS

also acquired AWS spectrum licenses that covered 97 million people. TMUS continued

to invest in its network throughout 2015 by entering into multiple agreements with

Verizon (VZ) and AT&T (T) for the exchange of additional AWS and PCS spectrum

licenses. TMUS plans to continue to invest into 2016 as well with an increase of $300

million in the range of capital expenditures for property and equipment from FY2015,

but its past investments have already put TMUS next to its competitors in LTE

coverage.

TMUS is currently the nation’s third-largest wireless carrier with around 68 million

customers. However, Its LTE network covers nearly 312 million POPs, which is higher

than T’s roughly 300 million POPs and right alongside VZ’s 312 million POPs. Now

TMUS is able to focus on the development of its network so that it can cover patchy

areas and enable high-speed LTE connections across its entire network. TMUS

primarily works on its AWS-1 and 700 MHz licenses, but it spent around $1.8 billion

on AWS-3 spectrum licenses, and has said it could start building out those licenses as

early as this year.

The Federal Communications Commission's Auction

T-Mobile has had the fastest 4G LTE Network for the past two and a half years, and

on August 4, 2016, Nielsen Mobile Insights released results from a survey placing

TMUS at the top for customer sentiment. TMUS uses mid-band spectrum licenses

such as Advanced Wireless Services and Personal Communications Services, and low-

band spectrum licenses which utilizes its 700 MHz A-Block spectrum. On its 700 MHz

A-Block Spectrum, TMUS is able to deploy its Extended Range LTE which is able to

reach twice the distance and work four times faster in buildings on average than its

regular LTE signal. This upgraded LTE service currently covers 190 million people in

over 300 market areas. TMUS’s LTE service as a whole has had a YOY growth of 40

million customers from 2014 to 2015, bringing its coverage to 305 million people, and

its nationwide network covers 91 percent of people in the U.S.

Thesis Point 3:

▪ Expansive Network in the

U.S.

▪ The Growing Process of

the TMUS LTE Network

▪ The FCC’s Auction

5. OUSEMGEQUITYRESEARCH 5

DECEMBER 11, 2016 | T-MOBILE US INC. (TMUS)

Net Neutrality

Service As a Utility

Management notes that they have yet to fully experience the anticipated downside

from the reclassification of their services as publicly necessary utilities, similar to

bussing, airlines, and telephone lines. The FCC intends to redefine wireless service

providers as Title 2 utilities, which would greatly increase their regulation from state

and local governments. By viewing these services as public goods instead of luxuries,

the FCC has indicated that customers should have easier access to these services, and

at a price that everyone can pay. Monopolies and collaborative agreements between

firms will also be more closely monitored by a wider variety of regulatory authorities,

further benefiting the consumer.

Defining Data

New contracts will require greater transparency and scrutiny from authorities before

being put in place, while existing plans will benefit from being grandfathered in with

less strict regulations. For TMUS, current pricing plans are well-established and should

fare better than its competitors, which have been relatively slow to adapt pricing

around data. The quality of service these contracts provide will also be homogenized,

eliminating data-throttling and fast lanes. This will eliminate partnership opportunities

for third parties who may wish to speed up their service for certain customers. This

has been a focal point of recent controversy, as Netflix and other streaming services

require significant amounts of high speed data, and are willing to pay extra to

guarantee a high quality service for their customers. Companies have employed data

throttling on customers using significant amounts of data, restricting the available

streaming speed regardless of their contract. This has led many firms to redefine

unlimited data according to their personal preference, and even to claim that

customers don’t need or want such unlimited services.

Thesis Risk 1:

▪ Service As a Utility

▪ Defining Data