Underbanked and Unbanked Consumers in the U.S.: Successfully Targeting Consum...

Final Poster Chensen Wang

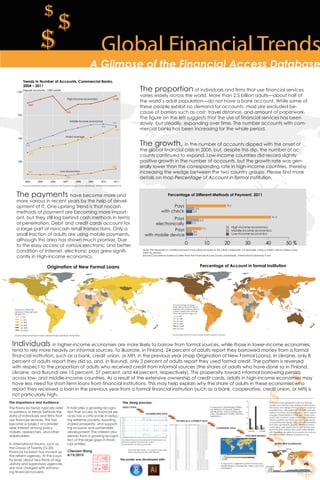

1. 300

600

900

1,200

2004 2005 2007 2009 20112006 2008 2010

Deposit accounts, 1,000 adults

High income economics

Middle income economics

World average

Low economics

1057

536

417

137

120

207

747

786

766

962

1153

Trends in Number of Accounts, Commercial Banks,

2004 – 2011

Source:Calculations based on data from the Financial Access Survey (database), International Monetary Fund

Global Financial Trends$

$

$

$

$

$

$

$

The proportion of individuals and firms that use financial services

varies widely across the world. More than 2.5 billion adults—about half of

the world’s adult population—do not have a bank account. While some of

these people exhibit no demand for accounts, most are excluded be-

cause of barriers such as cost, travel distance, and amount of paperwork.

The figure on the left suggests that the use of financial services has been

slowly, but steadily, expanding over time. The number accounts with com-

mercial banks has been increasing for the whole period.

The growth, in the number of accounts dipped with the onset of

the global financial crisis in 2008, but, despite this dip, the number of ac-

counts continued to expand. Low-income countries did record slightly

positive growth in the number of accounts, but the growth rate was gen-

erally lower than the corresponding rate in high-income countries, thereby

increasing the wedge between the two country groups. Please find more

details on map Percentage of Account in formal Institution.

A Glimpse of the Financial Access Database

The Importance and Audience

The financial trends typically refer

to patterns or trends behinds the

data of individuals and firms that

use financial services. This has

become a subject of consider-

able interest among policy

makers, researchers, and other

stakeholders.

In international forums, such as

the Group of Twenty (G-20),

financial inclusion has moved up

the reform agenda. At the coun-

try level, about two-thirds of reg-

ulatory and supervisory agencies

are now charged with enhanc-

ing financial inclusion.

0 10 20 30 40 50 %

Pays

with check

Pays

electronically

Pays

with mobile device

High-income economics

Middle-income economics

Low-income economics

19.3

3.9

2.9

6.3

2.5

7.5

2.6

3.3

41.3

Source:Calculations based on data from the Financial Access Survey (database), International Monetary Fund

Note: The response on mobile payments may subsume some of the other categories. For example, using a credit card to make a pay-

ment by phone.

Percentage of Different Methods of Payment, 2011The payments have become more and

more various in recent years by the help of devel-

opment of IT. One uprising trend is that nocash

methods of payment are becoming more import-

ant, but they still lag behind cash methods in terms

of penetration. Debit and credit cards account for

a large part of noncash retail transactions. Only a

small fraction of adults are using mobile payments,

although this area has shown much promise. Due

to the easy access of various electronic and better

condition of Internet, electronic pays grew signifi-

cantly in High-income economics.

0−6%

6−12%

12−18%

18−24%

24−30%

No Data

Loan from a financial

institution in the past year

(% age 15+)

Source:Global Financial Inclusion (Global Findex) Database, World Bank.

Origination of New Formal Loans

0−20%

20−40%

40−60%

60−80%

80−100%

No Data

The percentage of respon-

dents with an account (self or

together with someone else) at

a bank, credit union, another

financial institution (age 15+)

Source:Global Financial Inclusion (Global Findex) Database, orld Bank.

Percentage of Account in formal Institution

Individuals in higher-income economies are more likely to borrow from formal sources, while those in lower-income economies

tend to rely more heavily on informal sources. To illustrate, in Finland, 24 percent of adults report they borrowed money from a formal

financial institution, such as a bank, credit union, or MFI, in the previous year (map Origination of New Formal Loans). In Ukraine, only 8

percent of adults report they did so, and, in Burundi, only 2 percent of adults report they used formal credit. The pattern is reversed

with respect to the proportion of adults who received credit from informal sources (the shares of adults who have done so in Finland,

Ukraine, and Burundi are 15 percent, 37 percent, and 44 percent, respectively). This propensity toward informal borrowing persists

across low- and middle-income countries. As a result of the extensive ownership of credit cards, adults in high-income economies may

have less need for short-term loans from financial institutions. This may help explain why the share of adults in these economies who

report they received a loan in the previous year from a formal financial institution (such as a bank, cooperative, credit union, or MFI) is

not particularly high.

It indicates a growing recogni-

tion that access to financial ser-

vices has a critical role in reduc-

ing extreme poverty, boosting

shared prosperity, and support-

ing inclusive and sustainable

development. The interest also

derives from a growing recogni-

tion of the large gaps in finan-

cial entities.

The poster was developed with:

Chensen Wang

4/15/2015

The desig process:

SELECT TOPIC

ACQUIRE RAW DATA

TECHNICALLY CORRECT DATA

CONSISTENT DATA

PLOT WITH RSTUDIO

REFINE WITH ILLUSTRATOR

The Global Financial Development Database is an

extensive dataset of financial system

characteristics for 203 economies

One example table of consistent data after

date cleaning process with Rstudio.

0 30

GFDD.AI.07

Adult Loan Percentage

0−6%

6−12%

12−18%

18−24%

24−30%

No Data

R original plot, Origination of New Formal Loans.

Used Illustrator to change title, refine color, fonts

and legend.

avg.checks avg.mobile

01020304050

R original plot, Percentage of Differ-

ent Methods of Payment. Refined

with Illlustrator, works including add

color, change fonts, rotate, add text

explanation.

GFDD.AI.05

Adult Account Percentage

0−20%

20−40%

40−60%

60−80%

80−100%

No Data

Plots and maps generated with R or Rstudio

usually can only flect the statistical information,

the layout and design of those charts could be

unsatisfactory. Although R and Rstudio provids

various functions and packages to allow user to

change characteristics of the plot, these work

could only conduct under command interface

which is painful and time-consuming. Illustrator,

as a professional design tool, provides powerful

tool and user-friendly graphic interface which

could allow user open r plot in pdf format and

reine the plots quickly. Also, plots after refined

with Illustrator are able to be saved into various

formats to satisfy diferent purpose of use.