Report

Share

Download to read offline

Recommended

A practical method for advisers to measure exposure to sequence risk is through evaluation of the current probability of failure rate (which I've later renames as iteration failure rate to reflect measurement of the Monte Carlo simulation rather than the plan itself - two different things). This paper lead to a deeper investigation of failure rates thus leading to two subsequent papers discovering the three-dimensional nature of simulations over various time periods and allocations, as well as application of longevity to the simulation modeling.The Dynamic Implications of Sequence Risk on a Distribution Portfolio Journal...

The Dynamic Implications of Sequence Risk on a Distribution Portfolio Journal...Better Financial Education

Recommended

A practical method for advisers to measure exposure to sequence risk is through evaluation of the current probability of failure rate (which I've later renames as iteration failure rate to reflect measurement of the Monte Carlo simulation rather than the plan itself - two different things). This paper lead to a deeper investigation of failure rates thus leading to two subsequent papers discovering the three-dimensional nature of simulations over various time periods and allocations, as well as application of longevity to the simulation modeling.The Dynamic Implications of Sequence Risk on a Distribution Portfolio Journal...

The Dynamic Implications of Sequence Risk on a Distribution Portfolio Journal...Better Financial Education

This first appeared in blog post that describes the graphs in more details

https://blog.betterfinancialeducation.com/sustainable-retirement/what-are-the-three-paradigms-of-retirement-planning/

Prototype software example of aging model incorporating both portfolio and longevity percentile statistics along with consumer spending trend line of “Real People” (which is not based here on spending percentile statistics, but on research averages). Starting balance $500,000 with $36,000 Social Security. Two simple graphs by age answer many retiree questions about potential future spending and balances. Creates a whole different discussion. Also illustrates why age 95 is a poor reference for planning since it doesn’t plan or consider aging into future ages from the beginning of retirement.Prototype software example of aging model incorporating both portfolio and lo...

Prototype software example of aging model incorporating both portfolio and lo...Better Financial Education

Have you ever wondered who is buying if so many people are selling?

The notion that sellers can outnumber buyers on

down days doesn’t make sense. What the newscasters should say, of course, is that prices adjusted lower because would-be buyers weren’t prepared to pay

the former price.

What happens in such a case is either the would-be sellers sit on their shares or prices quickly adjust to the point where supply and demand come into balance and transactions occur at a price that both buyers

and sellers find mutually beneficial. Economists refer

to this as equilibrium. A question of equilibrium - can there be more buyers than sellers? Or more se...

A question of equilibrium - can there be more buyers than sellers? Or more se...Better Financial Education

More Related Content

More from Better Financial Education

This first appeared in blog post that describes the graphs in more details

https://blog.betterfinancialeducation.com/sustainable-retirement/what-are-the-three-paradigms-of-retirement-planning/

Prototype software example of aging model incorporating both portfolio and longevity percentile statistics along with consumer spending trend line of “Real People” (which is not based here on spending percentile statistics, but on research averages). Starting balance $500,000 with $36,000 Social Security. Two simple graphs by age answer many retiree questions about potential future spending and balances. Creates a whole different discussion. Also illustrates why age 95 is a poor reference for planning since it doesn’t plan or consider aging into future ages from the beginning of retirement.Prototype software example of aging model incorporating both portfolio and lo...

Prototype software example of aging model incorporating both portfolio and lo...Better Financial Education

Have you ever wondered who is buying if so many people are selling?

The notion that sellers can outnumber buyers on

down days doesn’t make sense. What the newscasters should say, of course, is that prices adjusted lower because would-be buyers weren’t prepared to pay

the former price.

What happens in such a case is either the would-be sellers sit on their shares or prices quickly adjust to the point where supply and demand come into balance and transactions occur at a price that both buyers

and sellers find mutually beneficial. Economists refer

to this as equilibrium. A question of equilibrium - can there be more buyers than sellers? Or more se...

A question of equilibrium - can there be more buyers than sellers? Or more se...Better Financial Education

More from Better Financial Education (20)

Prototype software example of aging model incorporating both portfolio and lo...

Prototype software example of aging model incorporating both portfolio and lo...

A question of equilibrium - can there be more buyers than sellers? Or more se...

A question of equilibrium - can there be more buyers than sellers? Or more se...

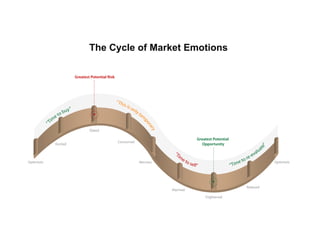

Cycle of market emotions

- 1. The Cycle of Market Emotions